We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Covid crash #2 started

Comments

-

It will depend how well it is managed. Not only will there be gradually rising of interest rates that will encourage that cautious money back into bonds, but the central banks will also likely step back from QE by selling bonds back into the market place or at least not buying more (and getting their money back that they have injected). Check out the 2013 taper tantrum of what could happen again if they are not careful.vacheron said:

This is exactly my feeling too. There is nowhere else to put money, people are currently unable to spend it in the manner they used to, and other savings options are worse than poor, so the marked demand is driven by the amount of money entering the market rather than the fundamentals of the companies themselves.talexuser said:Surely the difference with selling today is there is nowhere else to put your cash in the meantime deliberate era of QE, ultra low interest and relative bond rates? This is how growth and markets have been kept going since the credit crunch. Even property is now likely for a crash sometime.

The pandemic has changed everything, assuming we get back to normal with a vaccine, the next stage has to be deliberate higher inflation, the only way out without write offs, growth ain't going to do it anytime soon.

This could lead to a second question, what are the chances of a market crash actually occuring when the economy begins to pick up, as there is a risk that if interest and bond rates rise billions of pounds worth of "cautious" money could bail out in droves?1 -

Prism said:

It will depend how well it is managed. Not only will there be gradually rising of interest rates that will encourage that cautious money back into bonds, but the central banks will also likely step back from QE by selling bonds back into the market place or at least not buying more (and getting their money back that they have injected). Check out the 2013 taper tantrum of what could happen again if they are not careful.vacheron said:

This is exactly my feeling too. There is nowhere else to put money, people are currently unable to spend it in the manner they used to, and other savings options are worse than poor, so the marked demand is driven by the amount of money entering the market rather than the fundamentals of the companies themselves.talexuser said:Surely the difference with selling today is there is nowhere else to put your cash in the meantime deliberate era of QE, ultra low interest and relative bond rates? This is how growth and markets have been kept going since the credit crunch. Even property is now likely for a crash sometime.

The pandemic has changed everything, assuming we get back to normal with a vaccine, the next stage has to be deliberate higher inflation, the only way out without write offs, growth ain't going to do it anytime soon.

This could lead to a second question, what are the chances of a market crash actually occuring when the economy begins to pick up, as there is a risk that if interest and bond rates rise billions of pounds worth of "cautious" money could bail out in droves?And the Q4 2018 "tantrum" as well.I think the far bigger long term risk is inflation and inflation expectations surprising to the upside. Something like a 3-5% persistently can very well happen and I would not rule out more than 5% either. That will almost certainly lead to a big repricing event in financial markets.1 -

Yes, inflation would create a significant alteration in how a lot of people see the markets. Hard to know how that happens though when globalisation and automation is making stuff cheaper and people need to feel confident to start spending. Governments have struggled to encourage it too over recent years, probably because they were reluctant to go on big spending sprees. We shall see I guess.itwasntme001 said:Prism said:

It will depend how well it is managed. Not only will there be gradually rising of interest rates that will encourage that cautious money back into bonds, but the central banks will also likely step back from QE by selling bonds back into the market place or at least not buying more (and getting their money back that they have injected). Check out the 2013 taper tantrum of what could happen again if they are not careful.vacheron said:

This is exactly my feeling too. There is nowhere else to put money, people are currently unable to spend it in the manner they used to, and other savings options are worse than poor, so the marked demand is driven by the amount of money entering the market rather than the fundamentals of the companies themselves.talexuser said:Surely the difference with selling today is there is nowhere else to put your cash in the meantime deliberate era of QE, ultra low interest and relative bond rates? This is how growth and markets have been kept going since the credit crunch. Even property is now likely for a crash sometime.

The pandemic has changed everything, assuming we get back to normal with a vaccine, the next stage has to be deliberate higher inflation, the only way out without write offs, growth ain't going to do it anytime soon.

This could lead to a second question, what are the chances of a market crash actually occuring when the economy begins to pick up, as there is a risk that if interest and bond rates rise billions of pounds worth of "cautious" money could bail out in droves?And the Q4 2018 "tantrum" as well.I think the far bigger long term risk is inflation and inflation expectations surprising to the upside. Something like a 3-5% persistently can very well happen and I would not rule out more than 5% either. That will almost certainly lead to a big repricing event in financial markets.0 -

This thread asks those questions. You listen to the arguments, you do your own research, you hold your own counsel.AlanP_2 said:....Have we had GFC2? Are we currently in GFC2? Is it a possible event at an unknown point in the future? When does normal market movements become a GREAT FINANCIAL CRASH?Don't worry about missing it, you'll know full well when it happens..._0 -

All this talk about potential crashes is a little concerning, particularly for moderately informed non-pro investors. Crystal balls aside, it seems to make sense that the markets will fall due to recent Covid developments, fallout from the whole Covid situation, and perhaps even the influence of the credit crunch. I'm mid 50s, and have some higher equity funds alongside core balanced ones. I have been thinking about possibly selling the higher eq ones to protect myself a little bit in anticipation of some such crash, and then potentially buying back in again. Not sure if this is sensible.0

-

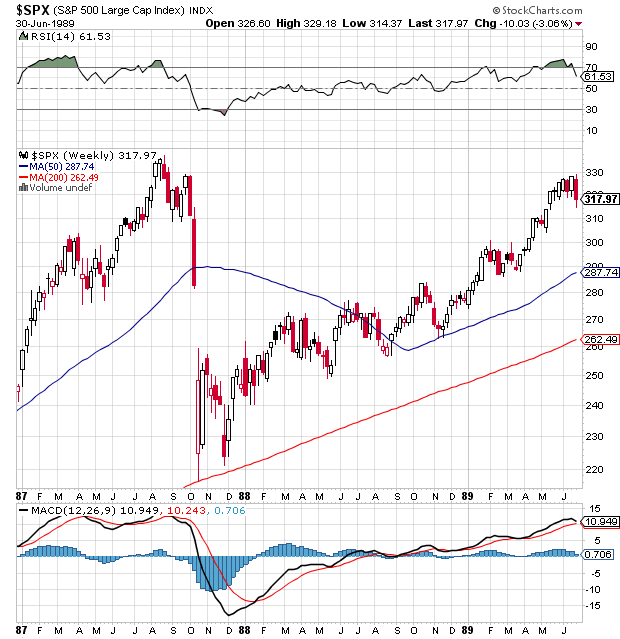

Nobody knows when a crash will happen but history shows markets have rallies and then either go sideways or correct. Looking at main indices such as the Dow and S&P 500 you can see many examples when a rally gets way above the 200 day average on a chart then corrects.

The 1987 crash was a prime example of a parabolic rise which ended badly . The S&P stood at 330 and the 200 day moving average around 220. At 50% above this is a rare event.

https://ivanhoff.com/wp-content/uploads/2016/10/spy1987-weekly.png

Generally when the index gets 10% and more above the 200 day average there's a correction of some sort. In the link below there's three. First was the virus in February then September and October recently.

https://stockcharts.com/h-sc/ui?s=$SPX&p=D&yr=1&mn=0&dy=0&id=p27848000232&a=226295345&listNum=1

Set this link below to 5 years and you can see clearly these mini parabolic moves way above the 200 day average. Although they may only be 10% or more they show the same chart pattern. I think the link will go back a few decades if anybody wants to see more. Basically if any investor is concerned about holding onto profits it's certainly worth watching the indices if the 10% region is breached. Apart from that its pretty difficult to predict anything really.

https://stockcharts.com/h-sc/ui2 -

All this talk about potential crashes is just that, all talk.Shocking_Blue said:All this talk about potential crashes is a little concerning, particularly for moderately informed non-pro investors. Crystal balls aside, it seems to make sense that the markets will fall due to recent Covid developments, fallout from the whole Covid situation, and perhaps even the influence of the credit crunch. I'm mid 50s, and have some higher equity funds alongside core balanced ones. I have been thinking about possibly selling the higher eq ones to protect myself a little bit in anticipation of some such crash, and then potentially buying back in again. Not sure if this is sensible.

If all these self appointed financial experts actually knew anything they wouldn't be sitting at their computer screens posting rubbish on a money saving forum day in day out.4 -

The other thing to remember is that all the major central banks have been printing huge amounts of money. So any increase in equities is some reflection of that; the dollar, euro, pound, yen etc that you have now is 'worth' far less than it would have been several years ago which is why most asset prices have increased so much in recent years.0

-

I assume that comment is only directed at those posting very specific predictions about how the market is going to crash last week, early next year, on your mum's birthday, etc. The rest of us self appointed financial experts who are not predicting any specific time for the next crash and only talk about risk in general terms can be trusted because of course we have the experience of posting on a money saving forum day in day out....The_Green_Hornet said:If all these self appointed financial experts actually knew anything they wouldn't be sitting at their computer screens posting rubbish on a money saving forum day in day out.1 -

Lower risk rated balanced funds have performed better over the past 3 years. A very different picture to the 5 year history. An exceptional year can provide a false sense of security. Trends are noticeable well before there's media commentary.Shocking_Blue said:All this talk about potential crashes is a little concerning, particularly for moderately informed non-pro investors. Crystal balls aside, it seems to make sense that the markets will fall due to recent Covid developments, fallout from the whole Covid situation, and perhaps even the influence of the credit crunch. I'm mid 50s, and have some higher equity funds alongside core balanced ones. I have been thinking about possibly selling the higher eq ones to protect myself a little bit in anticipation of some such crash, and then potentially buying back in again. Not sure if this is sensible.0

{kind=link}

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards