We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

The Top Regular Savers Discussion Thread

Comments

-

Re whether to close an existing account in order to open the new 8% one…

Yes, a lot depends on what capacity you have elsewhere.

The ideal regular saver strategy is to have the minimum amount in other easy access savers at any one time, and to maximise the amount that's in higher paying accounts. An ideal scenario would be to have regular savers maturing at regular intervals throughout the year, so that when each one matures it can be used to fund the others, and doesn't have to be dumped in a lower-paying easy access account. That's if you want to keep your money circulating around your regular savers. Or you might like to schedule your maturity dates so that you get a nice lump sum in time for Christmas / summer holidays.

I did a very simple spreadsheet to work out whether it's worth hanging on to the old Club Lloyds regular saver or sacrificing it for a higher interest rate but lower monthly deposit. And it seems (from a crude number-crunch) that once the account is a few months old, it becomes more beneficial to keep it.

The reasoning behind that conclusion is that you'll have a lump sum that you suddenly need to find a home for, at a much lower rate.

But consider that you'll have to find a home for that lump sum at some point, either now by closing early, or for the full balance in a few months' time.

So to get a truly accurate picture you'd need to run the figures over a longer period of time. I haven't done this yet, but I think it would swing more in favour of opening the 8% account.

2 -

HALIFAX RS

Tried logging in via my Halifax login but it still didn't give me the option to open the monthly saver.

So it might work for some but not me!

I found it listed in the fixed Saver Section after pressing the apply button

was metioned up thread but with so manny contributions it might have got lost

Mortgage Free 02/02/20240 -

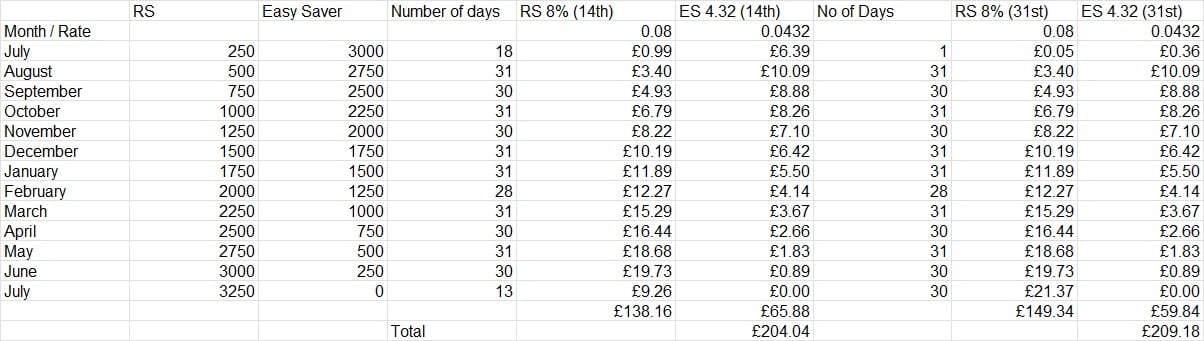

I did a calc on it yesterday, there around £5 in it, I thought the risk was too great to not go for it now. Maybe I will refresh it at the end of the month, depends on how it all plays out with the trouble people are having and luckily I had no problem yesterday refreshing mine.

Edit : Picture changed, realised the easy saver should have started with £3k not £3.25k, still £5 difference, just not so much interest in the total.

2 -

if the £250 wasn’t in the 8% RS it could be earning up to 5% in an EA acc, so the actual gain is less than half the figure that you quoted

0 -

I imagine it should be possible, the process for me was a download of the Lloyds app which somehow already knew I was a HF customer (possibly as I’d used the app before but had since deleted it) and required the accounts to be linked before continuing.

Once the change was authorised in the HF app, everything was available in Lloyds immediately and I could complete the Lloyds RS application in-app right away. Lloyds RS opened instantly and funded shortly after - Whole affair took maybe a few minutes once I decided to complete the account migration to get the Lloyds app up and running. Of course that’s discounting the hour I spent failing to log into Lloyds online first.Moo…2 -

If the £250 wasn't in the 8% RS it could have been spent down the pub or it could have made £9k in 20 seconds on the turn of a roulette wheel.

Where else the £250 could be is irrelevant to the question.

0 -

Halifax to Lloyds……..

I’m a Halifax customer with RS, registered for Mobile and Online Banking. Not a Lloyds or BOS customer. Also not been invited to migrate apps yet. Further to post from ‘TheElectricCow’ I downloaded the Llloyds app (iOS) and when launching it, get the following screen, so it seems migration is possible already.Not progressed any further and I am intrigued whether the opening of Lloyd’s RS would be possible.

2 -

Of course it is relevant.

The question was relating to the benefit of holding off opening the 8% RS until the 31st July.

You sound like you are having a bad day. Are you French?

5 -

Halifax/Lloyds

I have never downloaded the apps for either of these, always used the main computer. I've never seen the need to have the app. I've only used them these 2 for regular saver purposes so I check once a month and at the maturity date or if I was doing a renewal. Recently I've just logged into Halifax but I suppose at some point I will loose access to Halifax website and have to go via Lloyds.

Also I am thinking that by mid July 2027 and the maturity date of the Halifax (and BOS) just opened regular savers what will happen to the maturing Halifax regular savers as the name will be gone by then. My 2 LLoyds regular savers I am holding onto until they mature in May 2027 but by then will the choice be just one regular saver with £250 a month ….

In other news

Monmouthshire regular saver 8

Email today regarding maturity on the 28th - it morphs into easy access and you can then open a new Regular saver issue 8 and 6% (unless an issue 9 appears in the next 2 weeks) I think I am going to leave the easy access open with a minimal balance to preserve loyalty

“Create all the happiness you are able to create; remove all the misery you are able to remove. Every day will allow you, --will invite you to add something to the pleasure of others, --or to diminish something of their pains.”6 -

Monmouthshire regular saver 8

Will us OGs who opened the RS8 online when it was initially launched be permitted to open a replacement online too, or do they really expect us to use their app for any new application? What about an application by post?

If not, I fear it will be a case of Sayonara MBS. No point for me holding a low paying access account if applying for anything of any value from them in future is now is limited to via App or in person.

Lots of alternative places to squirrel away a small bit of spare cash paying 6% or more.

Even at 5%, the difference in interest at year end based on maximum deposits of £500 pm is only £30, or less than 9p per day. I'm sure I would survive without them0

{kind=link}

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards