We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

The New Top Easy Access Savings Discussion Area

Comments

-

You're not really looking at this from the perspective of the bank. They have created a new issue at a higher rate because they need to attract some new money and the way to do that is be competetive in the market. It does not help them by just putting up the price of existing funds, which raising the interest rate on the current issue does. By creating a new issue, they attract the funds they need, but those funds are compartmentalised at a specific rate which can be adjusted in the future.

4 -

And some of us are holding earlier Charter issues e.g. 69 (62 as was) at 4.18%.

2 -

Exactly, and such rate adjustments are something Charter Savings Bank have history of.

Only last month I was looking at an ever increasing quantity of their NLA EA accounts I had and wondering which ones to cull as many had been reduced to a common interest rate. But then Charter made it easy for me by renaming some issue numbers. e.g. Issues 58, 63, 64 & 65 were all renamed Issue 57. I managed to cull six Charter EA accounts within the last month alone, and my remaining Issue 57 is looking very vulnerable paying only 3.90% currently.

2 -

Yes, that was quite a recent one from 2 months ago, and hasn't suffered a rate reduction yet.

Issue 68 was the most recent account to be renumbered, back to issue 59.

Edit: Are you sure your Issue 69 was your former Issue 62?

My former Issue 62 was renamed Issue 59 (like former Issue 68)

Or do you mean you ditched & switched your former Issue 62 for an Issue 69 when it was on sale?

0 -

'Or do you mean you ditched & switched your former Issue 62 for an Issue 69 when it was on sale?'

Good spot @gpman I did indeed do that. Apologies if I confused anyone. Including myself!

1 -

Thank you. I was looking at the Yorkshire savings accounts yesterday and completely missed this one.

0 -

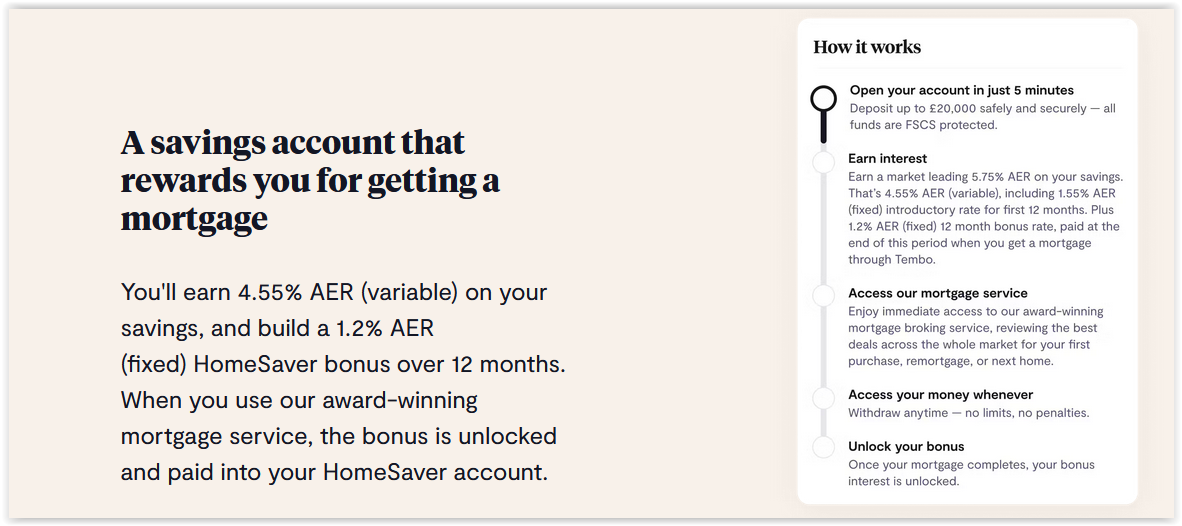

Tembo Home Saver currently 4.55% AER (if i'm not mistaken)

2 -

You only get this rate if you take out a Tembo mortgage in 12 months time, and on £20k max.

0

0 -

I don't believe you need to take out a Tembo Mortgage to earn the 4.55% (3% + 1.55% introductory Rate), just keep the account open for 12 months. The additional bonus rate of 1.2% is conditional on taking out a mortgage through them.

"5.75% AER (Variable), including conditional bonuses, comprised of:A) Base Rate: 3.00% AER (variable). Interest is earned daily and paid on the 8th working day of the following month.

B) 12-Month Introductory Rate: 1.55% AER fixed bonus, earned daily for 12 months from applying to open the account and paid if the account stays open for 12 months; and

C) Home Saver Bonus: 1.20% AER fixed bonus, earned daily for 12months from the date you submit your application to open your Home Saver account, and paid if you complete a qualifying mortgage through Tembo Money Limited within 3 years from the date of account opening."

0 -

Max a/c balance is £25K. The 3.00+1.55% bonus are not dependent on taking out a mortgage, only the additional 1.20% mortgage bonus is.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards