We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The New Top Easy Access Savings Discussion Area

Comments

-

Kent Reliancenottsphil said:

Obviously I know that.chris_the_bee said:

Kent Reliancenottsphil said:

Thanks, I'll go through thesejanusdesign said:nottsphil said:

My instant access money is earning 4.75% AER but it doesn't qualify for the list as it contravenes two of the criteria, the reason I am looking for a second one. At the time you compiled it however, the Saffron Building Society was offering it's E-Saver at 4.5%, so was its exclusions solely because of its £10 minimum balance?ircE said: True EA accounts are easy access savings accounts which can be opened (and the headline interest rate earned) from £1 and allow for unlimited deposits and withdrawals. This excludes accounts that are limited to smaller balances, accounts with fees, and accounts only available via savings platforms. Instant True EA accounts are those True EA accounts which advertise immediate deposit and withdrawal times 24/7. Highlighted entries show changes since last time: blue for new entries to the respective table, and red for rate reductions.cahoot and Hampshire Trust Bank return to the scorecard with their latest offerings. Newcastle BS makes a somewhat unusual debut with an account that matures in 6 months - just in time for Christmas.A note on Chip/Chase: their battle continues more than what is shown on the scorecard, which only goes by what I see on moneyfacts for my selected filters. Chip is offering a 4.76% account with limited access to new customers, and Chase is offering selected existing customers a boosted rate of 4.80%. DYOR etc.For those who care neither for Chip nor Chase, Chetwood provides the leading account for True EA accounts, and cahoot takes the lead for those who would like instant access.The MPC announces its next decision next Thursday, 8th May.it will be because of that - personally, I think those criteria are silly (no offence to irce) - but I guess if you want to have criteria, you have to draw the line somewhere... I wouldn't have chose there, but hey ho... the only use for me is to see which ones are considered "instant".Does anyone know of any other accounts that would make this list but for a petty minimum balance requirement?

True EA accounts are easy access savings accounts which can be opened (and the headline interest rate earned) from £1 and allow for unlimited deposits and withdrawals. This excludes accounts that are limited to smaller balances, accounts with fees, and accounts only available via savings platforms. Instant True EA accounts are those True EA accounts which advertise immediate deposit and withdrawal times 24/7. Highlighted entries show changes since last time: blue for new entries to the respective table, and red for rate reductions.cahoot and Hampshire Trust Bank return to the scorecard with their latest offerings. Newcastle BS makes a somewhat unusual debut with an account that matures in 6 months - just in time for Christmas.A note on Chip/Chase: their battle continues more than what is shown on the scorecard, which only goes by what I see on moneyfacts for my selected filters. Chip is offering a 4.76% account with limited access to new customers, and Chase is offering selected existing customers a boosted rate of 4.80%. DYOR etc.For those who care neither for Chip nor Chase, Chetwood provides the leading account for True EA accounts, and cahoot takes the lead for those who would like instant access.The MPC announces its next decision next Thursday, 8th May.it will be because of that - personally, I think those criteria are silly (no offence to irce) - but I guess if you want to have criteria, you have to draw the line somewhere... I wouldn't have chose there, but hey ho... the only use for me is to see which ones are considered "instant".Does anyone know of any other accounts that would make this list but for a petty minimum balance requirement?- Cahoot @ 5% is an option if you want to throw in a maximum of £3,000 - it only requires £1 to open, but would fail the above list because it has a "smaller balance".

- existing, and eligible, Chase users might be able to open a 4.8% boosted account for 6 months.

- Vida Savings (never used) is at 4.63% with a £10 opening... fails because it's not £1 to open.

- Kent Reliance is 4.5% if you have £1,000 to open it with (you might need to define what you think is a "petty" balance!) - you can drop the balance down to £1, but would then only receive a nominal interest rate.

Cahoot 5% - I already have one

Chase - requires current account.

Vida - a gem whose petty minimum has denied it a place! (Seriously, does @ircE think anybody would actually find that onerous? These aren't children's accounts!)

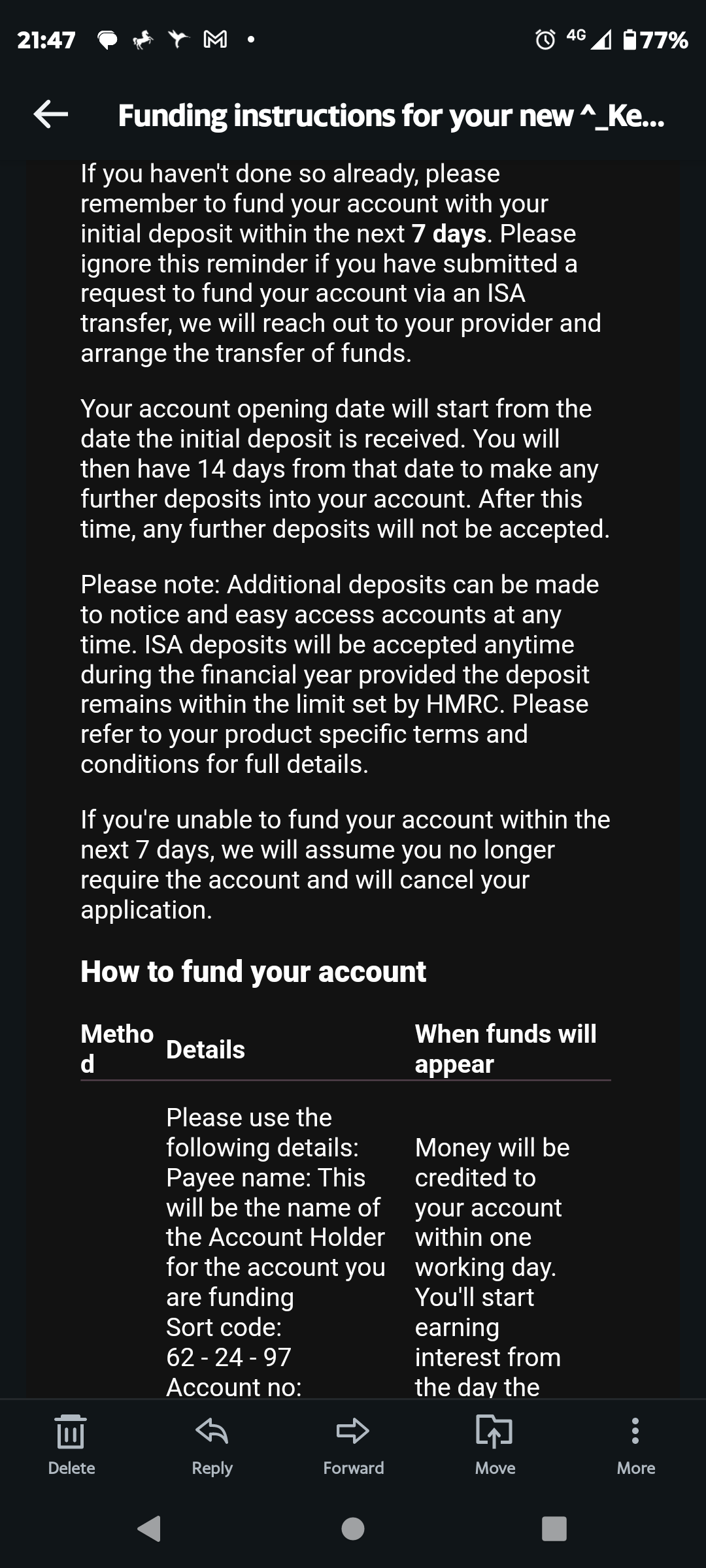

Kent Reliance - you can't pay into it after 14 days, or at least that's what I thought as I read this email (fuming!) so I didn't bother reading any further. Looking at it again though, it completely contradicts itself from the next sentence! So, which is correct?

(OK, so I don't know how to do bullet points on Android ☺️)

However, the 4th paragraph above does state:-

Please note: Additional deposits can be made to notice and easy access accounts at any time.

The question was, "which is correct?"

If you have a notice or easy access account, then paragraph 4 applies and is correct. However, if you have any other type of account, then paragraph 3 applies and is correct.0 -

Anyone had issues with Oaknorth Bank? I have tried several times today to close my 95 day notice account following a rate cut from 4.62 to 4.37. Each time, I receive a message saying that my withdrawal didn't go through, without any explanation. Have tried calling but can't get through.0

-

Update: Finally got through to Oaknorth - there is a glitch in their system but they have agreed to raise the withdrawal manually.Sherbertfizz said:Anyone had issues with Oaknorth Bank? I have tried several times today to close my 95 day notice account following a rate cut from 4.62 to 4.37. Each time, I receive a message saying that my withdrawal didn't go through, without any explanation. Have tried calling but can't get through.1 -

Not seeing a rate cut on my 95 day notice account. It’s still at 4.64% at the moment. This one’s on Issue 4.Sherbertfizz said:Anyone had issues with Oaknorth Bank? I have tried several times today to close my 95 day notice account following a rate cut from 4.62 to 4.37. Each time, I receive a message saying that my withdrawal didn't go through, without any explanation. Have tried calling but can't get through.0 -

Chase, quick off the mark as suspected.

https://www.chase.co.uk/gb/en/

Our saver interest rate is changingBecause the Bank of England has recently reduced its base rate, the standard Chase saver variable rate will change from 3.00% AER (2.96% gross) to 2.75% AER (2.72% gross), effective from 15 May 2025.

So for those of us who got recent boost to 4.8% will be 4.55% from 15th May.11 -

This thread's not for notice accounts.MichaelAP said:

Not seeing a rate cut on my 95 day notice account. It’s still at 4.64% at the moment. This one’s on Issue 4.Sherbertfizz said:Anyone had issues with Oaknorth Bank? I have tried several times today to close my 95 day notice account following a rate cut from 4.62 to 4.37. Each time, I receive a message saying that my withdrawal didn't go through, without any explanation. Have tried calling but can't get through.0 -

I assume that these are "95 day notice base rate tracker" accounts. The clue's in the name. Shouldn't come as any surprise that the saving rates are down 0.25%.MichaelAP said:

Not seeing a rate cut on my 95 day notice account. It’s still at 4.64% at the moment. This one’s on Issue 4.Sherbertfizz said:Anyone had issues with Oaknorth Bank? I have tried several times today to close my 95 day notice account following a rate cut from 4.62 to 4.37. Each time, I receive a message saying that my withdrawal didn't go through, without any explanation. Have tried calling but can't get through.0 -

I've put 15th May in my diary a couple of days agoToastLady said:Chase, quick off the mark as suspected.https://www.chase.co.uk/gb/en/

Our saver interest rate is changingBecause the Bank of England has recently reduced its base rate, the standard Chase saver variable rate will change from 3.00% AER (2.96% gross) to 2.75% AER (2.72% gross), effective from 15 May 2025.

So for those of us who got recent boost to 4.8% will be 4.55% from 15th May.") Now just need to watch the shaw, most of EAs will be dropping rates very soon (GB has already announced it on 29 April). I hope Cahoot will stick to their 60-days notice - I've got a space for £12k in Sunny Days @4.75%... I won't be surprised if in a couple of weeks time Chase's 4.55% will become the best home for EA cash again.

Now just need to watch the shaw, most of EAs will be dropping rates very soon (GB has already announced it on 29 April). I hope Cahoot will stick to their 60-days notice - I've got a space for £12k in Sunny Days @4.75%... I won't be surprised if in a couple of weeks time Chase's 4.55% will become the best home for EA cash again.

1 -

The GB Bank cut already announced is 4.7% down to 4.35% effective 13:05:25.allegro120 said:

I've put 15th May in my diary a couple of days agoToastLady said:Chase, quick off the mark as suspected.https://www.chase.co.uk/gb/en/

Our saver interest rate is changingBecause the Bank of England has recently reduced its base rate, the standard Chase saver variable rate will change from 3.00% AER (2.96% gross) to 2.75% AER (2.72% gross), effective from 15 May 2025.

So for those of us who got recent boost to 4.8% will be 4.55% from 15th May. Now just need to watch the shaw, most of EAs will be dropping rates very soon (GB has already announced it on 29 April). I hope Cahoot will stick to their 60-days notice - I've got a space for £12k in Sunny Days @4.75%... I won't be surprised if in a couple of weeks time Chase's 4.55% will become the best home for EA cash again. 1 -

Mine is Issue 2. Had notification today, rate drops tomorrow (9/5)MichaelAP said:

Not seeing a rate cut on my 95 day notice account. It’s still at 4.64% at the moment. This one’s on Issue 4.Sherbertfizz said:Anyone had issues with Oaknorth Bank? I have tried several times today to close my 95 day notice account following a rate cut from 4.62 to 4.37. Each time, I receive a message saying that my withdrawal didn't go through, without any explanation. Have tried calling but can't get through.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards