We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

This time I will do well

Cheesephetamine

Posts: 247 Forumite

I had a debt free diary here in 2019... It did not last for long...

I started a DMP in late 2019 due to me having accumulated debts up to 38K. My debts are 100% due to my poor mental health. I cannot make any excuses really. It is my fault and only my fault that I got myself in this situation so I am not going to try and excuse myself or anything of the sort.

I have been slowly paying the debts I have in my DMP and I am now down to 20K which is alright I guess! However... I have continued to accumulate debt on the side... mainly: clearpay, a store account and a payday loan. I swear I never learn...

Last week, when I realised it was the first time that I could actually not make my monthly payment rent (I have always paid my utility bills, rent and council tax on time), I told myself: get a bloody grip, this is not the way to go forward, you really need to get your stuff sorted!

So, I spoke to my landlord and made a deal with him (I have paid the outstanding today so that is now behind me), I have had a good hard look at my spendings and I have decided to finish my mobile phone contract early. I has paying 200 pounds for my bloody mobile phone!!!! I must be STUPID. Of course that comes with a penalty and I am talking to EE to set up a payment plan. So basically I will be paying 50 instead of 200... Its gonna take ages to pay the outstanding but at least I think this will help me on my day to day, especially if I am able to not incur any more debt...

Today I paid off my clearpay, so thats one less thing to worry about.

A couple of things I have done since I realise I was out of control again:

-Read a lot of MSE articles

-Moved my mobile number to lebara and struck a deal of 13GB for 1.99 for 5 months (compare that to my 200+ from EE X''D )

-Opened a loqbox and started putting 20 quid away to save and try to work on my credit score (which is basically nonexistant)

-Opened a chase account and a curve card and moved all my money and direct debits there. I want to use the 1% cashback. 5% on roundups and 1.5% on savings for as long as I can. It will not be a lot but it is more than the 0 I am getting now.

-Removed myself from the joint account I have with my husband so his credit score doesn't suffer (his is amazing, I wish I could be like him!)

-Had a look and cancelled a couple of subscriptions, apps etc that I did not use, same with old direct debits and other spendings

-Removed all card details from my chrome, autofill, shopping websites and such

-Unsubscribed from all triggering emails and closed a couple of site accounts

I am currently paying:

-1000 to the household account from where we pay rent, bills and groceries (my husband pays another 1000 monthly)

- 815 to my DMP

- 20 to loqbox

- 50 to a chase savings account at 1.5%

I earn around 2400 clean a month from PIP and income, so I do not understand where all my money is going. I have never in my life finished a month with money in my account. (I am 40...) I hope that, if I can control myself, I will be able to put a bit more in my savings at the end of the month and do lump sum payments into my DMP often.

Ah! regarding my mental health... I am working with a psychologist, I am diagnosed with C-PTSD, aspergers, ADHD, bulimia, dermatillomania

I wonder if it's worth trying to talk to my creditors about my mental health. Not that I want to avoid paying (I don't) but it might be of benefit? what do you all think? Am I missing anything important I should be doing to not get more debt AND pay the one I have??

I started a DMP in late 2019 due to me having accumulated debts up to 38K. My debts are 100% due to my poor mental health. I cannot make any excuses really. It is my fault and only my fault that I got myself in this situation so I am not going to try and excuse myself or anything of the sort.

I have been slowly paying the debts I have in my DMP and I am now down to 20K which is alright I guess! However... I have continued to accumulate debt on the side... mainly: clearpay, a store account and a payday loan. I swear I never learn...

Last week, when I realised it was the first time that I could actually not make my monthly payment rent (I have always paid my utility bills, rent and council tax on time), I told myself: get a bloody grip, this is not the way to go forward, you really need to get your stuff sorted!

So, I spoke to my landlord and made a deal with him (I have paid the outstanding today so that is now behind me), I have had a good hard look at my spendings and I have decided to finish my mobile phone contract early. I has paying 200 pounds for my bloody mobile phone!!!! I must be STUPID. Of course that comes with a penalty and I am talking to EE to set up a payment plan. So basically I will be paying 50 instead of 200... Its gonna take ages to pay the outstanding but at least I think this will help me on my day to day, especially if I am able to not incur any more debt...

Today I paid off my clearpay, so thats one less thing to worry about.

A couple of things I have done since I realise I was out of control again:

-Read a lot of MSE articles

-Moved my mobile number to lebara and struck a deal of 13GB for 1.99 for 5 months (compare that to my 200+ from EE X''D )

-Opened a loqbox and started putting 20 quid away to save and try to work on my credit score (which is basically nonexistant)

-Opened a chase account and a curve card and moved all my money and direct debits there. I want to use the 1% cashback. 5% on roundups and 1.5% on savings for as long as I can. It will not be a lot but it is more than the 0 I am getting now.

-Removed myself from the joint account I have with my husband so his credit score doesn't suffer (his is amazing, I wish I could be like him!)

-Had a look and cancelled a couple of subscriptions, apps etc that I did not use, same with old direct debits and other spendings

-Removed all card details from my chrome, autofill, shopping websites and such

-Unsubscribed from all triggering emails and closed a couple of site accounts

I am currently paying:

-1000 to the household account from where we pay rent, bills and groceries (my husband pays another 1000 monthly)

- 815 to my DMP

- 20 to loqbox

- 50 to a chase savings account at 1.5%

I earn around 2400 clean a month from PIP and income, so I do not understand where all my money is going. I have never in my life finished a month with money in my account. (I am 40...) I hope that, if I can control myself, I will be able to put a bit more in my savings at the end of the month and do lump sum payments into my DMP often.

Ah! regarding my mental health... I am working with a psychologist, I am diagnosed with C-PTSD, aspergers, ADHD, bulimia, dermatillomania

I wonder if it's worth trying to talk to my creditors about my mental health. Not that I want to avoid paying (I don't) but it might be of benefit? what do you all think? Am I missing anything important I should be doing to not get more debt AND pay the one I have??

TOTAL DEBT JUNE 2019: £38,233.87 Aiming debt free mid 2023. All bad debt written off / paid by January 2023. No missed payments in 2023. Only one active credit card to pay off! I DID IT 🎉

2

Comments

-

Hi there,good luck and well done for coming back!

I also struggle with my mental health, I think an awful lot of people on here will understand completely!!

I have told my creditors about it, and they were very understanding and worked with me to come up with a plan, and when I messed up and missed a payment they were maybe more gentle in their response if that makes sense?

I found when my debt was at its worst and I was bombarded by phone calls and letters from creditors I was also at my lowest mentally and even responding to a phone call was beyond what I could cope with,even though I knew how important it was.

It’s a horrible trap, I wish you well xx3 -

wishing you all the best I will be cheering you on.1

-

Welcome back and good luck! Likewise will be cheering you on. No point beating yourself up about anything. We have all been there with not making good decisions sometimes! Sounds like you have taken some great first steps.

Debt free November 20222 -

Thank you all! To be honest I can’t fault any of my creditors. Since I started my dmp in 2019 they have not called me or harrashed me at all. I get the odd letter here and there just with a summary of how things are going and such, always with the indication that they are only doing so as they are asked to by law. I have missed a couple of payments on months I was struggling and they have been understanding… also everyone stopped interests as soon as I started the dmp so all in all I feel lucky. It was definitely worse when I tried to manage it myself. Stepchange have been lifesavers for this reason. I just need to learn to not spend if I don’t need to!!!TOTAL DEBT JUNE 2019: £38,233.87 Aiming debt free mid 2023. All bad debt written off / paid by January 2023. No missed payments in 2023. Only one active credit card to pay off! I DID IT 🎉0

-

Do you keep a spending diary to figure out where yourmoney is going each month?1

-

Yes I do use an app called goodbudget that is like a virtual envelope system as well as using different "pots" in my chase bank account for different things. I have 4 pots: my bills, my spending, my household bills and the household spending (mainly groceries). This way I can see exactly how much money I have available on each.TOTAL DEBT JUNE 2019: £38,233.87 Aiming debt free mid 2023. All bad debt written off / paid by January 2023. No missed payments in 2023. Only one active credit card to pay off! I DID IT 🎉1

-

Hi, just started reading your diary.Is your hubby aware of your debt? Does something trigger your spending , is your job stressful maybe after a rubbish day do you just want to buy something.I’ve read a few other diaries where people give themselves a certain amount to spend each week and when it’s gone that’s it, maybe something you could try.Sounds like your on the right path, I’ll be cheering you along. Good luck.1

-

One thing that might help - realise the difference between "need" and "want". Don't buy the latter!

Obviously you need food, water and the dull stuff (as we all do) but things we want - well, we can manage without.Now a gainfully employed bassist again - WooHoo!1 -

My husband knows about my debt, yes. I do know the difference between wanting and needing, but is not that simple or easy. An addict also knows that they don't need the drug, they just want it, but it's still difficult for them not to take itTOTAL DEBT JUNE 2019: £38,233.87 Aiming debt free mid 2023. All bad debt written off / paid by January 2023. No missed payments in 2023. Only one active credit card to pay off! I DID IT 🎉1

-

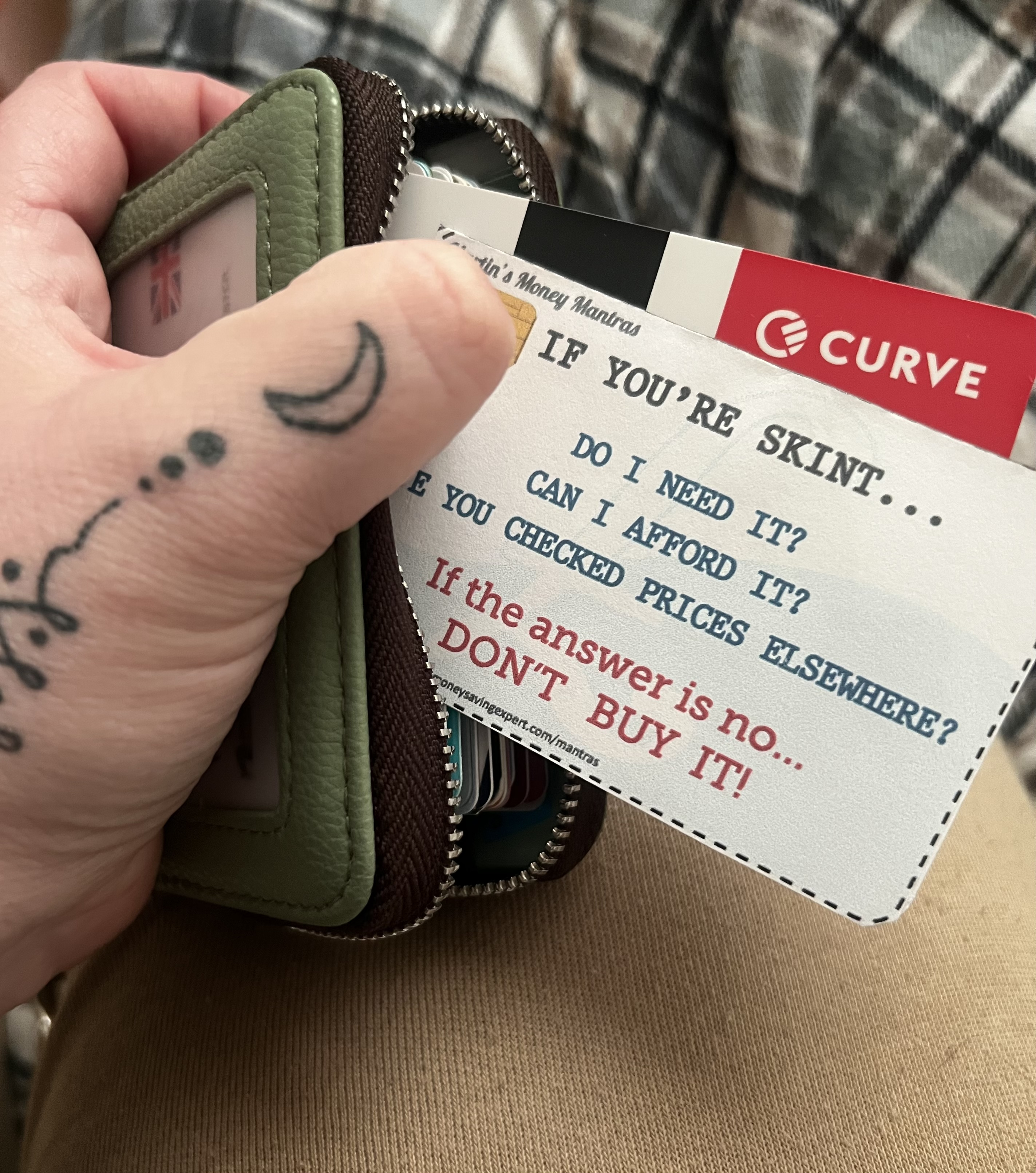

So! Welcome May. New month. New me? It’s my bday month 😣

today I cleaned my wallet out and kept the loyalty cards / discounts I use more alongside my curve card. All other credit cards and debit cards are stocked away in a drawer. In the slot where I keep my curve card I added the money mantras in the hope that they will help me stop and think when I’m about to spend money.

joined some challenges and created my own! (Check my signature) and I’m feeling very positive today to be honest.Calm day today at home and still off sick so mainly lying down reading and signing up for survey websites (earned £1.35 already on one!)

Counting today as a NSD as not going out and I’ve blocked my card from spending online")

oh! And I requested all 3 CRA to write a NOC in my score so I will not be given more credit for the time being… I hope I can continue with this positive vibe. PTOTAL DEBT JUNE 2019: £38,233.87 Aiming debt free mid 2023. All bad debt written off / paid by January 2023. No missed payments in 2023. Only one active credit card to pay off! I DID IT 🎉6

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards