We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Top Easy Access Savings Discussion Area

Comments

-

Tandem pays 4.89% gross (monthly) which equates to 5.00% AER.invuk said:Pretty dumb question but hopefully someone can answer it for me. I currently have a Tandem instant saver paying 5% and have just applied for a Cahoot simple saver which pays 5.12%. Cahoot only pays 5% interest if interest is paid monthly. Does this mean they both pay the same if monthly interest is chosen?

Cahoot pays 5.00% gross (when the monthly option is chosen) which equates to 5.12% AER

Whether you withdraw the interest or leave it in the account to compound, you'll get more with the Cahoot account.3 -

Both Tandem and Cahoot (and every other lender/product) will quote an APR to allow rates to be compared on a like-for-like basis. The Cahoot 5% figure is the rate if the interest is paid away each month (aka the gross interest rate). If the interest were left to compound in the account then the effective rate is 5.12% over a year (the Annual Percentage Rate and the gross rate for the annual interest product).invuk said:Pretty dumb question but hopefully someone can answer it for me. I currently have a Tandem instant saver paying 5% and have just applied for a Cahoot simple saver which pays 5.12%. Cahoot only pays 5% interest if interest is paid monthly. Does this mean they both pay the same if monthly interest is chosen?

I haven't looked up the numbers for the Tandem product.1 -

Thanks guys really appreciate the time and effort for all the responses

") Just one last question, if you choose monthly over 12-month interest does it always work out the same or do you get more if you choose the annual option? 0

Just one last question, if you choose monthly over 12-month interest does it always work out the same or do you get more if you choose the annual option? 0 -

It works out the same.invuk said:Thanks guys really appreciate the time and effort for all the responses Just one last question, if you choose monthly over 12-month interest does it always work out the same or do you get more if you choose the annual option?1 -

Only if you keep the funds in there for the full 12 months, if you were to "exit" i.e. close down the account and have the accrued interest paid, then the annual option would yield a tiny bit more than the monthly option.allegro120 said:

It works out the same.invuk said:Thanks guys really appreciate the time and effort for all the responses Just one last question, if you choose monthly over 12-month interest does it always work out the same or do you get more if you choose the annual option?

To give you an idea of how tiny, by my workings, a maximum possible difference of 0.0305% of the principal would be yielded if "exiting" at exactly the mid-point of the 12-month period. At a principal equal to the £85k FSCS limit this would be a maximum possible difference of £25.89.

So unless you need the monthly interest to be accessible (e.g. as a supplementary income, to feed a regular saver, etc), it might be slightly better to go with annual interest on an easy access account, and then:

- "exiting" immediately if a better interest rate comes along, and then re-apply the same logic with a new account

- "exiting" at the precise 6-month point if the same interest rate is available in a new account

- keeping the account going if the interest rate remains better than anything else available in the market

3 -

Nor existing now, NLA when logged in.poppystar said:

Not there for new customers. Sadly I left it until today to apply🙁soulsaver said:

Source...?BlackthornU said:Beehive Money 5.2% NLA

Still available to me when logged in - which may mean limited to existing customers?0 -

I dont thinks that's true, both will yield exactly the same over any period, as long as the interest is not taken out. I believe your workings are based on the interest rate quoted for monthly interest, but the bank has it just rounded to 2dp, whereas in reality it is many dp.intalex said:

Only if you keep the funds in there for the full 12 months, if you were to "exit" i.e. close down the account and have the accrued interest paid, then the annual option would yield a tiny bit more than the monthly option.allegro120 said:

It works out the same.invuk said:Thanks guys really appreciate the time and effort for all the responses Just one last question, if you choose monthly over 12-month interest does it always work out the same or do you get more if you choose the annual option?

To give you an idea of how tiny, by my workings, a maximum possible difference of 0.0305% of the principal would be yielded if "exiting" at exactly the mid-point of the 12-month period. At a principal equal to the £85k FSCS limit this would be a maximum possible difference of £25.89.

So unless you need the monthly interest to be accessible (e.g. as a supplementary income, to feed a regular saver, etc), it might be slightly better to go with annual interest on an easy access account, and then:

- "exiting" immediately if a better interest rate comes along, and then re-apply the same logic with a new account

- "exiting" at the precise 6-month point if the same interest rate is available in a new account

- keeping the account going if the interest rate remains better than anything else available in the market 2

2 -

martinm1 said:

I dont thinks that's true, both will yield exactly the same over any period, as long as the interest is not taken out. I believe your workings are based on the interest rate quoted for monthly interest, but the bank has it just rounded to 2dp, whereas in reality it is many dp.intalex said:

Only if you keep the funds in there for the full 12 months, if you were to "exit" i.e. close down the account and have the accrued interest paid, then the annual option would yield a tiny bit more than the monthly option.allegro120 said:

It works out the same.invuk said:Thanks guys really appreciate the time and effort for all the responses Just one last question, if you choose monthly over 12-month interest does it always work out the same or do you get more if you choose the annual option?

To give you an idea of how tiny, by my workings, a maximum possible difference of 0.0305% of the principal would be yielded if "exiting" at exactly the mid-point of the 12-month period. At a principal equal to the £85k FSCS limit this would be a maximum possible difference of £25.89.

So unless you need the monthly interest to be accessible (e.g. as a supplementary income, to feed a regular saver, etc), it might be slightly better to go with annual interest on an easy access account, and then:

- "exiting" immediately if a better interest rate comes along, and then re-apply the same logic with a new account

- "exiting" at the precise 6-month point if the same interest rate is available in a new account

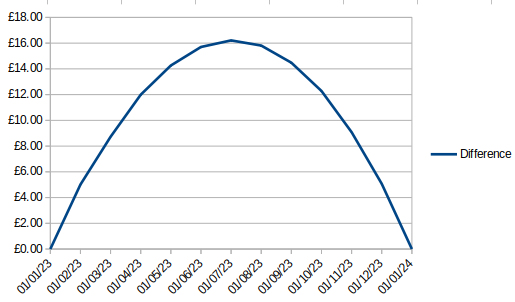

- keeping the account going if the interest rate remains better than anything else available in the marketActually it is true. For a static balance, the annual option gives a linear increase in accrued interest over the whole year, while the monthly option starts at a lower gross rate and has a slight upward curve over time (due to compounding). So for accounts with the same AER and monthly vs annual interest, over periods of less than a year you'll earn slightly more from the annual option as you'll be on the shallower end of the curve. The only time annual vs monthly with the same AER earn exactly the same is when saving over exactly 1 year (or 2 years etc), as this is the point when monthly catches up with annual. Any fractions of a year will lead to a difference.Remember that interest accrues daily at a rate of 1/365 x gross rate on the closing balance of the account, and the gross rate is different between monthly and annual variants. No amount of extra precision will make them the same.Here's a table and plot of the relative outcomes when closing the respective accounts on the first of each month (based on Paragon double access 5.16%), you can only just see the gap between the lower blue curve and upper red line in the plot:

9 -

May be worth plotting only the difference between the 2 columns, would show the proper U-curvemasonic said:Here's a table and plot of the relative outcomes when closing the respective accounts on the first of each month (based on Paragon double access 5.16%), you can only just see the gap between the lower blue curve and upper red line in the plot:4 -

intalex said:

May be worth plotting only the difference between the 2 columns, would show the proper U-curvemasonic said:Here's a table and plot of the relative outcomes when closing the respective accounts on the first of each month (based on Paragon double access 5.16%), you can only just see the gap between the lower blue curve and upper red line in the plot:Good idea, and indeed it does: 5

5

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.3K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 248K Work, Benefits & Business

- 605.2K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards