We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Top Regular Savers Discussion Thread

Comments

-

If this helps I tried to withdraw from mine and got an email from them almost immediately saying that I couldn't withdraw, but that if I went back in to my account and clicked to close the account, my funds would be sent to my nominated account. I did this and the funds were available in my nominated account the next morning.castle96 said:CHORLEY RS 5.15%v

Iv'e read their T&Cs and still cant make out if you can withdraw or close account... A) because you just wish to and") if they reduce the rate TIA

if they reduce the rate TIA

I had £2800 in it, they added £50.41 interest - it was due to mature on the 31st January 2026 xxx3 -

Received my Scottish Building Society pass book in the post. How cute, takes me back. Didn't realise such things still existed !

3

3 -

Scottish BS

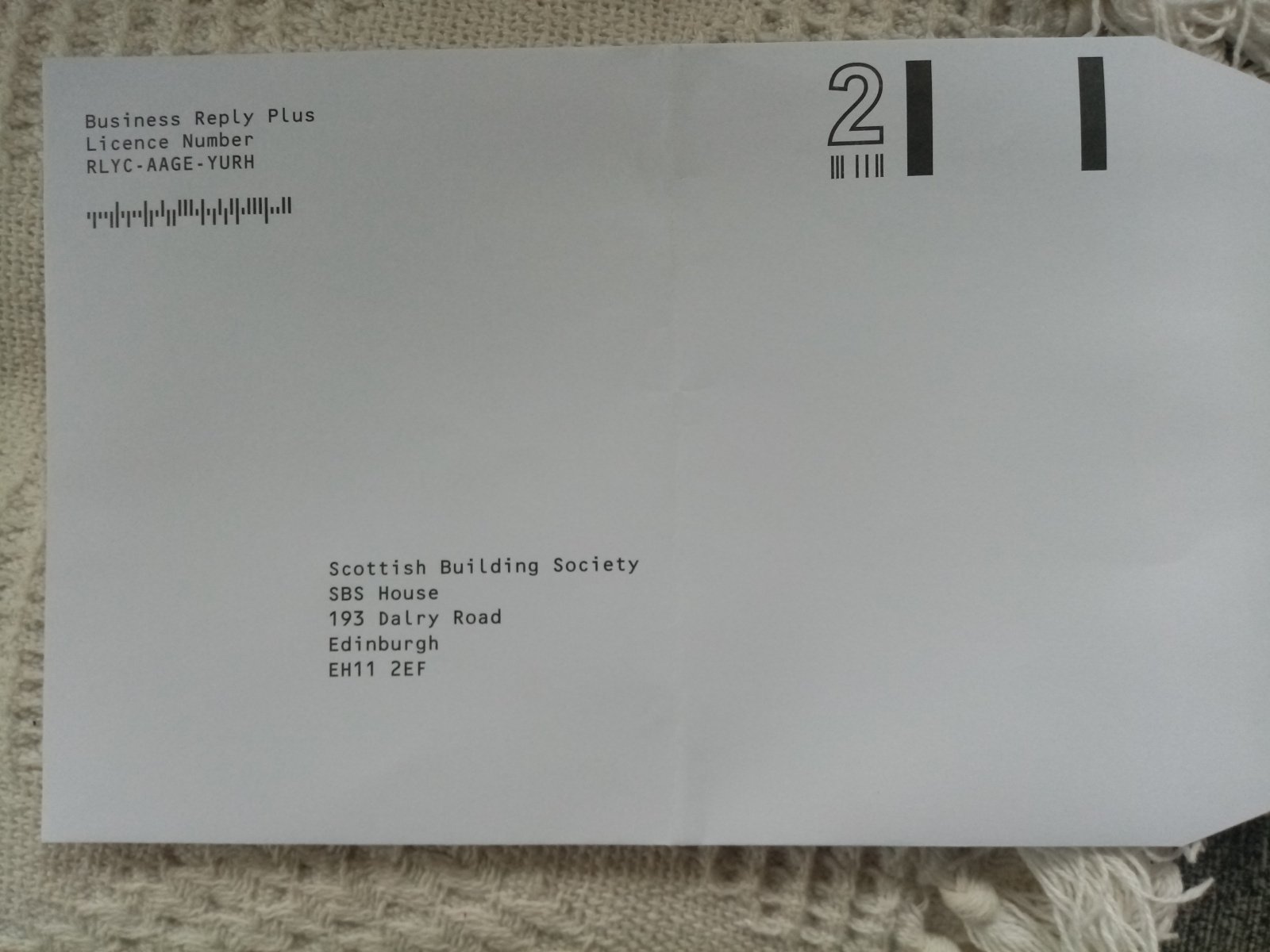

Going to apply for their RS via post - got my printed & completed form, photocopy of driving licence, & cheque ready. Now just to decide whether to pay for a stamp or ask them to post me a pre-paid envelope.

For people saying to use a Freepost licence number/address - how do you do that? Any successes with that approach? According to the below from Royal Mail handwriting is not allowed since 30th of March 2015 unless business uses "Freepost NAME" service - and Scottish BS seems not to have that as they use a licence number? https://www.royalmail.com/sites/royalmail.com/files/2022-09/response-services-user-guide_september-2022.pdf0 -

Sorry - "The Quaker" - I do not get sentimental with passbooks. I have a number of passbook RS`s including this one and they only add to admin. At least Scottish BS do online so ,after initial postal baloney, their RS can be managed easily. Lets hope the Maturity process doesn`t require posting in the passbook.1

-

where_are_we said:Sorry - "The Quaker" - I do not get sentimental with passbooks. I have a number of passbook RS`s including this one and they only add to admin. At least Scottish BS do online so ,after initial postal baloney, their RS can be managed easily. Lets hope the Maturity process doesn`t require posting in the passbook.

Haha, apologies I've not seen one for years. Sounds like the novelty wears off 1

1 -

I received a pre paid envelope from SBSChaykin said:Scottish BS

Going to apply for their RS via post - got my printed & completed form, photocopy of driving licence, & cheque ready. Now just to decide whether to pay for a stamp or ask them to post me a pre-paid envelope.

For people saying to use a Freepost licence number/address - how do you do that? Any successes with that approach? According to the below from Royal Mail handwriting is not allowed since 30th of March 2015 unless business uses "Freepost NAME" service - and Scottish BS seems not to have that as they use a licence number? https://www.royalmail.com/sites/royalmail.com/files/2022-09/response-services-user-guide_september-2022.pdf

Picture attached, if you put licence number on should be ok

0 -

The OH's ISA is now available, so I've moved the £5K from his RS into the ISA. Looks like he'll get interest for 1 day as they credited the transfer I did on Sunday into the RS yesterday.Dizzycap said:Slinky said:Slightly off topic, we tried opening a NatWest ISA for OH yesterday, which although it has issued an account number, hasn't appeared on his account list. Annoyingly I transferred £5K to our joint account yesterday in anticipation of moving it into the ISA. He has a Regular Saver with them which I previously emptied as he's nearing his £500 PSA, so I've just moved the £5K into the RS to see what would happen, and it's accepted the transfer. Will they bounce this back to the joint account I wonder or leave it?It depends when you emptied the NWest RS? I know that you can withdraw funds and replace them within the same month, but not sure about withdrawing and replacing in different months? The Natwest RS may appear to have accept the 5k transfer back and I hope it does; please let us folks on MSE know if it does,but if not; it will eventually after a few days, bounce back into the joint account.From experience of an accidental over payment of £150 into my NW RS, it took 6 days for the overpayment to be returned to my NWest current account.

Make £2025 in 2025

Prolific £1062.50, Octopoints £6.64, TCB £492.05, Tesco Clubcard challenges £89.90, Misc Sales £321, Airtime £70, Shopmium £53.06, Everup £106.08, Zopa CB £30, Misc survey £10

Total £2241.23/£2025 110.7%

Make £2024 in 2024 Total £1410/£2024 70%Make £2023 in 2023 Total: £2606.33/£2023 128.8%0 -

Well I think it's cute and nostalgic. I went to the library yesterday and the self-service machines weren't working so I got my book date-stamped by an actual librarian. It's reassuring that machines haven't completely taken over the world!TheQuaker said:where_are_we said:Sorry - "The Quaker" - I do not get sentimental with passbooks. I have a number of passbook RS`s including this one and they only add to admin. At least Scottish BS do online so ,after initial postal baloney, their RS can be managed easily. Lets hope the Maturity process doesn`t require posting in the passbook.

Haha, apologies I've not seen one for years. Sounds like the novelty wears off3 -

clairec666 said:

Well I think it's cute and nostalgic. I went to the library yesterday and the self-service machines weren't working so I got my book date-stamped by an actual librarian. It's reassuring that machines haven't completely taken over the world!TheQuaker said:where_are_we said:Sorry - "The Quaker" - I do not get sentimental with passbooks. I have a number of passbook RS`s including this one and they only add to admin. At least Scottish BS do online so ,after initial postal baloney, their RS can be managed easily. Lets hope the Maturity process doesn`t require posting in the passbook.

Haha, apologies I've not seen one for years. Sounds like the novelty wears offI'm with you there.Libraries, now that's also a blast from the past !!!3 -

Does Progressive BS send account details by post ?

Has anyone who does not have a device that can do apps managed to use Google Authenticator to login to Progressive with PC/Laptop ?0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.2K Banking & Borrowing

- 254K Reduce Debt & Boost Income

- 454.9K Spending & Discounts

- 246.3K Work, Benefits & Business

- 602.4K Mortgages, Homes & Bills

- 177.9K Life & Family

- 260.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards