We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Octopus Agile

Comments

-

Telegraph_Sam said:

Do you do some kind of a swings & roundabouts calculation? Someone once said there was no such thing as a free lunch. Or is Agile the exception?KevinG said:Dragging the thread back on-topic, we have some lovely low rates tomorrow, including a brief negative at 3pm.Not so much a free lunch as free afternoon tea as it's at 3pm (lunch is still looking pretty cheap though)

I am a Forum Ambassador and I support the Forum Team on the Benefits & tax credits, Heat pumps and Green & Ethical MoneySaving forums. If you need any help on those boards, do let me know. Please note that Ambassadors are not moderators. Any post you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own & not the official line of Money Saving Expert.1 -

All I know is that Agile is significantly cheaper for me than SVR (over 20%) and it is the only Octopus smart tariff I am eligible for as, although I have Solar panels, I have no battery and no EV. If I used a lot of electricity between 4 and 7pm it might be different, but I don't.Telegraph_Sam said:

Do you do some kind of a swings & roundabouts calculation? Someone once said there was no such thing as a free lunch. Or is Agile the exception?KevinG said:Dragging the thread back on-topic, we have some lovely low rates tomorrow, including a brief negative at 3pm.2kWp Solar PV - 10*200W Kioto, SMA Sunny Boy 2000HF, SSE facing, some shading in winter, 37° pitch, installed Jun-2011, inverter replaced Sep-2017 AND Feb-2022.2 -

Not that simple, and not anymore - like GW of renewables under and new nuclear will be under CfD.MikeyPGT said:

My understanding is that the gas generators set the price for everyone even if they are providing only a tiny amount of what is needed so they can rip us off whenever the wind drops or the sun don't shine!JKenH said:Has anyone any idea why electricity prices are so high this evening? We are only using about 14GW of gas and wind isn’t particularly low at over 5GW.

Which is why when last updated afaik in cap letters in Oct Ofgem put renewables CfDs at £27 ex vat wholesale - over 1p/kWh. Down from £30 last summer - c1.2p - when gas gen even lower.0 -

Agile only gets cheap rates to "save the grid" from excess generation capacity caused by over 30GW of unreliable wind and over 10GW of inconsistent solar - renewables. Solar having a notable impact on seasonal midday pricing when looked at agile rates in past.wrf12345 said:"The world doesn't revolve around you. Agile SC remains 1p lower than SVR for me. Nothing naughty about it."

A very small percentage of people had their s/c go up rather than down on variable, London and some other areas, I think, but most people had it go down, although still at an outrageously high level. Agile which saves the Grid at peak times merits zero s/c so current values make no sense.

Standing charges for electric are only so high because of an increase allocation of network costs between 2022 and 24 - and those costs are increasing for electric because of you guessed it - renewables and net zero.

With a share of the £100+ from recent Ofgem £24bn - £15bn of it is gas networks - with £9bn electric plus another £1,x bn imminent - in approvals coming to a mix of SC and unit rates near you, both gas and electric - for the operational costs and capex financing.

And remember that £9bn even adding the £1bn - on electric - less than fifth the low forecast by the 3 TNOs for five years to 2030 of £55bn core and £77bn if plans accelerated as forecast to meet "95% by 2030" and net zero demand increases.

Its unrealistic to expect the dynamic benefits on cheap agile unit rates, then object to the standing charge costs the very same energy sources impose.

And it's dynamic as currently renewables CfDs alone add estimated £27 - 1p/kWh - to wholesale costs under cap pricing. So dragging the average cost up for the majority not on agile.1 -

There is nothing to stop Octopus changing the TOU rates on Agile or Cosy to reflect the lack of s/c income, or to have a new TOU with zero s/c and higher unit rates (geared up when the Grid is in trouble) but let's see where the new zero s/c tariffs end up later this year and whether they fiddle the unit rates at too high a level, as suggested by Ofgem who are maybe under pressure from the Energy Sec who is a self-confessed nerd and likes to look at the detail of things.0

-

They would still have the fixed downstream costs the standing charge is used to fund, so they would need to be sure of actually recouping that from customers taking up the NSC deal. That means the customers would not benefit from doing so and could only lose out if they were higher users, not save if they were low users. In other words, a workable tariff of this type would be attractive to no one, which is probably why it doesn't exist.wrf12345 said:There is nothing to stop Octopus changing the TOU rates on Agile or Cosy to reflect the lack of s/c income, or to have a new TOU with zero s/c and higher unit rates (geared up when the Grid is in trouble) but let's see where the new zero s/c tariffs end up later this year and whether they fiddle the unit rates at too high a level, as suggested by Ofgem who are maybe under pressure from the Energy Sec who is a self-confessed nerd and likes to look at the detail of things.3 -

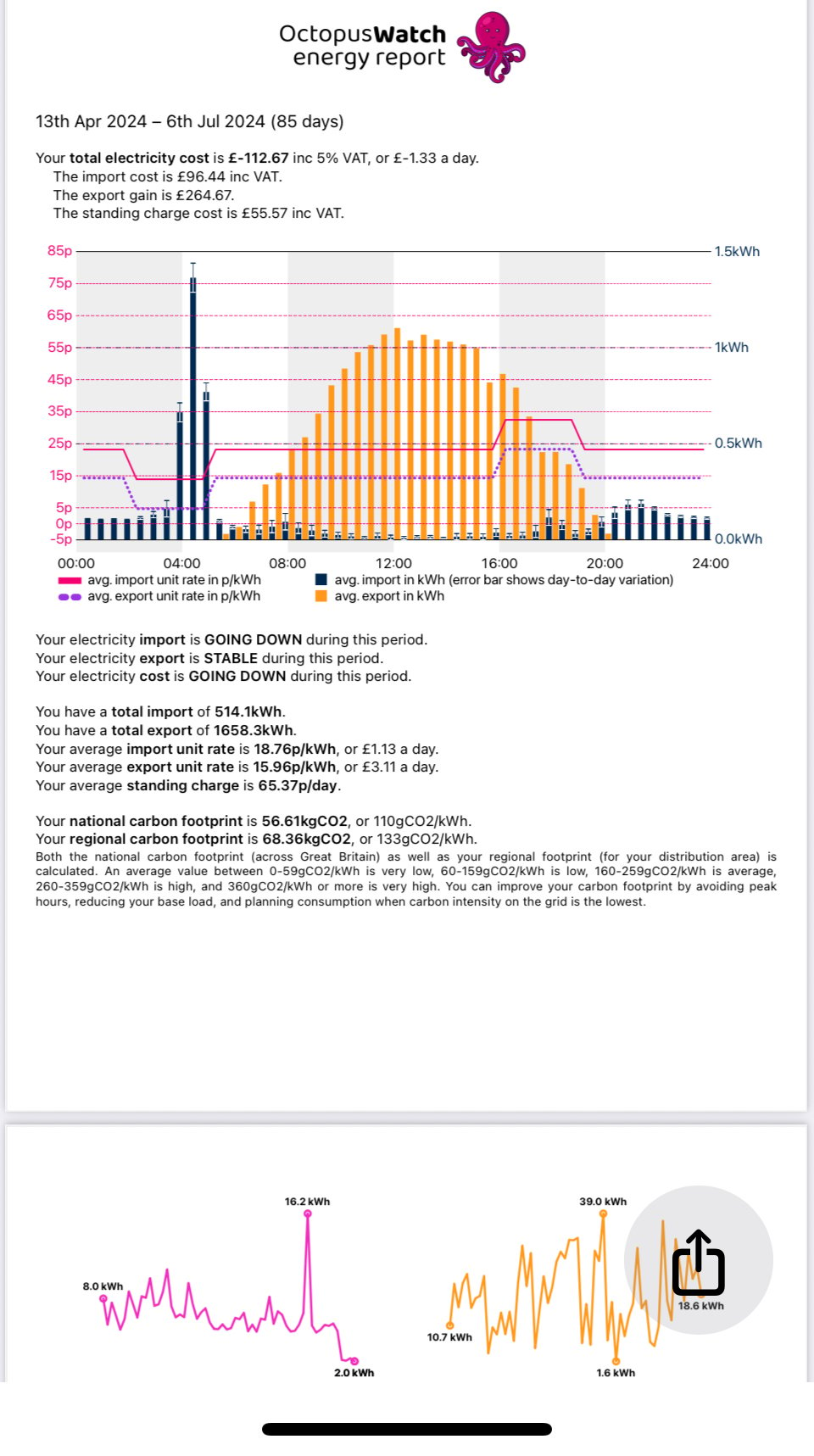

Yesterday I broke my run of 76 negative days (20th April to 5th July). The weather was poor, with a lot of rain and we cooked in the morning for visitors and heated two tanks of hot water. Net import of £1.23.We switched to Agile in 4th April having previously been on Flux. I can only access statistics back to 13 April 2024 so I have done a comparison of 13 April 2024 on Flux vs the same period in 2025 on Agile. Of course it has been a much better spring this year so I would expect my export to be much higher but import similar as my biggest draw from the grid in summer is domestic hot water with a bit of TV in the evening and background consumption (fridge/freezers and set top boxes) from around 8pm to 6am of 175w. This year my import cost has been £62.93 including for 510.7kWh or 74p/day compared to 2024 on Flux of £96.44 for 514.1 kWh or £1.13/day. Add in SC and the average import cost is £1.40/day for Agile in 2025 compared to Flux in 2024 at £1.78/day. Total import cost on Agile in 2025 works out at £119.25 and on Flux in 2024 £152.01. Because if the difference I. Sunshine across the two years I have bothered comparing export.

Northern Lincolnshire. 7.8 kWp system, (4.2 kWwest facing panels , 3.6 kWeast facing), Solis inverters installed 2018, 5kW SSE facing system (shaded in afternoon) added in 2025 with Tesla PW3 battery, Mitsubishi SRK35ZS-S and SRK20ZS-S Wall Mounted A2A Heat Pumps, ex Nissan Leaf owner.2

Northern Lincolnshire. 7.8 kWp system, (4.2 kWwest facing panels , 3.6 kWeast facing), Solis inverters installed 2018, 5kW SSE facing system (shaded in afternoon) added in 2025 with Tesla PW3 battery, Mitsubishi SRK35ZS-S and SRK20ZS-S Wall Mounted A2A Heat Pumps, ex Nissan Leaf owner.2 -

No comments for 2 months! Guess there hasn't been much to say about this tariff for a while but it's still always cheaper than tracker for me, averaging 15% cheaper over the month

What's the predictions for tomorrow? Better than this afternoon?1 -

RavingMad said:No comments for 2 months! Guess there hasn't been much to say about this tariff for a while but it's still always cheaper than tracker for me, averaging 15% cheaper over the month

What's the predictions for tomorrow? Better than this afternoon?The N2EX data suggests it will be better tomorrow. Marginally negative on that auction from 11am-4pm (well 5pm if not for the Agile premium).Likewise I've been able to save vs both Tracker and the E7 fix I gave up to join Agile in June. My usage has been higher due to having to run a newly purchased portable air conditioner more than I would have imagined over the summer. I was in two minds as to whether to bother buying this, but with the summer we've had it was worth every penny! Higher usage meant less of a penalty from the higher Agile standing charge.1 -

Not much point shouting about it to be honest, everyone already on it knows how good it is.My past 150 day average is just under 15p / kWh. Tomorrow should pull that down further too.Just need to work out whether to fully take advantage of the lengthy plunge tomorrow and crack the heating on or leave it as I know of it goes on, the missus will be having it on every day...2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards