We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

EV Discussion thread

Comments

-

Yep, all looks very promising.1961Nick said:

I think that considering the hefty discounting, a gross margin of 19.3% is quite an achievement. The Model 3 is now competing with the likes of the ID3 as well as the ID4 & is still generating a healthy profit. At the end of March, the Model 3 SR was actually £2000 cheaper than the poverty spec ID3 in the UK.Martyn1981 said:

Yes, very true, and the comparison to Toyota doesn't work when net profits are considered, since 10-11% for Tesla is helping to move them towards the top of the list for annual profits, despite far lower sales numbers than the biggest auto groups.1961Nick said:

The problem with trying to compare Tesla with another automaker is that you're either comparing them with an ICEV manufacturer like Toyota or trying to extract the BEV figures from a mix of ICEV & BEV numbers. The only true comparison at the moment is with Ford, but even then there's no detail from the electric division yet other than that they expect to lose $3B this year on top of the $3 they lost in the last 2 years. Tesla have made further price reductions since Ford estimated the loss for this year which won't help the situation.JKenH said:Tesla (TSLA) releases Q1 2023 results: meets expectations, impresses with gross margin

Edit: Edit 2. Average selling price has dropped from around $54k per car in Q1 2022 to $47k in 2023

Edit 2. Average selling price has dropped from around $54k per car in Q1 2022 to $47k in 2023

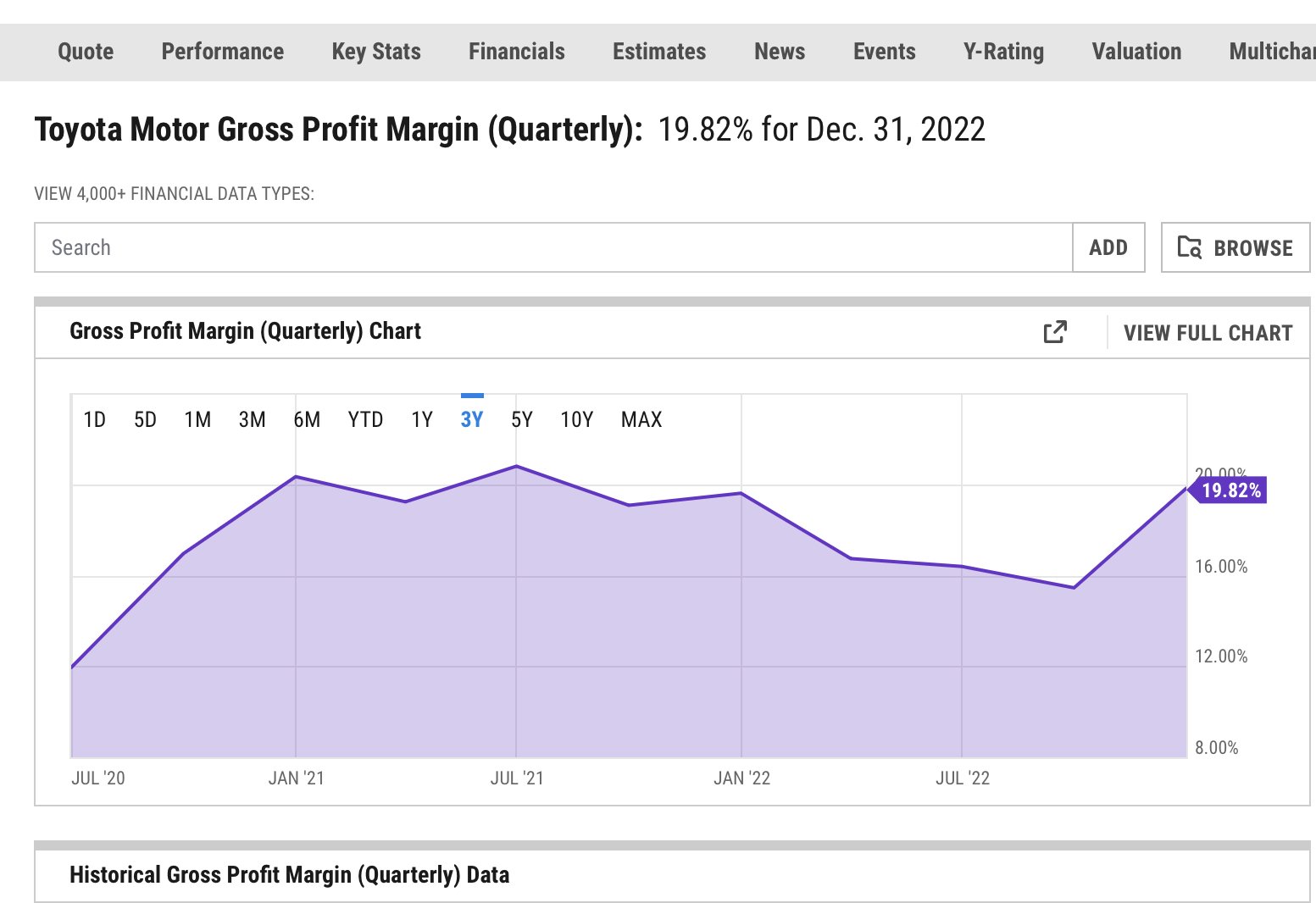

Edit 3: just out of interest here is a comparison of Tesla and Toyota Gross Margins over the last 3 years.

Edit 4: The ASPs quoted in edit 2 were my calculations. Here are alternative figures and comment on the gross margin.

Edit 4: The ASPs quoted in edit 2 were my calculations. Here are alternative figures and comment on the gross margin.The average Tesla vehicle selling price in the first quarter was around $46,850, according to FactSet estimates. That's down from $51,400 in the fourth quarter and $52,100 a year ago.

Auto gross margins excluding regulatory credits and leases declined to 18.3% vs. 23.8% in Q4. That is below the 20% gross margin "floor" Tesla had previously forecast.

Of the Chinese manufacturers, BYD have an impressive market share in China, but when they expand globally they're likely to run straight into reliability, safety & regulatory issues. A battery fire every day might be something that can be supressed in China, but anywhere else it'll be front page news.

Rivian, Lucid & NIO look like money pits with no end in sight. Surely it can't be long before the big legacy auto players start picking them off to fast track their EV ranges & avoid ICEV fines in the process.

Would like to feel slightly smug about the gross margin figure, but actually I think we split the difference between us, when the regulatory credits are removed. [Plus my ~20% guess, was tbh, leaning towards 20+ not 20-.] Zach did explain that missing the 20%+ target was down to the further price cuts in Q1, after his statements on the Q4 earnings call.

Given Tesla's (and BYD's) decision to go for market share, at the cost of gross margin, I suspect legacy auto need to be scared, especially if the 'recession' takes another 12 months to end.

Regarding Rivian and Lucid, totally agree about them being money pits, but in Rivian's defence, they are meeting production targets and growing towards profitability. Combine that with their Amazon sales, and they have a decent chance.

Lucid however, continue to be somewhat of a joke. Having repeatedly reduced their production target last year, eventually down from 20k to 6k-7k, so they could just squeeze above it (~7,100), they continue to only sell about 50% of quarterly production, which is really weird. But ..... they should also be safe, since the Saudi's are willing to back them, and whilst those injections are diluting shareholder value, it does almost look like they are safe ..... in a very weird sort of way?

My overall takeaway was 'middling', not good news, but not terrible news (for Tesla), but I think they've held up far too well to bring any relief to legacy.

What do legacy do now? They have to transition even faster, but with falling (most likely negative) profits on BEV's, they need the ICE sales to fund it. This isn't going to be pretty, but will be fascinating.

Musk clearly wants a 50% y-o-y increase in production & currently price reductions are the only way to achieve that. The launch of the Cybertruck will help add volume in 2024 after which we could see Model 2 deliveries starting. A $25,000 Model 2 must surely have the potential of selling at least 3 million units a year? In the meantime, there's a Model 3/Y facelift due later this year which will freshen up the range & give existing owners a reason to change.

This is slightly tongue-in-cheek, but the further price cuts in the US yesterday, are starting to look less like a price war, and more like a scorched earth policy.

Obviously BEV sales have been growing for a decade, but 2023 may be a year we look back on as when things got 'real'.Mart. Cardiff. 8.72 kWp PV systems (2.12 SSW 4.6 ESE & 2.0 WNW). 28kWh battery storage. Two A2A units for cleaner heating. Two BEV's for cleaner driving.

For general PV advice please see the PV FAQ thread on the Green & Ethical Board.1 -

Well, £25k for a Focus sounds expensive to me.michaels said:25k model 2 still sounds expensive to me, is it Focus size or Fiesta size?

But, in today's prices, that would compete directly with MG4 and Octavia.

I guess it all depends what happens to the overall market price (and availability) for new cars of all types and the extent to which the uplifts for chip shortage etc fall back or are maintained.1 -

Hasn't the tax rebate for the Model 3 just halved to $3750 because the battery is manufactured in China? That could be the reason for the recent price reduction.Martyn1981 said:

Yep, all looks very promising.1961Nick said:

I think that considering the hefty discounting, a gross margin of 19.3% is quite an achievement. The Model 3 is now competing with the likes of the ID3 as well as the ID4 & is still generating a healthy profit. At the end of March, the Model 3 SR was actually £2000 cheaper than the poverty spec ID3 in the UK.Martyn1981 said:

Yes, very true, and the comparison to Toyota doesn't work when net profits are considered, since 10-11% for Tesla is helping to move them towards the top of the list for annual profits, despite far lower sales numbers than the biggest auto groups.1961Nick said:

The problem with trying to compare Tesla with another automaker is that you're either comparing them with an ICEV manufacturer like Toyota or trying to extract the BEV figures from a mix of ICEV & BEV numbers. The only true comparison at the moment is with Ford, but even then there's no detail from the electric division yet other than that they expect to lose $3B this year on top of the $3 they lost in the last 2 years. Tesla have made further price reductions since Ford estimated the loss for this year which won't help the situation.JKenH said:Tesla (TSLA) releases Q1 2023 results: meets expectations, impresses with gross margin

Edit:Edit 2. Average selling price has dropped from around $54k per car in Q1 2022 to $47k in 2023

Edit 3: just out of interest here is a comparison of Tesla and Toyota Gross Margins over the last 3 years.Edit 4: The ASPs quoted in edit 2 were my calculations. Here are alternative figures and comment on the gross margin.The average Tesla vehicle selling price in the first quarter was around $46,850, according to FactSet estimates. That's down from $51,400 in the fourth quarter and $52,100 a year ago.

Auto gross margins excluding regulatory credits and leases declined to 18.3% vs. 23.8% in Q4. That is below the 20% gross margin "floor" Tesla had previously forecast.

Of the Chinese manufacturers, BYD have an impressive market share in China, but when they expand globally they're likely to run straight into reliability, safety & regulatory issues. A battery fire every day might be something that can be supressed in China, but anywhere else it'll be front page news.

Rivian, Lucid & NIO look like money pits with no end in sight. Surely it can't be long before the big legacy auto players start picking them off to fast track their EV ranges & avoid ICEV fines in the process.

Would like to feel slightly smug about the gross margin figure, but actually I think we split the difference between us, when the regulatory credits are removed. [Plus my ~20% guess, was tbh, leaning towards 20+ not 20-.] Zach did explain that missing the 20%+ target was down to the further price cuts in Q1, after his statements on the Q4 earnings call.

Given Tesla's (and BYD's) decision to go for market share, at the cost of gross margin, I suspect legacy auto need to be scared, especially if the 'recession' takes another 12 months to end.

Regarding Rivian and Lucid, totally agree about them being money pits, but in Rivian's defence, they are meeting production targets and growing towards profitability. Combine that with their Amazon sales, and they have a decent chance.

Lucid however, continue to be somewhat of a joke. Having repeatedly reduced their production target last year, eventually down from 20k to 6k-7k, so they could just squeeze above it (~7,100), they continue to only sell about 50% of quarterly production, which is really weird. But ..... they should also be safe, since the Saudi's are willing to back them, and whilst those injections are diluting shareholder value, it does almost look like they are safe ..... in a very weird sort of way?

My overall takeaway was 'middling', not good news, but not terrible news (for Tesla), but I think they've held up far too well to bring any relief to legacy.

What do legacy do now? They have to transition even faster, but with falling (most likely negative) profits on BEV's, they need the ICE sales to fund it. This isn't going to be pretty, but will be fascinating.

Musk clearly wants a 50% y-o-y increase in production & currently price reductions are the only way to achieve that. The launch of the Cybertruck will help add volume in 2024 after which we could see Model 2 deliveries starting. A $25,000 Model 2 must surely have the potential of selling at least 3 million units a year? In the meantime, there's a Model 3/Y facelift due later this year which will freshen up the range & give existing owners a reason to change.

This is slightly tongue-in-cheek, but the further price cuts in the US yesterday, are starting to look less like a price war, and more like a scorched earth policy.

Obviously BEV sales have been growing for a decade, but 2023 may be a year we look back on as when things got 'real'.4kWp (black/black) - Sofar Inverter - SSE(141°) - 30° pitch - North LincsInstalled June 2013 - PVGIS = 3400Sunsynk Ecco Inverter & Pylontech 5x US2000, 3x US3000, 3x US5000 Batteries - 37kWh0 -

Tesla’s pricing policy from the Q&A last night.

Ben Kallo

Thank you. Moving to sort of pricing, but a lot of pundits talk about the pie and losing share or gaining share. But how do you guys look at pricing versus the EVs or price vehicles, or does that not come into the equation? Sorry to ask about pricing again. Thank you.

Elon Musk

No, it's really just like – every day, we get a daily real-time update of how many cars were ordered yesterday, how many cars were produced yesterday. We must have – if there's a company that's got more real-time data than Tesla – I'm not sure, there's any company on earth that has better real-time data than Tesla, except maybe SpaceX Starlink. So – because like we don't have to -- for the other car companies, they will make the cars, send them to the dealers then the dealers will sell the cars. And then it takes quite a long time for them to get the data back to actually figure out how many cars were sold.

Whereas we know how many cars were ordered yesterday throughout the world. So our fingers on the pulse is real-time and does not have latency, whereas the other car companies have a lot of latency in their data. As does the government, the government has a lot of latency in their data. So we're just looking at and saying, okay, what does it take to achieve a clearing price for our vehicle production? And then we'll make a pricing change, and we see what happens immediately and adjust course. So we're adjusting course – and we're thinking about it literally every day, seven days a week. Every seven days, we collect that e-mail and so is the rest of the team. And we try to make the lease down decision that we can. And on balance, I think our decisions are pretty good. Sometimes they'll be down, but on average, they're, I think, better than the rest of the industry.

My comment:

Basically it is a reactive policy to sales. In the long term all manufacturers need to do that but in the short term some have a buffer in the dealer network or choose to adjust output/supply to the market. Tesla is production lead and hence uses price to maximise stock turnover (rather than profit) although there were rumours that Shanghai production was cut for a few days (under the guise of refitting lines) at the end of 2022 because of lack of demand. The problem with responding day by day, as Tesla did at the end of Q1, is that people become aware that that’s how Tesla is operating and defer their orders until the price goes down. Not everyone has that option so Tesla will still make sales at the higher price to those who are replacing existing vehicles (e.g. company cars) but discretionary purchasers can play Tesla at their own game. Just like you get your best deals from your local car dealer ant the end of the month when there are targets to be hit, you wait until end of quarter with Tesla.

I think Tesla have being doing the same thing with their CPO used cars recently, slashing the price when they need to clear stock then hiking it back up. Because they control so much of the used stock and can offer a full extended warranty they can do that.

Northern Lincolnshire. 7.8 kWp system, (4.2 kWwest facing panels , 3.6 kWeast facing), Solis inverters installed 2018, 5kW SSE facing system (shaded in afternoon) added in 2025 with Tesla PW3 battery, Mitsubishi SRK35ZS-S and SRK20ZS-S Wall Mounted A2A Heat Pumps, ex Nissan Leaf owner.0 -

The cheapest Focus costs £27,080. The Focus that matches a likely Model 2 spec is around £30,000. Even the Fiesta starts around £20,000 with higher spec models costing £24,000.Grumpy_chap said:

Well, £25k for a Focus sounds expensive to me.michaels said:25k model 2 still sounds expensive to me, is it Focus size or Fiesta size?

But, in today's prices, that would compete directly with MG4 and Octavia.

I guess it all depends what happens to the overall market price (and availability) for new cars of all types and the extent to which the uplifts for chip shortage etc fall back or are maintained.4kWp (black/black) - Sofar Inverter - SSE(141°) - 30° pitch - North LincsInstalled June 2013 - PVGIS = 3400Sunsynk Ecco Inverter & Pylontech 5x US2000, 3x US3000, 3x US5000 Batteries - 37kWh0 -

Looking at 'real life' pricing on https://www.cars2buy.co.uk/new-cars/ford/focus-hatchback/ it seems that this size of vehicles start at about 19k for a Fiat tipo, 22k for a Focus and 23.5k for a Golf.1961Nick said:

The cheapest Focus costs £27,080. The Focus that matches a likely Model 2 spec is around £30,000. Even the Fiesta starts around £20,000 with higher spec models costing £24,000.Grumpy_chap said:

Well, £25k for a Focus sounds expensive to me.michaels said:25k model 2 still sounds expensive to me, is it Focus size or Fiesta size?

But, in today's prices, that would compete directly with MG4 and Octavia.

I guess it all depends what happens to the overall market price (and availability) for new cars of all types and the extent to which the uplifts for chip shortage etc fall back or are maintained.

However the possible model 2 spy shots perhaps suggest that it will be slightly more SUV/higher than these and so perhaps should be compared against a Toyota CHR, VW T-Roc or Peugeot 3008 cars?I think....0 -

I'd replace my (Salary Sacrifice) Leaf with a Tesla 2, if they were similar pricing.michaels said:

Looking at 'real life' pricing on https://www.cars2buy.co.uk/new-cars/ford/focus-hatchback/ it seems that this size of vehicles start at about 19k for a Fiat tipo, 22k for a Focus and 23.5k for a Golf.1961Nick said:

The cheapest Focus costs £27,080. The Focus that matches a likely Model 2 spec is around £30,000. Even the Fiesta starts around £20,000 with higher spec models costing £24,000.Grumpy_chap said:

Well, £25k for a Focus sounds expensive to me.michaels said:25k model 2 still sounds expensive to me, is it Focus size or Fiesta size?

But, in today's prices, that would compete directly with MG4 and Octavia.

I guess it all depends what happens to the overall market price (and availability) for new cars of all types and the extent to which the uplifts for chip shortage etc fall back or are maintained.

However the possible model 2 spy shots perhaps suggest that it will be slightly more SUV/higher than these and so perhaps should be compared against a Toyota CHR, VW T-Roc or Peugeot 3008 cars?I'm a Forum Ambassador on the housing, mortgages & student money saving boards. I volunteer to help get your forum questions answered and keep the forum running smoothly. Forum Ambassadors are not moderators and don't read every post. If you spot an illegal or inappropriate post then please report it to forumteam@moneysavingexpert.com (it's not part of my role to deal with this). Any views are mine and not the official line of MoneySavingExpert.com.2 -

Only because Focus and Fiesta are in surge pricing as are most cars. Will price normality be restored?1961Nick said:

The cheapest Focus costs £27,080. The Focus that matches a likely Model 2 spec is around £30,000. Even the Fiesta starts around £20,000 with higher spec models costing £24,000.Grumpy_chap said:

Well, £25k for a Focus sounds expensive to me.michaels said:25k model 2 still sounds expensive to me, is it Focus size or Fiesta size?

But, in today's prices, that would compete directly with MG4 and Octavia.

I guess it all depends what happens to the overall market price (and availability) for new cars of all types and the extent to which the uplifts for chip shortage etc fall back or are maintained.0 -

Yes, but only for the cheapest RWD base model, as it uses the LFP batts. But that said, the LR dual motor version isn't currently available in the US, but it still qualifies (or will qualify) for the full $7.5k.1961Nick said:

Hasn't the tax rebate for the Model 3 just halved to $3750 because the battery is manufactured in China? That could be the reason for the recent price reduction.Martyn1981 said:

Yep, all looks very promising.1961Nick said:

I think that considering the hefty discounting, a gross margin of 19.3% is quite an achievement. The Model 3 is now competing with the likes of the ID3 as well as the ID4 & is still generating a healthy profit. At the end of March, the Model 3 SR was actually £2000 cheaper than the poverty spec ID3 in the UK.Martyn1981 said:

Yes, very true, and the comparison to Toyota doesn't work when net profits are considered, since 10-11% for Tesla is helping to move them towards the top of the list for annual profits, despite far lower sales numbers than the biggest auto groups.1961Nick said:

The problem with trying to compare Tesla with another automaker is that you're either comparing them with an ICEV manufacturer like Toyota or trying to extract the BEV figures from a mix of ICEV & BEV numbers. The only true comparison at the moment is with Ford, but even then there's no detail from the electric division yet other than that they expect to lose $3B this year on top of the $3 they lost in the last 2 years. Tesla have made further price reductions since Ford estimated the loss for this year which won't help the situation.JKenH said:Tesla (TSLA) releases Q1 2023 results: meets expectations, impresses with gross margin

Edit:Edit 2. Average selling price has dropped from around $54k per car in Q1 2022 to $47k in 2023

Edit 3: just out of interest here is a comparison of Tesla and Toyota Gross Margins over the last 3 years.Edit 4: The ASPs quoted in edit 2 were my calculations. Here are alternative figures and comment on the gross margin.The average Tesla vehicle selling price in the first quarter was around $46,850, according to FactSet estimates. That's down from $51,400 in the fourth quarter and $52,100 a year ago.

Auto gross margins excluding regulatory credits and leases declined to 18.3% vs. 23.8% in Q4. That is below the 20% gross margin "floor" Tesla had previously forecast.

Of the Chinese manufacturers, BYD have an impressive market share in China, but when they expand globally they're likely to run straight into reliability, safety & regulatory issues. A battery fire every day might be something that can be supressed in China, but anywhere else it'll be front page news.

Rivian, Lucid & NIO look like money pits with no end in sight. Surely it can't be long before the big legacy auto players start picking them off to fast track their EV ranges & avoid ICEV fines in the process.

Would like to feel slightly smug about the gross margin figure, but actually I think we split the difference between us, when the regulatory credits are removed. [Plus my ~20% guess, was tbh, leaning towards 20+ not 20-.] Zach did explain that missing the 20%+ target was down to the further price cuts in Q1, after his statements on the Q4 earnings call.

Given Tesla's (and BYD's) decision to go for market share, at the cost of gross margin, I suspect legacy auto need to be scared, especially if the 'recession' takes another 12 months to end.

Regarding Rivian and Lucid, totally agree about them being money pits, but in Rivian's defence, they are meeting production targets and growing towards profitability. Combine that with their Amazon sales, and they have a decent chance.

Lucid however, continue to be somewhat of a joke. Having repeatedly reduced their production target last year, eventually down from 20k to 6k-7k, so they could just squeeze above it (~7,100), they continue to only sell about 50% of quarterly production, which is really weird. But ..... they should also be safe, since the Saudi's are willing to back them, and whilst those injections are diluting shareholder value, it does almost look like they are safe ..... in a very weird sort of way?

My overall takeaway was 'middling', not good news, but not terrible news (for Tesla), but I think they've held up far too well to bring any relief to legacy.

What do legacy do now? They have to transition even faster, but with falling (most likely negative) profits on BEV's, they need the ICE sales to fund it. This isn't going to be pretty, but will be fascinating.

Musk clearly wants a 50% y-o-y increase in production & currently price reductions are the only way to achieve that. The launch of the Cybertruck will help add volume in 2024 after which we could see Model 2 deliveries starting. A $25,000 Model 2 must surely have the potential of selling at least 3 million units a year? In the meantime, there's a Model 3/Y facelift due later this year which will freshen up the range & give existing owners a reason to change.

This is slightly tongue-in-cheek, but the further price cuts in the US yesterday, are starting to look less like a price war, and more like a scorched earth policy.

Obviously BEV sales have been growing for a decade, but 2023 may be a year we look back on as when things got 'real'.Mart. Cardiff. 8.72 kWp PV systems (2.12 SSW 4.6 ESE & 2.0 WNW). 28kWh battery storage. Two A2A units for cleaner heating. Two BEV's for cleaner driving.

For general PV advice please see the PV FAQ thread on the Green & Ethical Board.0 -

Tesla abandons Mercedes battle to take on the likes of Ford

“Tesla is not only sacrificing its EV margins to achieve its volume ambitions. To some extent, it is also placing the goodwill and brand equity that it has built up on the altar too,” Daniel Roeska, Bernstein’s European auto analyst, wrote in a report Thursday. “This is most important in the premium end of the market, where brand perception and social status are the crux of sales.”Northern Lincolnshire. 7.8 kWp system, (4.2 kWwest facing panels , 3.6 kWeast facing), Solis inverters installed 2018, 5kW SSE facing system (shaded in afternoon) added in 2025 with Tesla PW3 battery, Mitsubishi SRK35ZS-S and SRK20ZS-S Wall Mounted A2A Heat Pumps, ex Nissan Leaf owner.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards