We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

EV Discussion thread

Comments

-

21% would mean a lot of glum boardrooms across the auto industry.JKenH said:Posted for the quote, not the headline.Teslas are cheaper than ever and it's a creating a headache for the entire auto industry

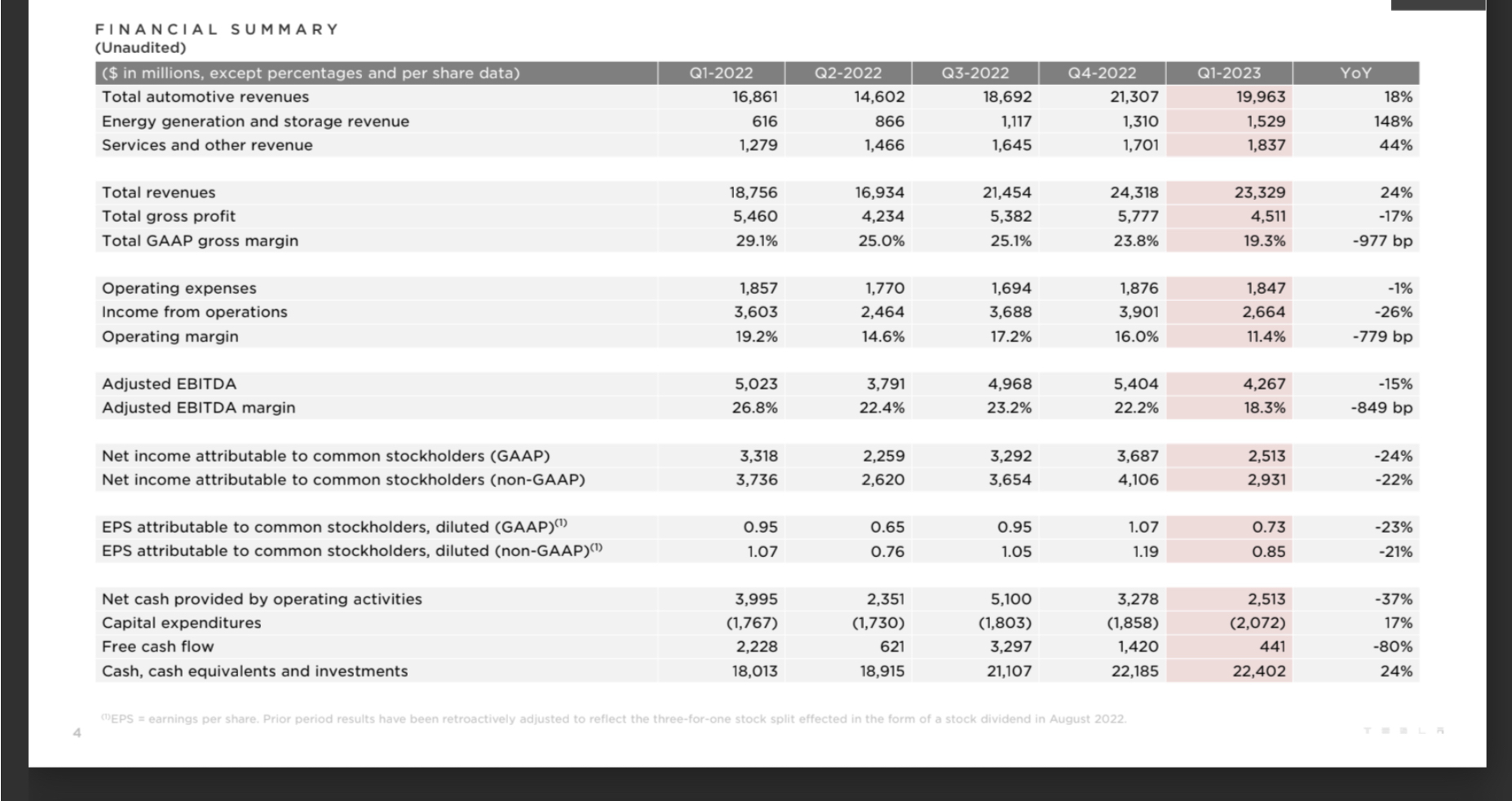

Analysts polled by Bloomberg expect gross margins to fall slightly, to about 21% from nearly 24%, along with lower per-share earnings and revenue.

Toady's share price movements following the latest price reductions give an indication of who's hurting the most & it's not Tesla.

Tesla -1.03%

Ford -3.18%

Lucid -4.15%

NIO -6.5%

Rivian -4.73%

Fisker -1.98%4kWp (black/black) - Sofar Inverter - SSE(141°) - 30° pitch - North LincsInstalled June 2013 - PVGIS = 3400Sunsynk Ecco Inverter & Pylontech 5x US2000, 3x US3000, 3x US5000 Batteries - 37kWh0 -

Quite rightly so as it would indicate those legacy auto manufacturers have been asleep at the wheel in terms of innovation - the Tesla profits are not only because they are getting the "E" part right but because they are getting the core manufacturing process for the the "V" part right also.1961Nick said:21% would mean a lot of glum boardrooms across the auto industry.0 -

I don't think I know how to use the Tesla website.

When I look right now, there are only 3 (three) used TM3 LR (not Performance) cars listed.

That can't be correct...0 -

I saw five listed all between 23k and 27k miles but all over £32k which IIRC is around £5k more than a month ago. Some of them were listed several weeks ago and then removed from the listings to reappear later. There will be more kicking around and being advertised when Tesla need the room.Northern Lincolnshire. 7.8 kWp system, (4.2 kWwest facing panels , 3.6 kWeast facing), Solis inverters installed 2018, 5kW SSE facing system (shaded in afternoon) added in 2025 with Tesla PW3 battery, Mitsubishi SRK35ZS-S and SRK20ZS-S Wall Mounted A2A Heat Pumps, ex Nissan Leaf owner.1

-

Tesla (TSLA) releases Q1 2023 results: meets expectations, impresses with gross margin

Edit: Edit 2. Average selling price has dropped from around $54k per car in Q1 2022 to $47k in 2023

Edit 2. Average selling price has dropped from around $54k per car in Q1 2022 to $47k in 2023

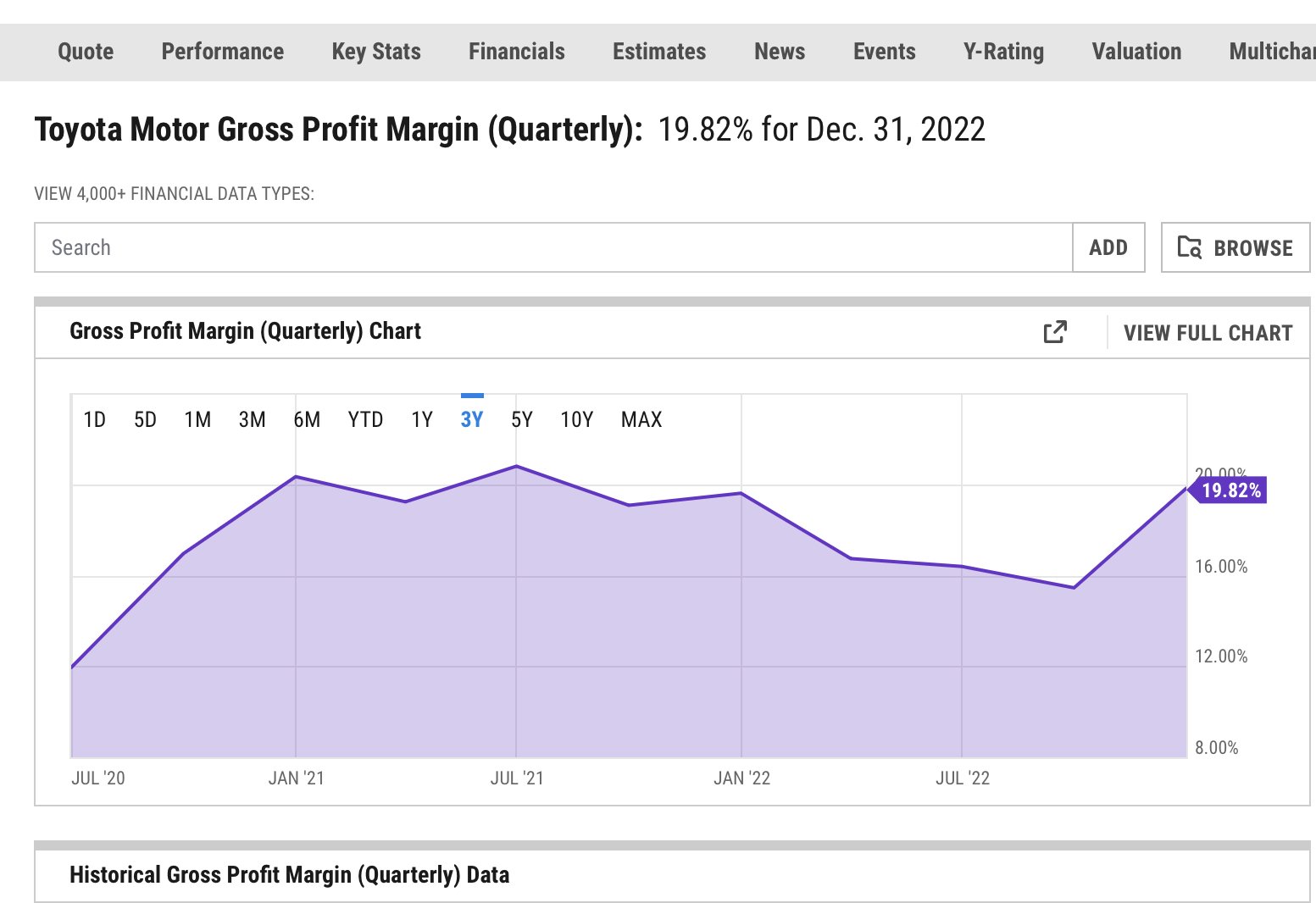

Edit 3: just out of interest here is a comparison of Tesla and Toyota Gross Margins over the last 3 years.

Edit 4: The ASPs quoted in edit 2 were my calculations. Here are alternative figures and comment on the gross margin.

Edit 4: The ASPs quoted in edit 2 were my calculations. Here are alternative figures and comment on the gross margin.The average Tesla vehicle selling price in the first quarter was around $46,850, according to FactSet estimates. That's down from $51,400 in the fourth quarter and $52,100 a year ago.

Auto gross margins excluding regulatory credits and leases declined to 18.3% vs. 23.8% in Q4. That is below the 20% gross margin "floor" Tesla had previously forecast.

Northern Lincolnshire. 7.8 kWp system, (4.2 kWwest facing panels , 3.6 kWeast facing), Solis inverters installed 2018, 5kW SSE facing system (shaded in afternoon) added in 2025 with Tesla PW3 battery, Mitsubishi SRK35ZS-S and SRK20ZS-S Wall Mounted A2A Heat Pumps, ex Nissan Leaf owner.1 -

The problem with trying to compare Tesla with another automaker is that you're either comparing them with an ICEV manufacturer like Toyota or trying to extract the BEV figures from a mix of ICEV & BEV numbers. The only true comparison at the moment is with Ford, but even then there's no detail from the electric division yet other than that they expect to lose $3B this year on top of the $3 they lost in the last 2 years. Tesla have made further price reductions since Ford estimated the loss for this year which won't help the situation.JKenH said:Tesla (TSLA) releases Q1 2023 results: meets expectations, impresses with gross margin

Edit:Edit 2. Average selling price has dropped from around $54k per car in Q1 2022 to $47k in 2023

Edit 3: just out of interest here is a comparison of Tesla and Toyota Gross Margins over the last 3 years.Edit 4: The ASPs quoted in edit 2 were my calculations. Here are alternative figures and comment on the gross margin.The average Tesla vehicle selling price in the first quarter was around $46,850, according to FactSet estimates. That's down from $51,400 in the fourth quarter and $52,100 a year ago.

Auto gross margins excluding regulatory credits and leases declined to 18.3% vs. 23.8% in Q4. That is below the 20% gross margin "floor" Tesla had previously forecast.

Of the Chinese manufacturers, BYD have an impressive market share in China, but when they expand globally they're likely to run straight into reliability, safety & regulatory issues. A battery fire every day might be something that can be supressed in China, but anywhere else it'll be front page news.

Rivian, Lucid & NIO look like money pits with no end in sight. Surely it can't be long before the big legacy auto players start picking them off to fast track their EV ranges & avoid ICEV fines in the process.

4kWp (black/black) - Sofar Inverter - SSE(141°) - 30° pitch - North LincsInstalled June 2013 - PVGIS = 3400Sunsynk Ecco Inverter & Pylontech 5x US2000, 3x US3000, 3x US5000 Batteries - 37kWh1 -

Yes, Ford are losing the sort of money on EVs that Tesla were in 2018. There are bound to be some development costs and Ford has admitted what they are.1961Nick said:

The problem with trying to compare Tesla with another automaker is that you're either comparing them with an ICEV manufacturer like Toyota or trying to extract the BEV figures from a mix of ICEV & BEV numbers. The only true comparison at the moment is with Ford, but even then there's no detail from the electric division yet other than that they expect to lose $3B this year on top of the $3 they lost in the last 2 years. Tesla have made further price reductions since Ford estimated the loss for this year which won't help the situation.JKenH said:Tesla (TSLA) releases Q1 2023 results: meets expectations, impresses with gross margin

Edit:Edit 2. Average selling price has dropped from around $54k per car in Q1 2022 to $47k in 2023

Edit 3: just out of interest here is a comparison of Tesla and Toyota Gross Margins over the last 3 years.Edit 4: The ASPs quoted in edit 2 were my calculations. Here are alternative figures and comment on the gross margin.The average Tesla vehicle selling price in the first quarter was around $46,850, according to FactSet estimates. That's down from $51,400 in the fourth quarter and $52,100 a year ago.

Auto gross margins excluding regulatory credits and leases declined to 18.3% vs. 23.8% in Q4. That is below the 20% gross margin "floor" Tesla had previously forecast.

Of the Chinese manufacturers, BYD have an impressive market share in China, but when they expand globally they're likely to run straight into reliability, safety & regulatory issues. A battery fire every day might be something that can be supressed in China, but anywhere else it'll be front page news.

Rivian, Lucid & NIO look like money pits with no end in sight. Surely it can't be long before the big legacy auto players start picking them off to fast track their EV ranges & avoid ICEV fines in the process.Elon Musk aside, I don’t actually think there is too much to worry about with Tesla - they are still making good profit but with each passing year the automotive* division becomes more like other automakers and has to face the challenges they face. Until last year and BYD Tesla had no real competition in the volume EV market - the likes of VW were still ramping up production while others are still developing their product, all while dealing with interruptions to production from COVID supplier issues. Tesla were able to put up their prices which also gave other manufacturers the headroom to do the same. VW and Korean EV manufacturers now have healthy waiting lists despite hiked prices. MG have a fantastic product and demand to go with it.As I see it Tesla are trying to expand too rapidly committing to levels of production that may not be sustainable in the current market and certainly not at current prices and with their current limited model range. (One has to ask why the Model S and X are selling so poorly). It is possible to expand too fast - if you can’t sell what you are making you have to cut prices and margins and if you look at the operating margin Tesla has taken a big hit. This is where Tesla may lose out to other traditional automakers who manage demand through the dealer network and fleets/leasing companies and do not have to tinker with their list prices - individual models may see price tweaks but whole brands rarely. Tesla by slashing prices across its full range is potentially damaging its image as an aspirational brand in the general auto marketplace. Go downmarket with pricing and the brand image goes downmarket. That’s fine if Tesla wants to be a volume seller which clearly is its primary objective but that has a long term effect on margins and as an investor that would concern me.The big question is what is now sustaining the high valuation on Tesla shares? It isn’t exceptionally high margins. It isn’t a product that flies off the shelf at any price. The image of its FSD advantage has been undermined by other manufacturers releasing driver assistance systems that do allow the driver to take their hands off the wheel and rolling out (geofenced) robotaxis. In recent years some of Tesla’s tech has even gone backwards (ditching of radar and USS on the altar of cost saving). This last year has seen increasing insurance premiums for Tesla cars and the secondhand market for Teslas and residual values trashed by Tesla’s price slashing.Elon Musk is not interested in profit only achieving arbitrary production and delivery volumes at whatever cost. While that idea will appeal to many it isn’t a recipe for a buoyant valuation. Great visionary that he is, I think his time at Tesla has passed and for the good of the company he should move on.

*the energy storage division is going from strength to strength and with falling lithium prices should do very well this year.Northern Lincolnshire. 7.8 kWp system, (4.2 kWwest facing panels , 3.6 kWeast facing), Solis inverters installed 2018, 5kW SSE facing system (shaded in afternoon) added in 2025 with Tesla PW3 battery, Mitsubishi SRK35ZS-S and SRK20ZS-S Wall Mounted A2A Heat Pumps, ex Nissan Leaf owner.0 -

Yes, very true, and the comparison to Toyota doesn't work when net profits are considered, since 10-11% for Tesla is helping to move them towards the top of the list for annual profits, despite far lower sales numbers than the biggest auto groups.1961Nick said:

The problem with trying to compare Tesla with another automaker is that you're either comparing them with an ICEV manufacturer like Toyota or trying to extract the BEV figures from a mix of ICEV & BEV numbers. The only true comparison at the moment is with Ford, but even then there's no detail from the electric division yet other than that they expect to lose $3B this year on top of the $3 they lost in the last 2 years. Tesla have made further price reductions since Ford estimated the loss for this year which won't help the situation.JKenH said:Tesla (TSLA) releases Q1 2023 results: meets expectations, impresses with gross margin

Edit:Edit 2. Average selling price has dropped from around $54k per car in Q1 2022 to $47k in 2023

Edit 3: just out of interest here is a comparison of Tesla and Toyota Gross Margins over the last 3 years.Edit 4: The ASPs quoted in edit 2 were my calculations. Here are alternative figures and comment on the gross margin.The average Tesla vehicle selling price in the first quarter was around $46,850, according to FactSet estimates. That's down from $51,400 in the fourth quarter and $52,100 a year ago.

Auto gross margins excluding regulatory credits and leases declined to 18.3% vs. 23.8% in Q4. That is below the 20% gross margin "floor" Tesla had previously forecast.

Of the Chinese manufacturers, BYD have an impressive market share in China, but when they expand globally they're likely to run straight into reliability, safety & regulatory issues. A battery fire every day might be something that can be supressed in China, but anywhere else it'll be front page news.

Rivian, Lucid & NIO look like money pits with no end in sight. Surely it can't be long before the big legacy auto players start picking them off to fast track their EV ranges & avoid ICEV fines in the process.

Would like to feel slightly smug about the gross margin figure, but actually I think we split the difference between us, when the regulatory credits are removed. [Plus my ~20% guess, was tbh, leaning towards 20+ not 20-.] Zach did explain that missing the 20%+ target was down to the further price cuts in Q1, after his statements on the Q4 earnings call.

Given Tesla's (and BYD's) decision to go for market share, at the cost of gross margin, I suspect legacy auto need to be scared, especially if the 'recession' takes another 12 months to end.

Regarding Rivian and Lucid, totally agree about them being money pits, but in Rivian's defence, they are meeting production targets and growing towards profitability. Combine that with their Amazon sales, and they have a decent chance.

Lucid however, continue to be somewhat of a joke. Having repeatedly reduced their production target last year, eventually down from 20k to 6k-7k, so they could just squeeze above it (~7,100), they continue to only sell about 50% of quarterly production, which is really weird. But ..... they should also be safe, since the Saudi's are willing to back them, and whilst those injections are diluting shareholder value, it does almost look like they are safe ..... in a very weird sort of way?

My overall takeaway was 'middling', not good news, but not terrible news (for Tesla), but I think they've held up far too well to bring any relief to legacy.

What do legacy do now? They have to transition even faster, but with falling (most likely negative) profits on BEV's, they need the ICE sales to fund it. This isn't going to be pretty, but will be fascinating.Mart. Cardiff. 8.72 kWp PV systems (2.12 SSW 4.6 ESE & 2.0 WNW). 28kWh battery storage. Two A2A units for cleaner heating. Two BEV's for cleaner driving.

For general PV advice please see the PV FAQ thread on the Green & Ethical Board.1 -

I think that considering the hefty discounting, a gross margin of 19.3% is quite an achievement. The Model 3 is now competing with the likes of the ID3 as well as the ID4 & is still generating a healthy profit. At the end of March, the Model 3 SR was actually £2000 cheaper than the poverty spec ID3 in the UK.Martyn1981 said:

Yes, very true, and the comparison to Toyota doesn't work when net profits are considered, since 10-11% for Tesla is helping to move them towards the top of the list for annual profits, despite far lower sales numbers than the biggest auto groups.1961Nick said:

The problem with trying to compare Tesla with another automaker is that you're either comparing them with an ICEV manufacturer like Toyota or trying to extract the BEV figures from a mix of ICEV & BEV numbers. The only true comparison at the moment is with Ford, but even then there's no detail from the electric division yet other than that they expect to lose $3B this year on top of the $3 they lost in the last 2 years. Tesla have made further price reductions since Ford estimated the loss for this year which won't help the situation.JKenH said:Tesla (TSLA) releases Q1 2023 results: meets expectations, impresses with gross margin

Edit:Edit 2. Average selling price has dropped from around $54k per car in Q1 2022 to $47k in 2023

Edit 3: just out of interest here is a comparison of Tesla and Toyota Gross Margins over the last 3 years.Edit 4: The ASPs quoted in edit 2 were my calculations. Here are alternative figures and comment on the gross margin.The average Tesla vehicle selling price in the first quarter was around $46,850, according to FactSet estimates. That's down from $51,400 in the fourth quarter and $52,100 a year ago.

Auto gross margins excluding regulatory credits and leases declined to 18.3% vs. 23.8% in Q4. That is below the 20% gross margin "floor" Tesla had previously forecast.

Of the Chinese manufacturers, BYD have an impressive market share in China, but when they expand globally they're likely to run straight into reliability, safety & regulatory issues. A battery fire every day might be something that can be supressed in China, but anywhere else it'll be front page news.

Rivian, Lucid & NIO look like money pits with no end in sight. Surely it can't be long before the big legacy auto players start picking them off to fast track their EV ranges & avoid ICEV fines in the process.

Would like to feel slightly smug about the gross margin figure, but actually I think we split the difference between us, when the regulatory credits are removed. [Plus my ~20% guess, was tbh, leaning towards 20+ not 20-.] Zach did explain that missing the 20%+ target was down to the further price cuts in Q1, after his statements on the Q4 earnings call.

Given Tesla's (and BYD's) decision to go for market share, at the cost of gross margin, I suspect legacy auto need to be scared, especially if the 'recession' takes another 12 months to end.

Regarding Rivian and Lucid, totally agree about them being money pits, but in Rivian's defence, they are meeting production targets and growing towards profitability. Combine that with their Amazon sales, and they have a decent chance.

Lucid however, continue to be somewhat of a joke. Having repeatedly reduced their production target last year, eventually down from 20k to 6k-7k, so they could just squeeze above it (~7,100), they continue to only sell about 50% of quarterly production, which is really weird. But ..... they should also be safe, since the Saudi's are willing to back them, and whilst those injections are diluting shareholder value, it does almost look like they are safe ..... in a very weird sort of way?

My overall takeaway was 'middling', not good news, but not terrible news (for Tesla), but I think they've held up far too well to bring any relief to legacy.

What do legacy do now? They have to transition even faster, but with falling (most likely negative) profits on BEV's, they need the ICE sales to fund it. This isn't going to be pretty, but will be fascinating.

Musk clearly wants a 50% y-o-y increase in production & currently price reductions are the only way to achieve that. The launch of the Cybertruck will help add volume in 2024 after which we could see Model 2 deliveries starting. A $25,000 Model 2 must surely have the potential of selling at least 3 million units a year? In the meantime, there's a Model 3/Y facelift due later this year which will freshen up the range & give existing owners a reason to change.4kWp (black/black) - Sofar Inverter - SSE(141°) - 30° pitch - North LincsInstalled June 2013 - PVGIS = 3400Sunsynk Ecco Inverter & Pylontech 5x US2000, 3x US3000, 3x US5000 Batteries - 37kWh1 -

25k model 2 still sounds expensive to me, is it Focus size or Fiesta size? Also it will likely cannibalise M3/Y sales as every new model has done.1961Nick said:

I think that considering the hefty discounting, a gross margin of 19.3% is quite an achievement. The Model 3 is now competing with the likes of the ID3 as well as the ID4 & is still generating a healthy profit. At the end of March, the Model 3 SR was actually £2000 cheaper than the poverty spec ID3 in the UK.Martyn1981 said:

Yes, very true, and the comparison to Toyota doesn't work when net profits are considered, since 10-11% for Tesla is helping to move them towards the top of the list for annual profits, despite far lower sales numbers than the biggest auto groups.1961Nick said:

The problem with trying to compare Tesla with another automaker is that you're either comparing them with an ICEV manufacturer like Toyota or trying to extract the BEV figures from a mix of ICEV & BEV numbers. The only true comparison at the moment is with Ford, but even then there's no detail from the electric division yet other than that they expect to lose $3B this year on top of the $3 they lost in the last 2 years. Tesla have made further price reductions since Ford estimated the loss for this year which won't help the situation.JKenH said:Tesla (TSLA) releases Q1 2023 results: meets expectations, impresses with gross margin

Edit:Edit 2. Average selling price has dropped from around $54k per car in Q1 2022 to $47k in 2023

Edit 3: just out of interest here is a comparison of Tesla and Toyota Gross Margins over the last 3 years.Edit 4: The ASPs quoted in edit 2 were my calculations. Here are alternative figures and comment on the gross margin.The average Tesla vehicle selling price in the first quarter was around $46,850, according to FactSet estimates. That's down from $51,400 in the fourth quarter and $52,100 a year ago.

Auto gross margins excluding regulatory credits and leases declined to 18.3% vs. 23.8% in Q4. That is below the 20% gross margin "floor" Tesla had previously forecast.

Of the Chinese manufacturers, BYD have an impressive market share in China, but when they expand globally they're likely to run straight into reliability, safety & regulatory issues. A battery fire every day might be something that can be supressed in China, but anywhere else it'll be front page news.

Rivian, Lucid & NIO look like money pits with no end in sight. Surely it can't be long before the big legacy auto players start picking them off to fast track their EV ranges & avoid ICEV fines in the process.

Would like to feel slightly smug about the gross margin figure, but actually I think we split the difference between us, when the regulatory credits are removed. [Plus my ~20% guess, was tbh, leaning towards 20+ not 20-.] Zach did explain that missing the 20%+ target was down to the further price cuts in Q1, after his statements on the Q4 earnings call.

Given Tesla's (and BYD's) decision to go for market share, at the cost of gross margin, I suspect legacy auto need to be scared, especially if the 'recession' takes another 12 months to end.

Regarding Rivian and Lucid, totally agree about them being money pits, but in Rivian's defence, they are meeting production targets and growing towards profitability. Combine that with their Amazon sales, and they have a decent chance.

Lucid however, continue to be somewhat of a joke. Having repeatedly reduced their production target last year, eventually down from 20k to 6k-7k, so they could just squeeze above it (~7,100), they continue to only sell about 50% of quarterly production, which is really weird. But ..... they should also be safe, since the Saudi's are willing to back them, and whilst those injections are diluting shareholder value, it does almost look like they are safe ..... in a very weird sort of way?

My overall takeaway was 'middling', not good news, but not terrible news (for Tesla), but I think they've held up far too well to bring any relief to legacy.

What do legacy do now? They have to transition even faster, but with falling (most likely negative) profits on BEV's, they need the ICE sales to fund it. This isn't going to be pretty, but will be fascinating.

Musk clearly wants a 50% y-o-y increase in production & currently price reductions are the only way to achieve that. The launch of the Cybertruck will help add volume in 2024 after which we could see Model 2 deliveries starting. A $25,000 Model 2 must surely have the potential of selling at least 3 million units a year? In the meantime, there's a Model 3/Y facelift due later this year which will freshen up the range & give existing owners a reason to change.

What is more interesting is our Tesla achieving the lower production costs we have been told will come from innovative design (as well as obviously huge volume of individual models). For example I wonder how model Y production costs compare to the Mach E, ID 4 and EV6?I think....0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards