We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Octopus Tracker

Comments

-

A relatively small number of tracker customers v1 and v2 are still on fixed terms with vastly lower standing charges and product capsSAC2334 said:

Every one now is on exactly the same rate (with usual regional differences ) as any other version right back to the original V1 .We are all getting the same as Nov 22 v1 except new custs who are on Dec 23..Spoonie_Turtle said:

There have been different caps with different versions, so for instance summer of 2022 people joining later were paying more than others on the older versions with the lower caps. There have also been differences in the standing charges, between the earliest original versions.SAC2334 said:

Seems unfair on those on the Dec 23 new rate that Nov 22 rates are lower and sometimes 12 % lower for electricity . Has Tracker ever had two tier pricing before ? I have only been on it since early January and would have been a bit narked if others were getting lower rates , and I don t mean regional rates .masonic said:

No, they will reach a decision in January about the timing to move everyone across. It may not be for some time after that, hopefully after winter is behind us! Reasonable notice should help with this.Telegraph_Sam said:I was trying to work out from the Tracker FAQ's when the new charges come into effect if I am on Nov 22 v1 without an end date. Has this date been publicized?

It might make a bit more sense if you view them as different tariffs, just all of a certain type. Kind of like how fixes are offered, then closed to new customers. Obviously not quite the same as that's based on buying set amounts of energy, but it means people are on tariffs with a similar name but different versions and pricing all at the same time, and if you're too late for a cheaper one that's not inherently unfair. Similarly if you've joined a Tracker tariff too late to benefit from the cheaper, earlier version, that's just the way it is.1 -

I have read this para 3.16 through several times. My interpretation for what it's worth is that if I made an active choice to move to Tracker [Nov 22 v1] then I am not protected by the price cap regardless of whether there is an end date or not. It refers to SC's only by the look of it. There may be another para that clarifies how the date of joining the tariff affects the situation.Telegraph Sam

There are also unknown unknowns - the one's we don't know we don't know1 -

bristolleedsfan said:

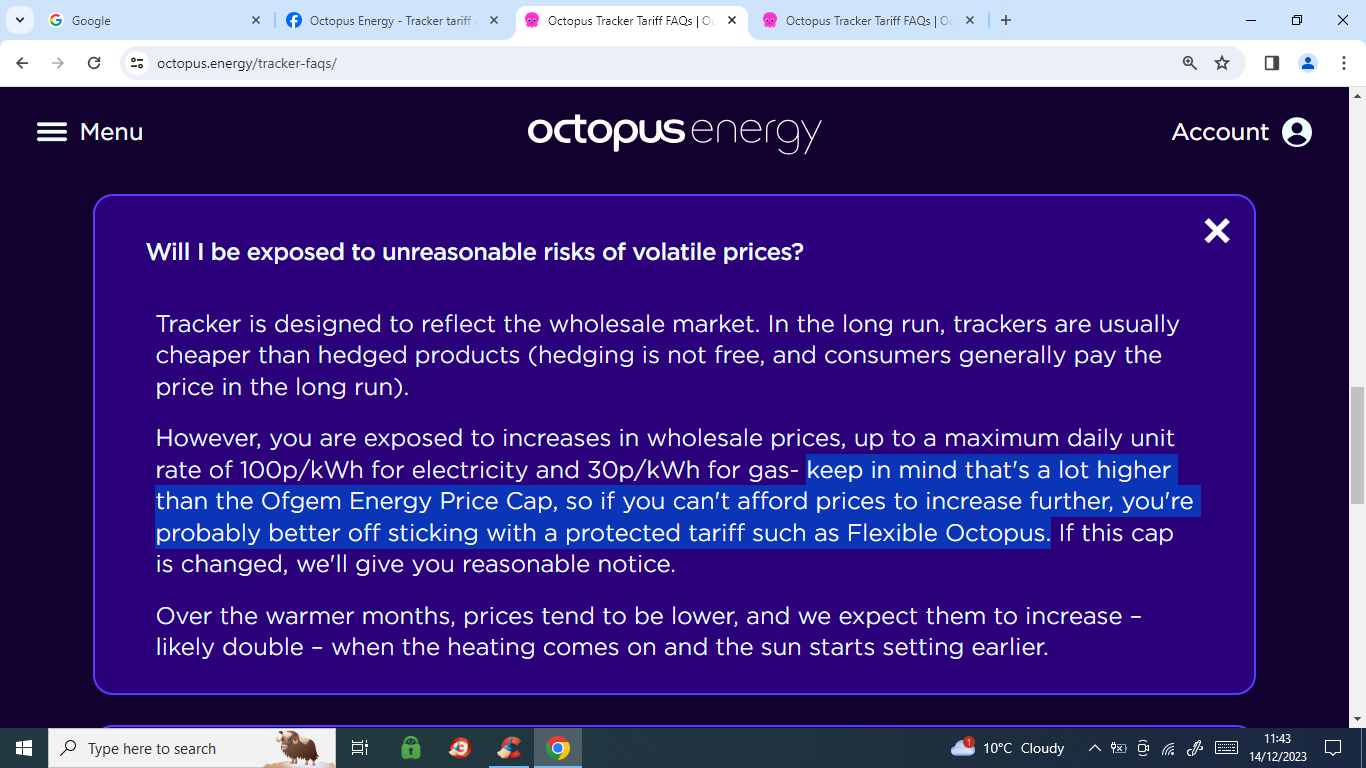

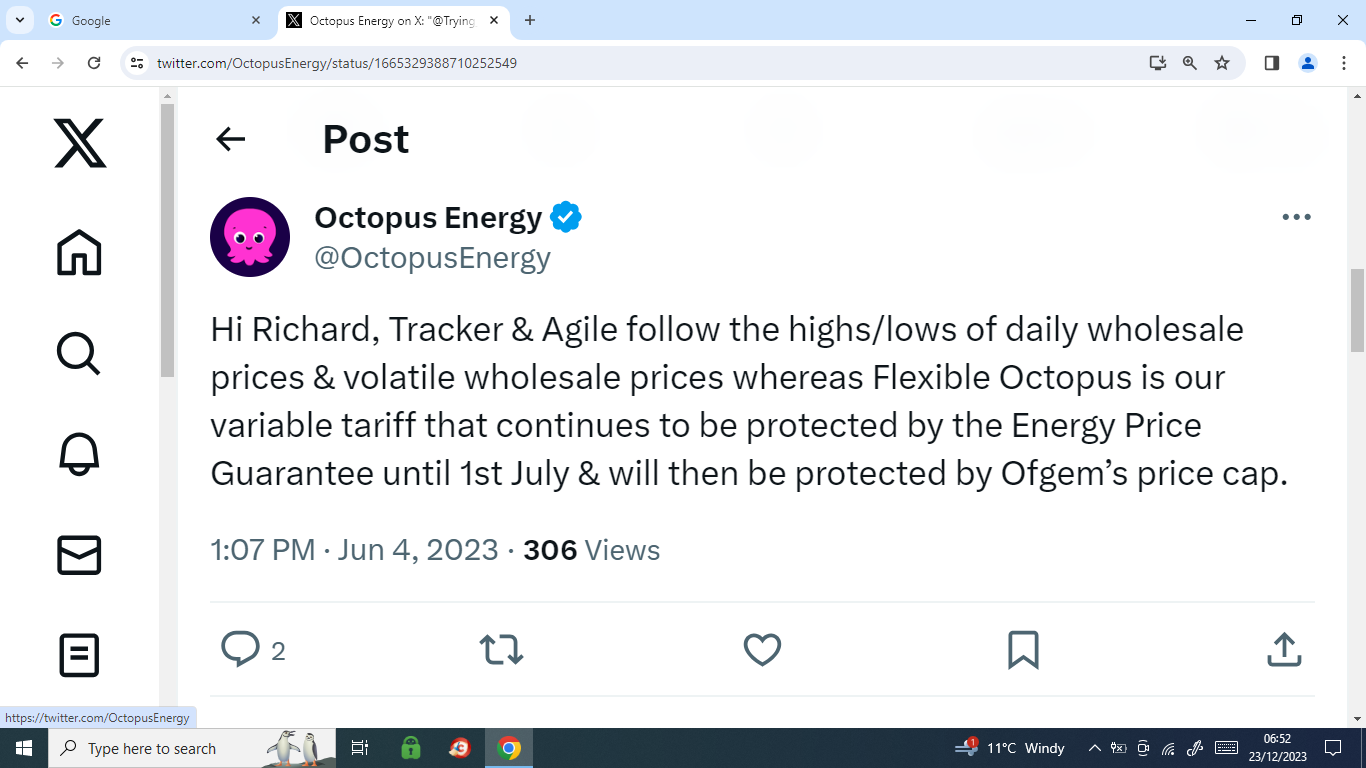

Agile and Tracker tariffs would not be subject to price cap as a variable tariff with no end date. (I know they say this and that). Agile/Tracker tariffs seemingly qualified for EPG discount for new signups after 1 October 2022 as a variable tariff with no end date not subject to price cap.Bendo said:. The only reason it has an end date is to work around the price cap. I've no desire to read the various conditions but Octopus reasoning is it needs an end term to avoid being subject to price cap. To qualify for EPG, they had to remove the end term.Whether their interpretation is correct, no idea.1

I've no desire to read the various conditions but Octopus reasoning is it needs an end term to avoid being subject to price cap. To qualify for EPG, they had to remove the end term.Whether their interpretation is correct, no idea.1 -

Whatever the reason Octopus give for reviewing / rationalising / increasing their tariff and regardless how much we'd all prefer they didn't I don't really think anyone can fairly argue that it's unreasonable for them to do so.It's always been clear that this is a beta tariff - i.e. new and not fully tested - so fair game for them to change things in the light of testing. And common sense should say that in a time of high inflation the fixed element will need to be increased at some time to reflect rising costs. And difficult to justify having lower standing charges. So personally I've no objection to the principle of a price hike. Octopus smart tariffs are still some of the best value tariffs around.Also, there's no point in getting hot under the collar about notice periods etc.. Octopus have always been reasonable in the past and there's no reason I can think of to suggest it will be any different now. The time to worry about unreasonable notice periods is if and when it happens.Price rises are a fact of life - best just suck it up IMHO. And if it makes Tracker unattractive it's always possible to move without notice or penalty.5

-

The EPG last year meant that my 40p/11p caps became 34p/10.4p (V3 tracker with end date of June 2023). We hit those caps quite a lot last year too so you could say we had our cake and ate it too. We got lower rates on cheap days but never had to pay more than flexible. On renewal I got an end date for electricity but not for gas.bristolleedsfan said:

Agile and Tracker tariffs would not be subject to price cap as a variable tariff with no end date. (I know they say this and that). Agile/Tracker tariffs seemingly qualified for EPG discount for new signups after 1 October 2022 as a variable tariff with no end date not subject to price cap.Bendo said:. The only reason it has an end date is to work around the price cap.2 -

With the July 2022 tariff we were protected from the high prices too; with a cap of 55p the first three months where we had the full 30+p discount meant we were fully protected. When the discount became 17p that still gave us an effective ceiling of 38p and I don't know if it ever went over the EPG rate then anyway, maybe once or twice but if so never far enough to exceed the discount.Griffindog said:

The EPG last year meant that my 40p/11p caps became 34p/10.4p (V3 tracker with end date of June 2023). We hit those caps quite a lot last year too so you could say we had our cake and ate it too. We got lower rates on cheap days but never had to pay more than flexible. On renewal I got an end date for electricity but not for gas.bristolleedsfan said:

Agile and Tracker tariffs would not be subject to price cap as a variable tariff with no end date. (I know they say this and that). Agile/Tracker tariffs seemingly qualified for EPG discount for new signups after 1 October 2022 as a variable tariff with no end date not subject to price cap.Bendo said:. The only reason it has an end date is to work around the price cap.

0 -

Post about EPG reduction in reply to subject of whether tracker tariff is subject to price cap as a variable tariff is irrelevant. two completely different schemes. Griffindog said:

Griffindog said:

The EPG last year meant that my 40p/11p caps became 34p/10.4p (V3 tracker with end date of June 2023). We hit those caps quite a lot last year too so you could say we had our cake and ate it too. We got lower rates on cheap days but never had to pay more than flexible. On renewal I got an end date for electricity but not for gas.bristolleedsfan said:

Agile and Tracker tariffs would not be subject to price cap as a variable tariff with no end date. (I know they say this and that). Agile/Tracker tariffs seemingly qualified for EPG discount for new signups after 1 October 2022 as a variable tariff with no end date not subject to price cap.Bendo said:. The only reason it has an end date is to work around the price cap.

0 -

I am.fairly relaxed about the new formula.proposal but have noticed some areas are +1p and others are +4p.

Those regions on +4p and the predictions for electricity prices next year could mean tracker becomes a regional product.

Maybe Octopus have not weighted the formula properly or maybe I am missing something.1 -

Prior to pricing changes I think I am correct that London had cheapest SC as well as one of the lowest (if not lowest) unit rate, December 2023 version has seen London unit rate increase by more than most other regions.1

-

MultiFuelBurner said:I am.fairly relaxed about the new formula.proposal but have noticed some areas are +1p and others are +4p.

Those regions on +4p and the predictions for electricity prices next year could mean tracker becomes a regional product.

Maybe Octopus have not weighted the formula properly or maybe I am missing something.An interesting observation. Looking at both sets of formulae, there is a slight increase in the spread for constant added on to the rate, which has gone up from a 1.5p range to a 1.8p range (the relative standard deviation has increased from 5.9% to 6.1%). London has gone from the second cheapest to second most expensive. NW and East of England have also gone from towards the cheaper end to towards the more expensive end. Some others have gone from lower-middle to upper-middle. In terms of the wholesale rate multiplier, this remains at a 0.8% RSD with only tiny tweaks made in the last decimal places.In terms of the final unit rate, the spread has gone up from about 1.6p to 1.9p, so I don't think that would make Tracker significantly less attractive in any specific region (I dare say the regional differences in SVT are aligned with these differences too). The main thing that has happened is that the relative price ranking of each region has shifted around. Yorkshire is now clear cheapest (after being neck and neck with London) and Merseyside+N Wales remains most expensive.2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards