We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Cash ISAs: The Best Currently Available List

Comments

-

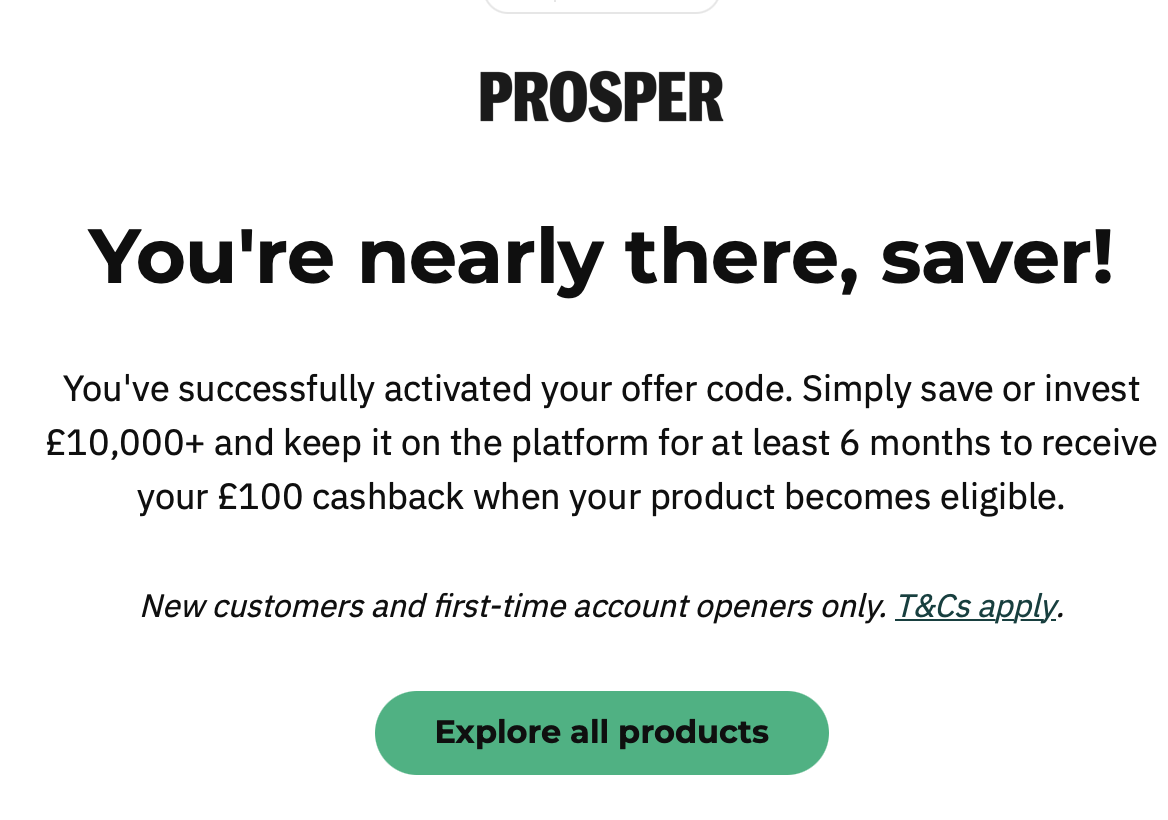

I've had a reply from Prosper regarding the funding window for their ISA

The account cannot be opened without being funded. There is no deadline for opening the account, however we cannot guarantee the rate for a specific amount of time.

The account will only be considered as open once it is funded.

In order to receive the boosted rate, £10,000 is the minimum amount to fund as mentioned in the app.

If you do not currently have the ISA allowance for £10,000, you will need to wait until the new tax year in order to fund the product.

3 -

I opened Prosper this morning (at 1.82%, not 1.92% bonus 😞) As part of the opening, I had to add money (into the Prosper wallet, then into the ISA) there and then. I couldn't see an open-and-don't-fund-yet.

2 -

Did you apply the other promo code for the extra £100 for holding >£10k for 6 months?

0 -

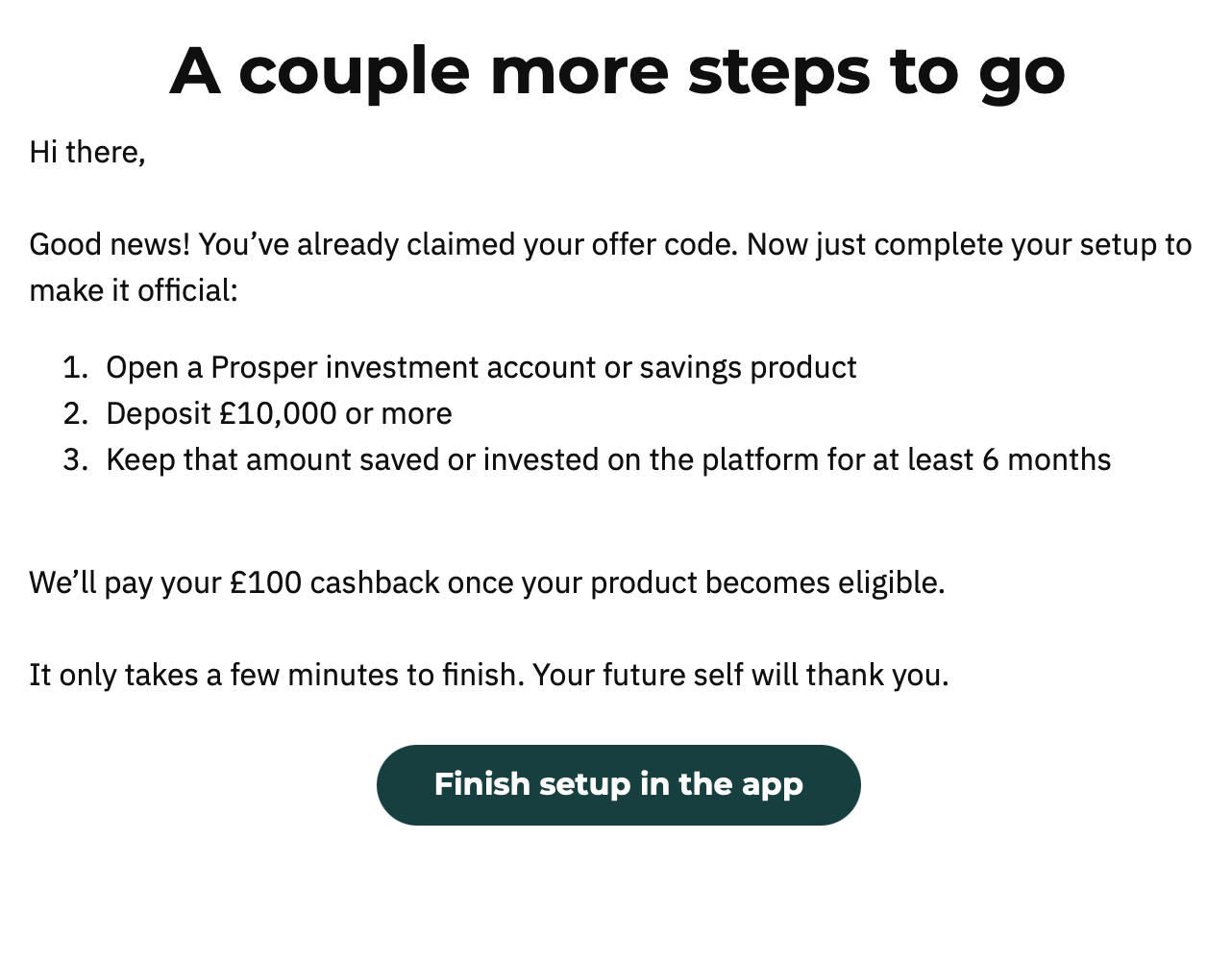

I did, yesterday when I first registered (without an open ISA) & received an email about the successful £100 registration.

In fact I planned to just open the ISA yesterday, then fund it whenever (like you were thinking of.) They had to verify my identity (which didn't take long), but when that was complete being registered for their app wasn't the same as opening an ISA account. Then I went to to try and open an ISA, to find a deposit was part of the opening.

2

2 -

Did the email say how soon you have to deposit the £10k in order to be eligible for the £100?

I'm thinking of doing this first stage now (to lock that part in), and just cross my fingers that the decent ISA rate is still available on the 6th April.

0 -

Nope. The part I screenshotted above links to these conditions;

;

where it says the offer period is "3.3. The Offer is valid from 5 November 2025 and will remain open until Prosper withdraws or varies it"

The email then lists these steps to take (without giving a date):

1

1 -

Furness 5yr now showing as 4.30%

2 -

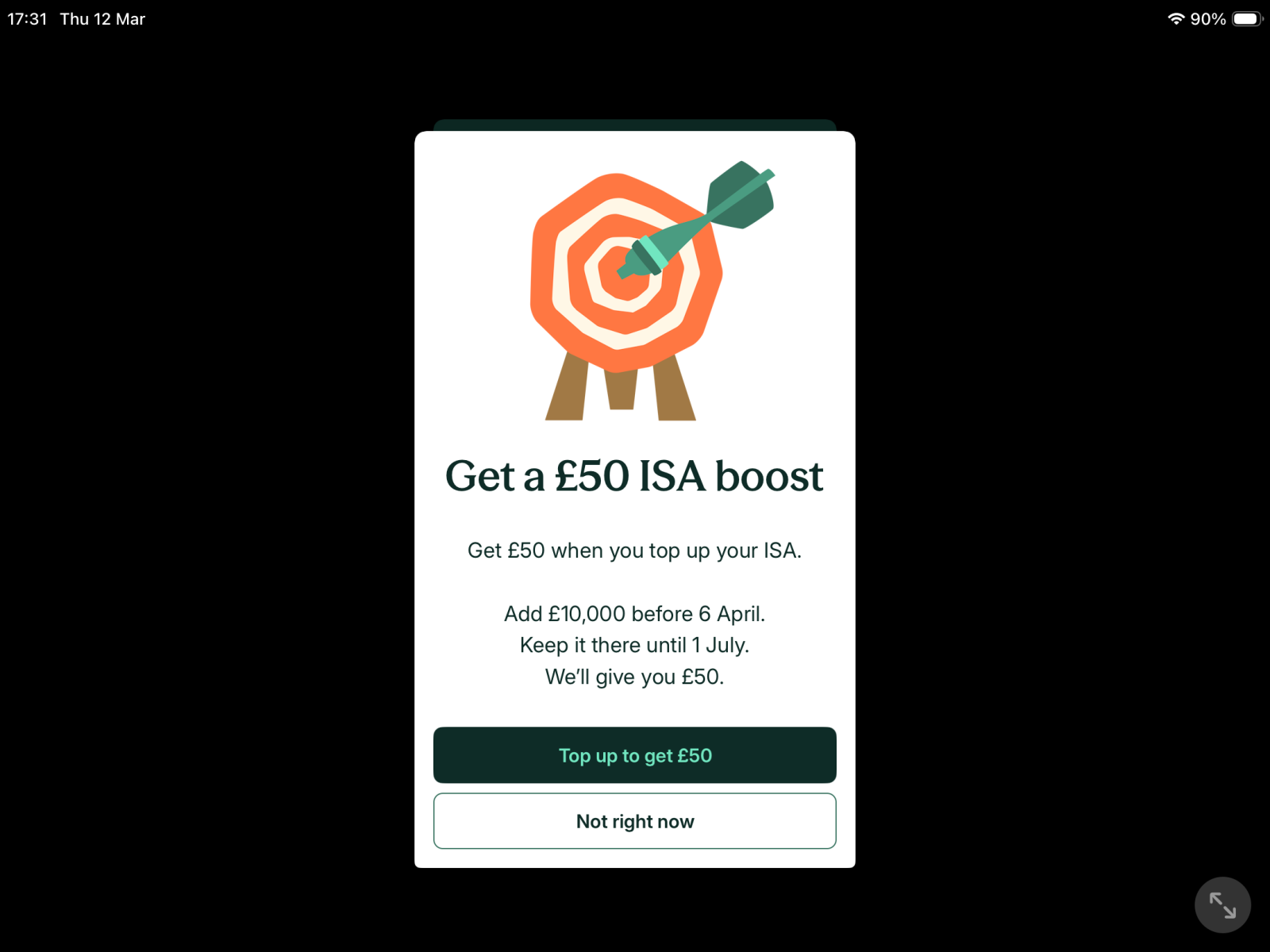

Zopa ISA boost

Just had this appear in my app

Might be of interest to anyone with a Zopa ISA that’s not fully funded yet.

1

1 -

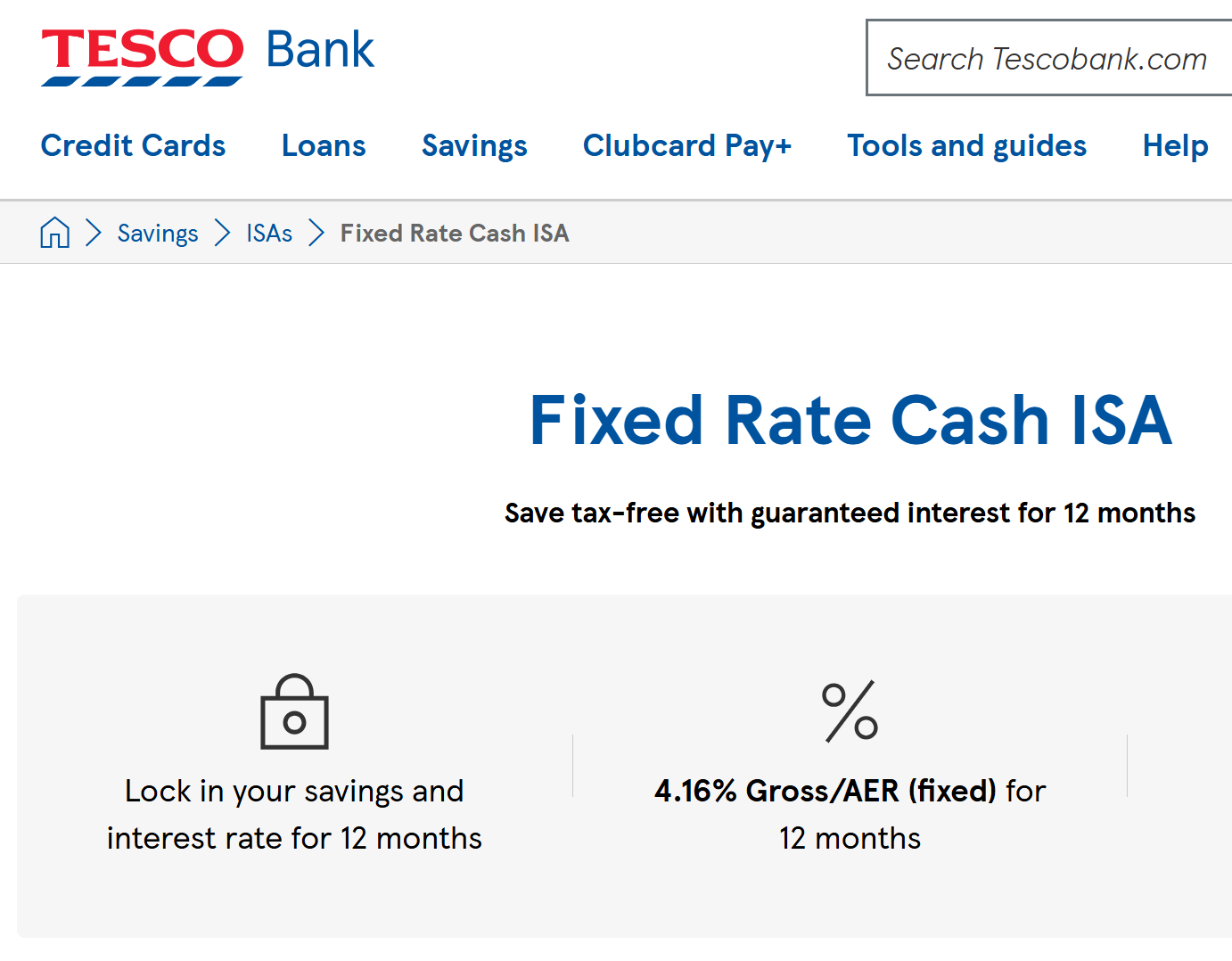

Just a heads - went to Tesco Bank as showing 4.2% for one year on MSE…….but website is showing 4.16% - not a lot of difference but just for info….

The Forum Member formally known as Pieman1972 (but failed to sort his account out!!)1

The Forum Member formally known as Pieman1972 (but failed to sort his account out!!)1 -

Regarding HSBC offer: I have Gatehouse fixed ISA coming to an end on May 7th. What are the chances that the funds can reach HSBC by 11th?

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards