We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

The Cashback for Bank or Investment Accounts Discussion Thread

Comments

-

As far as chargeable 'trades' go, no requirement to make any. Fidelity don't charge any dealing fees on funds. So an accumulating MM would work (or similar).

2 -

Fidelity S & S ISA via TCB

I transferred my S&S ISA out of Fidelity last July. I have no investments held with Fidelity any longer, but I can still log into the account and see my GIA, ISA and cash management account. There is a message when I click on the ISA etc.. which says some actions are not available. I have previously requested all accounts to be closed.

My question is would I be classed as a new customer and qualify for the TCB payout, has anyone else tried this ?

0 -

If you set up a Regular Savings Plan with Fidelity for £25 a month into a GIA (or ISA), the platform charge is 0.35% (rather than 0.45%)

0 -

Where are people seeing the £25 per month option on TCB? All I can see is lump sum options. Unless I have misunderstood?

0 -

There isn’t a £25 per month option on TCB - the offer is only for lump sum investments minimum 5K for £100 cashback.

The £25 per month is only to lower the 0.45% (£7.50pm on 20K) platform fee to 0.35%(£5.83pm on 20K). If you go for the full 20K into an ISA then you can set a Regular Savings Plan up on a GIA with Fidelity (or on the ISA if not investing the full 20K).

2 -

Personally I wouldn't expect that to work, as you wouldn't be a new customer. No harm in trying in one respect, but there is an opportunity cost of missing out on another ISA offer if you use this year's subscription on Fidelity. Best approach I feel would be to close your relationship with Fidelity, and possibly use another Fidelity offer in the future.

1 -

Yes that's just a workaround really if using the maximum subscription for the highest bonus. It's marginal at that level, but with one if the lower tiers it is important to set up the regular payment, which can then be to the ISA as well.

My preference with Fidelity was to keep the cash management account topped up.

1 -

Apols if this is a duplicate, on TCB but it's different to the one noted on page 1. So perhaps this has been generated due to the new tax year. But it's quite decent.

3

3 -

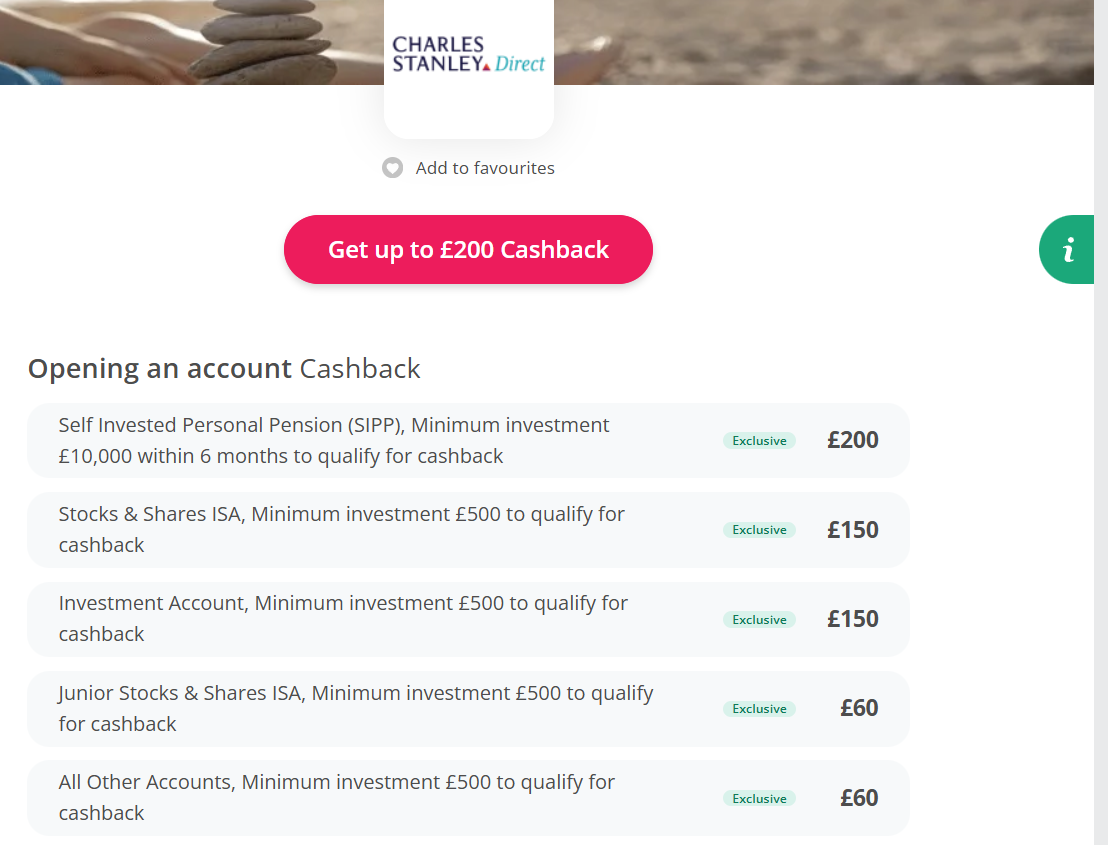

I've previously mentioned that CS are firmly on my naughty list. But given there's nothing in the terms to exclude previous/existing customers, nor to make these offers mutually exclusive, I'm going to be hard pressed to resist taking £150 for a £500 deposit in each of the ISA and Investment accounts…

1 -

Yes that is exactly my approach. If it goes pear shaped, £1K in a MM fund for a few months (less fees) isn't material.

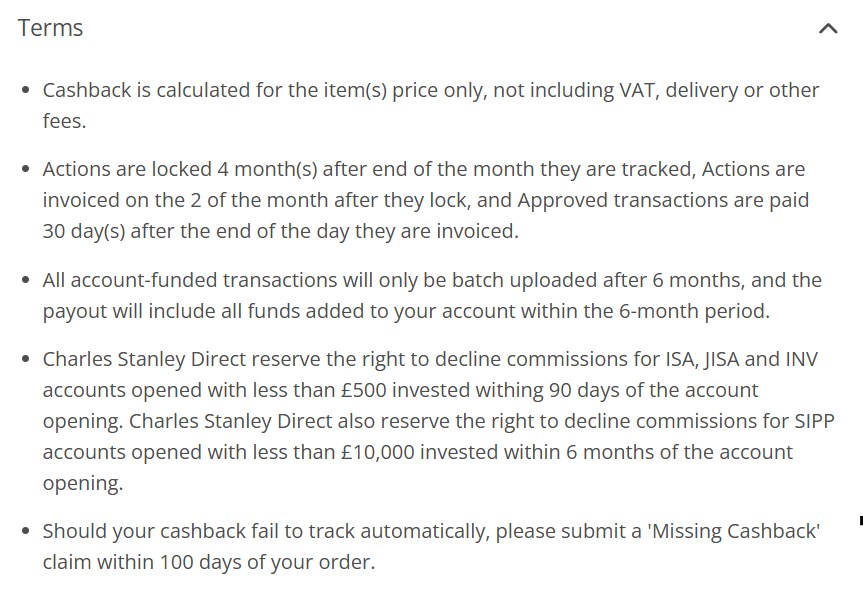

Probably worth dropping a shot of the terms here, if people can decipher exactly when they are meant to track and drop, they are better than me! My approach is to fund the 2*£500 immediately, check that it's tracked in 3 months and pay out should be within 7.

1

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards