We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Will / trust

Comments

-

Hallelujah 🥳 Just waiting for council tax letter. They said they need a reply from a solicitor so will need to sort that outposeidon1 said:

In passing, the solicitor's negligence in leaving your father as sole trustee and life tenant meant that he was in fact the sole owner of the entire property both legally ( as sole trustee) and beneficially in the eyes of trust and tax law. On this basis I believe you have a legitimate basis to claim entitlement to the empty property discount, and should strongly push for it on these facts.❤️Mum 2018

0% credit card £1360 & 0% Car Loan £7500 ~ paid in full JAN 2020 = NOW DEBT FREE 🤗

House sale OCT 2022 = NOW MORTGAGE FREE 🤗

House cash purchase completed FEB 2023 🥳🍾 & left work. 🤗

Retired at 55 & now living off the equity £10k a year

❤️Dad 2025

Previous Savings diary https://forums.moneysavingexpert.com/discussion/5597938/get-a-grip/p1

Living off savings diary

https://forums.moneysavingexpert.com/discussion/6429003/escape-to-the-country-living-off-savings/p10 -

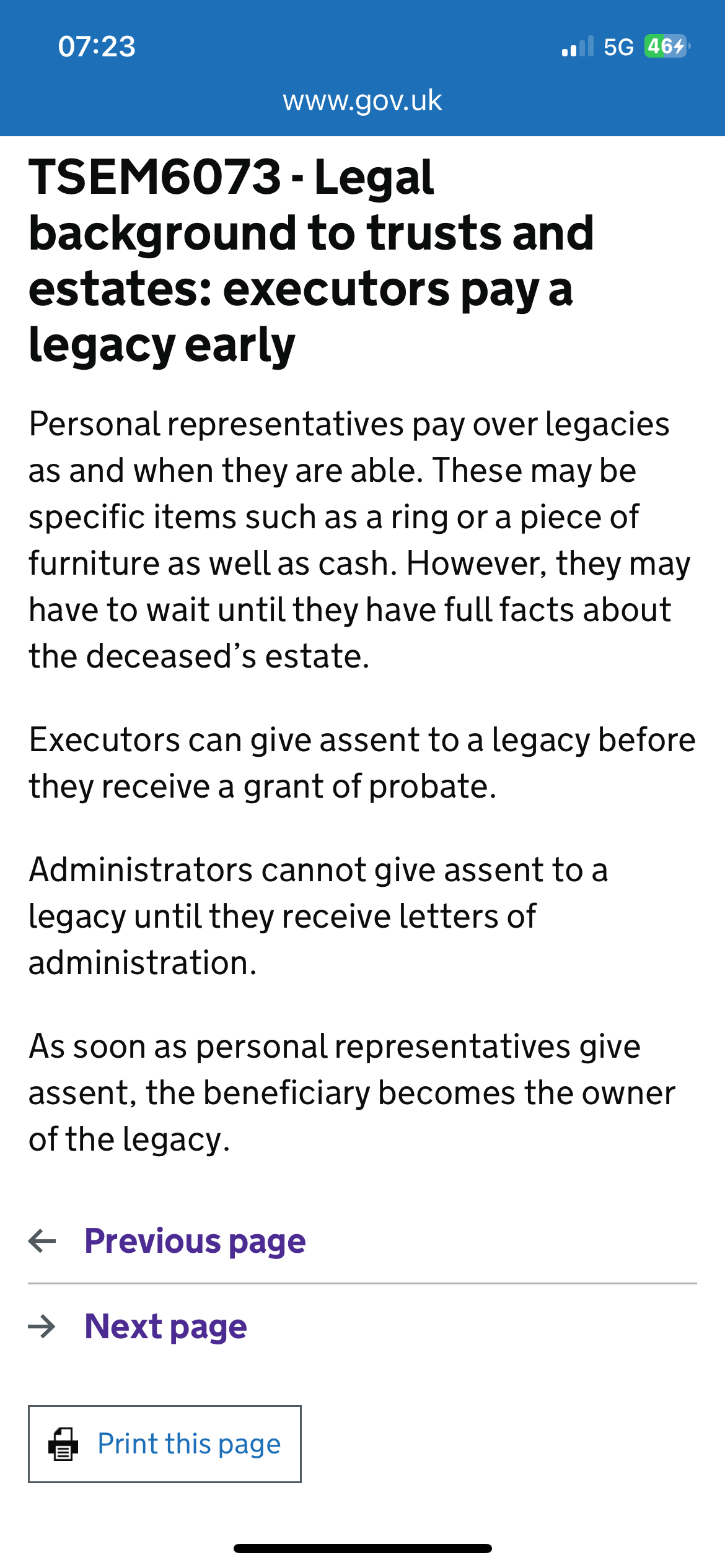

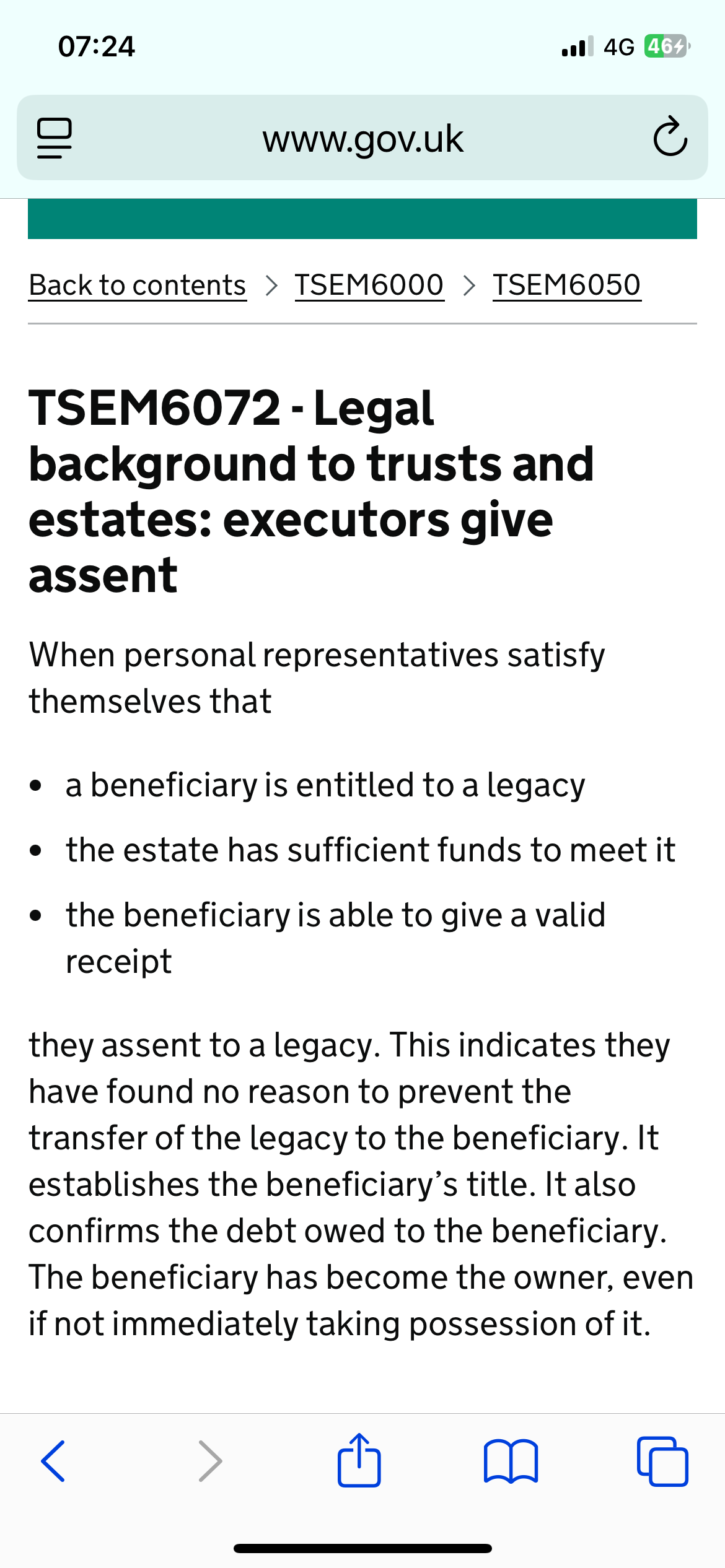

Hope you don’t mind me asking a question about a pecuniary legacy?We have one in a codicil for £3k. How soon can we start to distribute the estate after probate? There will be sufficient money in the estate to pay this pecuniary legacy after debts are paid, but before the house is sold / sale fees are paid.

I see we have one year from date of death before interest is due but we are not likely to get an interest rate of the amount specified in a savings account on a £3k balance?Does it have to be an executor savings account? It was hard enough to open just an ordinary executor account.

❤️Mum 2018

0% credit card £1360 & 0% Car Loan £7500 ~ paid in full JAN 2020 = NOW DEBT FREE 🤗

House sale OCT 2022 = NOW MORTGAGE FREE 🤗

House cash purchase completed FEB 2023 🥳🍾 & left work. 🤗

Retired at 55 & now living off the equity £10k a year

❤️Dad 2025

Previous Savings diary https://forums.moneysavingexpert.com/discussion/5597938/get-a-grip/p1

Living off savings diary

https://forums.moneysavingexpert.com/discussion/6429003/escape-to-the-country-living-off-savings/p10 -

You may have seen the recent thread below:Skint_yet_Again said:Hope you don’t mind me asking a question about a pecuniary legacy?We have one in a codicil for £3k. How soon can we start to distribute the estate after probate? There will be sufficient money in the estate to pay this pecuniary legacy after debts are paid, but before the house is sold / sale fees are paid.

I see we have one year from date of death before interest is due but we are not likely to get an interest rate of the amount specified in a savings account on a £3k balance?Does it have to be an executor savings account? It was hard enough to open just an ordinary executor account.

https://forums.moneysavingexpert.com/discussion/comment/81668387#Comment_81668387

Frankly the rigidity of rules relating to interest payable on pecuniary legacies after elaspe of the estate year together with difficulty in sourcing accounts to accrue such interest, I would aim to settle the £3000 within the deadline.

The extra work and effort involve if the deadline is missed is simply disproportionate for the sum involved.

2 -

I saw this and thought we could pay the pecuniary amount as soon as we have probate?

❤️Mum 2018

0% credit card £1360 & 0% Car Loan £7500 ~ paid in full JAN 2020 = NOW DEBT FREE 🤗

House sale OCT 2022 = NOW MORTGAGE FREE 🤗

House cash purchase completed FEB 2023 🥳🍾 & left work. 🤗

Retired at 55 & now living off the equity £10k a year

❤️Dad 2025

Previous Savings diary https://forums.moneysavingexpert.com/discussion/5597938/get-a-grip/p1

Living off savings diary

https://forums.moneysavingexpert.com/discussion/6429003/escape-to-the-country-living-off-savings/p10 -

I paid the pecuniary legacies long before gaining Confirmation (probate) after the lawyer said it was fine to do so as long as my brother agreed.Skint_yet_Again said:I saw this and thought we could pay the pecuniary amount as soon as we have probate?0 -

Thanks @jem16 we don’t have a lawyer yet but will need one for selling the house & probably a letter for council tax. However if we are doing probate ourselves and can see that there are enough funds to cover all expenses I think we will pay all debts (water bill to date of death) and the pecuniary legacy once we have probate and can access funds.❤️Mum 2018

0% credit card £1360 & 0% Car Loan £7500 ~ paid in full JAN 2020 = NOW DEBT FREE 🤗

House sale OCT 2022 = NOW MORTGAGE FREE 🤗

House cash purchase completed FEB 2023 🥳🍾 & left work. 🤗

Retired at 55 & now living off the equity £10k a year

❤️Dad 2025

Previous Savings diary https://forums.moneysavingexpert.com/discussion/5597938/get-a-grip/p1

Living off savings diary

https://forums.moneysavingexpert.com/discussion/6429003/escape-to-the-country-living-off-savings/p10 -

As long as the estate has the funds after debts expenses and IHT has been covered pecuniary legacies can be paid as soon as you like. You don’t even need to wait until you have probate.

2 -

poseidon1 said:I have noted the difference interpretation of how CGT disposals of life interest trust assets are dealt with after death of life tenant and remaindermen are now absolutely entitled to those assets against the trustees. Fortunately the relatively short summation from HMRC manuals attempts to explain as below -

https://www.gov.uk/hmrc-internal-manuals/trusts-settlements-and-estates-manual/tsem6361

Key points to note for life interest trusts:

* On death of life tenant, trust assets are amalgamated with personal assets of the deceased but purely for the purposes of ascertaining the overall charge to IHT. Here the deceased's nil rate band is shared proportionally between the life interest trustees and the deceased estate executors.

* Any IHT that may then become due is split between the life interest trustees and the estate, with each liable for their own share.

* Importantly there has been no de facto merger of life interest trust assets ( following death) with the free estate assets, other than to calculate IHT. The life interest trustees have now become bare trustees answerable to the remaindermen and must convey to them the trust fund net of the trust's share of any IHT due.

* Where, as in the present case, the trustees will be party to a sale of an asset which is also owned by the free estate ( ie the 50:50 shares of the house), as indicated by HMRC guidance the trustees will be selling their share as bare trustees for the absolute benefit of the remaindermen with any gain arising after the market value uplift, attributable to the remainderman in their personal capacity with their individual CGT exemptions available as a result.

* in the case of the executors of the free estate, their sale follows usual estate sale principles with a single estate CGT exemption available for up to 3 tax years post death.

I admit, this continued separation between trust and estate assets after death of life tenant is more difficult to discern where trustees, trust remainderman, estate executors, and residuary estate beneficiaries are all the same people wearing multiple hats they are largely unaware of and the primary asset is the family home. In that scenario they will more than likely see themselves as mere residuary estate beneficiaries, overlooking the fact there is also a separate 'bare trust' that can work to their advantage.

That separation is more easily recognised ( and understood ) where the trustees and beneficiaries of the life interest trust, differ completely from those who benefit from the deceased's estate.

Outside of professionally administered trusts ( my previous area of work), lay people will more readily recognise this separation in cases where the married couple have children from prior relationships , and each parent wants to make separate and distinct provision for their own offspring using an IPDI trust for that purpose.

As we have seen on this forum, in these blended family situations the children of the first spouse to die will often be trustees and remainderman of one half of the house occupied by the survivor, whilst children of the surviving parent/life tenant end up being executors of that deceased's estate. Here there should be less scope for confusion as to their respective roles, and duties and specifically who is responsible for and liable to CGT when the house is eventually sold.

As a final observation, I have no doubt many families in the OP's circumstance lose the opportunity to apply multiple CGT exemptions where the family home is eventually sold, due to not understanding the concept of a continuing 'bare trust' for remainderman of the IPDI trust, which can potentially be utilised to their advantage.Could you please explain how this sharing of the nil rate band works in practice? Do we use the NRB in a certain order?Eg gifts £42,000

bank accounts £150,000

house £170,000 (50% from the trust)

total £362,000

nrb £325,000 transfer unused from spouse £265,000

IHT due nil?❤️Mum 2018

0% credit card £1360 & 0% Car Loan £7500 ~ paid in full JAN 2020 = NOW DEBT FREE 🤗

House sale OCT 2022 = NOW MORTGAGE FREE 🤗

House cash purchase completed FEB 2023 🥳🍾 & left work. 🤗

Retired at 55 & now living off the equity £10k a year

❤️Dad 2025

Previous Savings diary https://forums.moneysavingexpert.com/discussion/5597938/get-a-grip/p1

Living off savings diary

https://forums.moneysavingexpert.com/discussion/6429003/escape-to-the-country-living-off-savings/p10 -

Gift made in the previous 7 years first, if anything left it is usually pecuniary bequests that come next (wills will often state these are to be given free of IHT), the residual state uses the rest and pays any tax due.The exact terms of the will could change the above.0

-

Thanks @Keep_pedalling the pecuniary bequest was going out of a codicil 3k & nothing about being free of IHT. If the exact terms of the will may change everything I am definitely going to have to see a solicitor.❤️Mum 2018

0% credit card £1360 & 0% Car Loan £7500 ~ paid in full JAN 2020 = NOW DEBT FREE 🤗

House sale OCT 2022 = NOW MORTGAGE FREE 🤗

House cash purchase completed FEB 2023 🥳🍾 & left work. 🤗

Retired at 55 & now living off the equity £10k a year

❤️Dad 2025

Previous Savings diary https://forums.moneysavingexpert.com/discussion/5597938/get-a-grip/p1

Living off savings diary

https://forums.moneysavingexpert.com/discussion/6429003/escape-to-the-country-living-off-savings/p10

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards