We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Will / trust

Comments

-

Savvy_Sue said:

I can't see a problem. It seems unlikely that an unrelated "Joe Bloggs" would pop up and say "Fred meant to leave that to me rather than to his grandson”Skint_yet_Again said:Thanks @Savvy_Sue

The codicil says for example…. I leave “Joe bloggs” £3000

The name matches one of the grandchildren. We know it was intended to be left to the grandchild of that name but it isn’t specified.

Not sure where this leaves us ?Thank you so much @Savvy_Sue you have set my mind at rest especially about the above. I imagined loads of “Joe Bloggs” turning up wanting £3000. All codicil beneficiary names are known to us and they are the only people with those names in the family. I have drawn up a family tree and will get copies of birth certificates to file with executor accounts (not for distribution).I am so grateful for everyone who helps on this board.So I am hopefully not far off applying for probate. Still waiting for P45 figures from one company pension. I think they are holding out until we repay the pension overpaid after date of death. If no reply by the time I get back from holiday I will get figures of final monthly pension and estimate the tax refund.Final of 3 estate agents visiting today. Estate agent 1 was very dismissive and gave a low value £155-£160k as a 2 bed & loft room built 1970’s & not known if planning/ building regs. Estate agent 2 was very positive, said don’t worry about planning/ building regs, commented that there’s plenty of space in walk-through bedroom for new buyers to insert a stud wall if they wanted & valued at £170k. No prizes for guessing who gets my vote at the moment!Do we need to get the will & codicil verified as valid before put the house on the market or before we apply for probate?We collected the will from the solicitor that wrote it and found the codicil in dads safe signed & witnessed by 2 of dads neighbours (not beneficiaries).

Edited to add it appears to follow this format

https://coronerscourtssupportservice.org.uk/wp-content/uploads/2021/11/Codicil-Website-Factsheet-121121.pdf❤️Mum 2018

0% credit card £1360 & 0% Car Loan £7500 ~ paid in full JAN 2020 = NOW DEBT FREE 🤗

House sale OCT 2022 = NOW MORTGAGE FREE 🤗

House cash purchase completed FEB 2023 🥳🍾 & left work. 🤗

Retired at 55 & now living off the equity £10k a year

❤️Dad 2025

Previous Savings diary https://forums.moneysavingexpert.com/discussion/5597938/get-a-grip/p1

Living off savings diary

https://forums.moneysavingexpert.com/discussion/6429003/escape-to-the-country-living-off-savings/p10 -

You can't finalise sale before you've got probate, and that will take time.

I have no idea how you'd verify a will other than by applying for probate.

Many would put house on market before obtaining probate, but estate agent must be aware it's a probate sale, and tell potential buyers. It will put some people off, because no-one can predict how long it will take, but doing it yourselves will be faster than using solicitors.Signature removed for peace of mind1 -

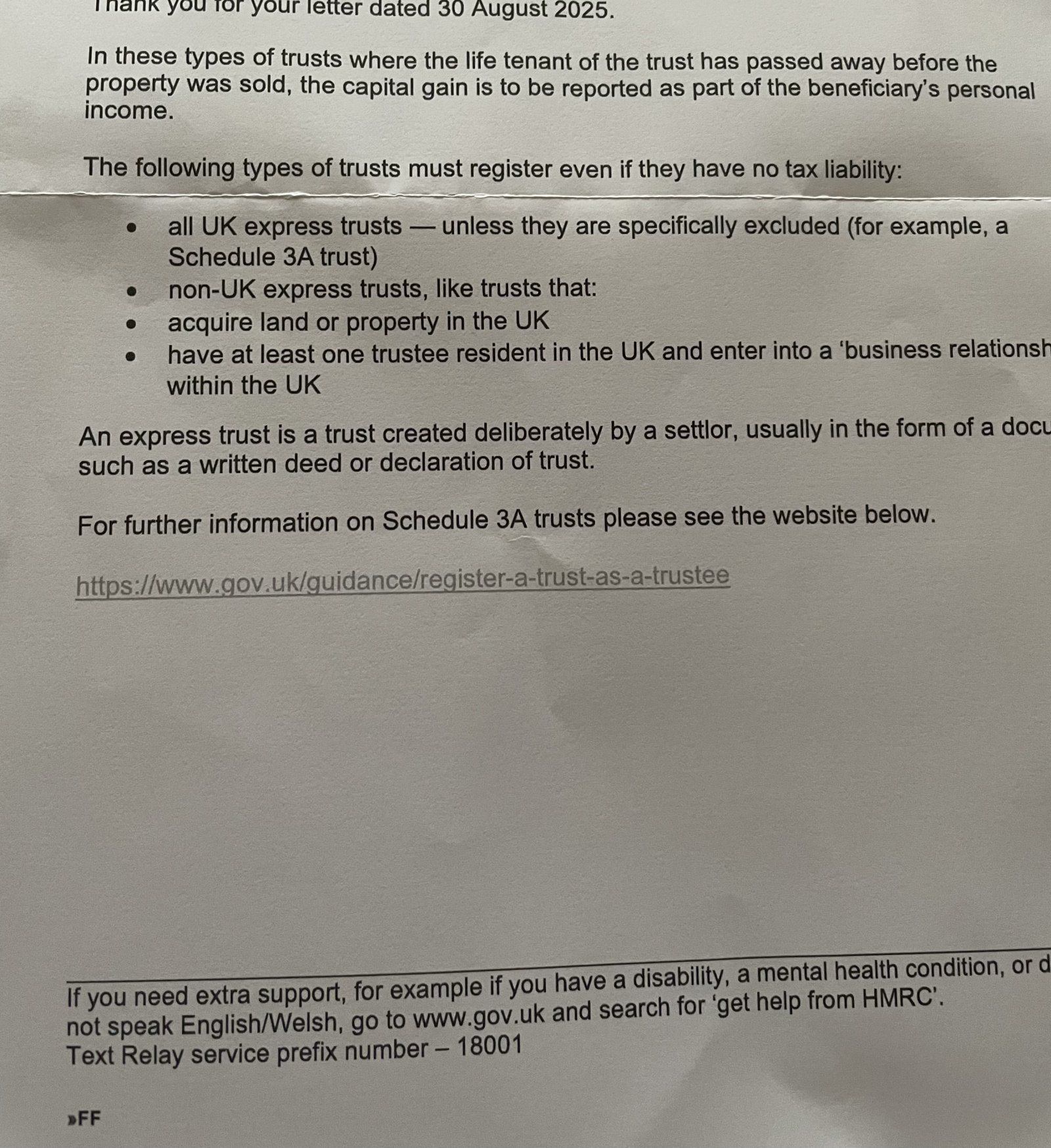

I wrote to HMRC Trusts as above and advised mums will (edit to add dated 2018) created a trust with dad as trustee with a life interest to remain living in the property. Dad has now passed away and it has come to light that the trust should have been registered by Sept 22. The trust ended when dad died and the property now forms part of dad’s estate. Is it really necessary to register a trust which has since terminated without ever giving rise to any trustee tax liability during its existence.poseidon1 said:Skint_yet_Again said:Thanks @poseidon1 and @RAS as soon as I have some figures I will come back. Estate agents booked for valuation (under £200k would expect £160-£180k total including trust share) savings £150k ish waiting for statements/ ISAS, contents no real collectables have been checking eBay nothing over £100 ish. Car = just about to get quotes from auto trader/ we buy ani car & motor way. (7,000 ish). Do expenses for solicitors/ tax come off to reach the total figure or is it gross amount?RAS sorry I missed your post earlier. Yes we missed the change in 2022 requiring us to register the trust. We were expecting to pay CGT as house has increased a lot due to house market going up since 2018 when mums trust was created.

A very modest estate totalling around £350k -£360k including car?

On this basis and notwithstanding the termination of your father's trust on death, I believe the estate qualifies as an excepted estate for probate purposes - see HMRC guidance below -

https://www.gov.uk/valuing-estate-of-someone-who-died/check-type-of-estate

The terminated trust is well under the £250k threshold ( only £90k at the top end of 50% of the house value), whilst personal assets, chattels and the other 50% of the house comes in at around £270k.

At most only your mother' s transferable NRB of £325k is required here together with your father's NRB, so you can ignore the residence nil rate bands for both your mother and father entirely.

Suggest once you have your finalised and compiled all the numbers for estate assets and liabilties, follow the link for excepted estate reporting in the HMRC guidance above , and you should find you can apply for probate yourselves without professional assistance.

As for overlooking registration of your father's trust created by your mother, suggest you write to HMRC in the 1st instance, setting out the events and mitigation you have explained here, and ask if there is much point registering a trust which has since terminated without ever giving rise to any trustee tax liabilties during its exsistence.

Hopefully HMRC's trust inspectorate will be of the view they have more important things to concern themselves than a now defunct trust.

Overall it would be ashame incurring professional fees for such a modest estate, not withstanding the slight complication with the trust.Can anyone explain their reply because it makes no sense to me ? 😕 Grateful for any help ❤️Mum 2018

❤️Mum 2018

0% credit card £1360 & 0% Car Loan £7500 ~ paid in full JAN 2020 = NOW DEBT FREE 🤗

House sale OCT 2022 = NOW MORTGAGE FREE 🤗

House cash purchase completed FEB 2023 🥳🍾 & left work. 🤗

Retired at 55 & now living off the equity £10k a year

❤️Dad 2025

Previous Savings diary https://forums.moneysavingexpert.com/discussion/5597938/get-a-grip/p1

Living off savings diary

https://forums.moneysavingexpert.com/discussion/6429003/escape-to-the-country-living-off-savings/p10 -

Sya, can a solicitor sort this out? when each of my parent's died, the solicitor dealt with they probate and we didn't really get involved but any worry like this would have been handled by them. This seems very hard to deal with yourself?0

-

@poseidon1 and others advised there is no CGT liability to the trust so I don’t understand why HMRC mention CG. I also don’t understand the part about express trusts as there is no written deed or declaration of trust. This is an IPDI trust so I would be grateful for any further advice. I don’t want to pay a solicitor until I understand what is going on. If it’s above my pay grade that’s fair enough but most of the advice given on here is backed up by trust manual or HMRC guidance. If needs be I will phone HMRC & speak to a higher grade. Was fairly impressed with the quick response even though I don’t have a clue what they are talking about 😂❤️Mum 2018

0% credit card £1360 & 0% Car Loan £7500 ~ paid in full JAN 2020 = NOW DEBT FREE 🤗

House sale OCT 2022 = NOW MORTGAGE FREE 🤗

House cash purchase completed FEB 2023 🥳🍾 & left work. 🤗

Retired at 55 & now living off the equity £10k a year

❤️Dad 2025

Previous Savings diary https://forums.moneysavingexpert.com/discussion/5597938/get-a-grip/p1

Living off savings diary

https://forums.moneysavingexpert.com/discussion/6429003/escape-to-the-country-living-off-savings/p10 -

Skint_yet_Again said:@poseidon1 and others advised there is no CGT liability to the trust so I don’t understand why HMRC mention CG. I also don’t understand the part about express trusts as there is no written deed or declaration of trust. This is an IPDI trust so I would be grateful for any further advice. I don’t want to pay a solicitor until I understand what is going on. If it’s above my pay grade that’s fair enough but most of the advice given on here is backed up by trust manual or HMRC guidance. If needs be I will phone HMRC & speak to a higher grade. Was fairly impressed with the quick response even though I don’t have a clue what they are talking about 😂

The first sentence of the letter from HMRC would have been enough in the circumstances.

I don't know what prompted the comment about capital gains but it isn't an acceptable or complete explanation of the position for capital gains when the property is sold after the life tenant of the IPDI trust (your Dad) has passed.

The IPDI trust was a express trust created by your Mum's will; that trust has ended.

When probate for your Dad's will is granted, the executors can sell the property. If it sells for more than the date of death/probate value a capital gain will arise and the estate will be liable for any capital gains tax.

The beneficiaries individually would be liable for capital gains tax if the property was transferred to them before it is sold. In your situation transferring the property to the beneficiaries is not needed in order to sell the property.

File the letter which acknowledges you have notified HMRC of the trust (which has ended), it is all you needed to do in respect of the trust.

It seems you now have all you need to make the probate application and then to go ahead with the sale of the property by the estate when it is granted.

0 -

Thank you @mybestattempt for taking the time to explain it so clearly.

If it is an express trust I believe it would not be excluded and so I would have to register? I believe this was what @poseidon1 was hoping I could avoid by sending the letter. Is it worth phoning with a complaint? I put a lot of other information in the letter about the circumstances and mitigating factors and they have not even responded to that part, not mentioned anything about penalties or reasonable excuse, or even given any condolences.If I have to register the trust how do I register it and then close it? Do we have to come up with a name for it? I assume I would then have to wait for automatic penalties and appeal. Again a lot of bureaucratic nonsense and unnecessary work.❤️Mum 2018

0% credit card £1360 & 0% Car Loan £7500 ~ paid in full JAN 2020 = NOW DEBT FREE 🤗

House sale OCT 2022 = NOW MORTGAGE FREE 🤗

House cash purchase completed FEB 2023 🥳🍾 & left work. 🤗

Retired at 55 & now living off the equity £10k a year

❤️Dad 2025

Previous Savings diary https://forums.moneysavingexpert.com/discussion/5597938/get-a-grip/p1

Living off savings diary

https://forums.moneysavingexpert.com/discussion/6429003/escape-to-the-country-living-off-savings/p10 -

Skint_yet_Again said:Thank you @mybestattempt for taking the time to explain it so clearly.

If it is an express trust I believe it would not be excluded and so I would have to register? I believe this was what @poseidon1 was hoping I could avoid by sending the letter. Is it worth phoning with a complaint? I put a lot of other information in the letter about the circumstances and mitigating factors and they have not even responded to that part, not mentioned anything about penalties or reasonable excuse, or even given any condolences.If I have to register the trust how do I register it and then close it? Do we have to come up with a name for it? I assume I would then have to wait for automatic penalties and appeal. Again a lot of bureaucratic nonsense and unnecessary work.

My own view is you have done enough by notifying HMRC of the trust, including the fact it has ended.

Unfortunately, however, the very poor response from HMRC does not give you reassurance about whether you need to formally register it online and then close it down nor does it mention penalties.

I would telephone HMRC to seek clarification on both points and recommend you make a written note of what is said.

Even if you do need to formally register the trust I think it is unlikely any penalties would be imposed because the late registration was not deliberate:

https://www.litrg.org.uk/tax-nic/trusts-and-estates/trust-registration-service

https://www.gov.uk/hmrc-internal-manuals/trust-registration-service-manual/trsm80020

1 -

Skint_yet_Again said:Thank you @mybestattempt for taking the time to explain it so clearly.

If it is an express trust I believe it would not be excluded and so I would have to register? I believe this was what @poseidon1 was hoping I could avoid by sending the letter. Is it worth phoning with a complaint? I put a lot of other information in the letter about the circumstances and mitigating factors and they have not even responded to that part, not mentioned anything about penalties or reasonable excuse, or even given any condolences.If I have to register the trust how do I register it and then close it? Do we have to come up with a name for it? I assume I would then have to wait for automatic penalties and appeal. Again a lot of bureaucratic nonsense and unnecessary work.

Firstly agree @mybestattempt, ignore HMRC reference to CGT.

Trust has terminated so any potential exposure sits personally with the trust remainderman for the ex trust half share and the other half via your father's estate, in due course. £3k CGT exemptions across the estate and trust beneficiaries should be available if you are lucky to sell at a profit.

As for the trust registration, looks as if HMRC completely missed the point relating to its termination with no tax liabilities arising thereon. Looks as if they simply churned out a non personalised standard response.

Sadly therefore , they are putting you to the trouble of registering online via a link embedded within the following guidance ( scroll towards the bottom of the guidance ) -

https://www.gov.uk/guidance/register-a-trust-as-a-trustee

Had a quick look to see if your trust could claim a Schedule 3A exclusion from registration, but you don't qualify.

Once registered, you should immediately update the trust record to show the termination date of the trust ( your fathers date of death). At some point in time you may then get a follow up acknowledgement from HMRC. Hopefully you have retained a copy of your original mitigation letter for the purposes of resubmission, if HMRC have the temerity to raise the issue of a potential penalty.

Regrettably you are being put to a lot of work for a modest sized trust/estate. Unfortunately there is no proportionality where trusts are concerned.

1 -

Thank you @mybestattempt you are right I am not reassured by HMRC response. I will telephone and complain and seek clarification but believe that they will still make me register. Thank you for your help & the links.

Thank you @poseidon1 the house has been valued by 3 estate agents and top value is £170k from 2 agents so I will use that for probate. If the house sells for more I see that you said the trust remaindermen would be personally responsible for any CGT on the trust half. I was under the impression that the trust had ended & the property was not transferred to the remaindermen until after it is sold? I’ve never calculated CGT but assume can deduct estate agent/ solicitor/ accountant fees? Could we also deduct unoccupied house insurance fee or is that an expense of the estate?If remaindermen are personally responsible for half any potential CGT could this be taken from the estate shares before distribution? If necessary 2 executors / remaindermen/ beneficiaries could pay from personal funds but we would have to pay for 3rd remainderman/ beneficiary up front and would likely not get it back once the estate has been distributed. (The 3rd remainderman has renounced as executor of trustee / life tenant).I have looked at the links. If we have to register the trust I would imagine it would be by me as executor of the deceased trustee / life tenant (dad) for a deceased settlor (mum) of a non-taxable express trust. It says I will need the name of the trust (there is no name/ no trust deed) & details of any land or property that the trust has purchased (none as property was transferred in will?). So I believe I would not include details of the property? The beneficiaries would be the 3 named in the deceased settlors will.It also appears that I would have to apply for an “Organisation” Government Gateway user ID and password.Then I would need to amend and close the trust registration within 90 days of the change? Is this within 90 days of death of trustee / life tenant / closure of the trust? If so I am running out of time and will need to either diy or appoint a solicitor as soon as possible.Am now going to lie down in a dark room for a week 🫣 Thank you in advance for any further advice.❤️Mum 2018

0% credit card £1360 & 0% Car Loan £7500 ~ paid in full JAN 2020 = NOW DEBT FREE 🤗

House sale OCT 2022 = NOW MORTGAGE FREE 🤗

House cash purchase completed FEB 2023 🥳🍾 & left work. 🤗

Retired at 55 & now living off the equity £10k a year

❤️Dad 2025

Previous Savings diary https://forums.moneysavingexpert.com/discussion/5597938/get-a-grip/p1

Living off savings diary

https://forums.moneysavingexpert.com/discussion/6429003/escape-to-the-country-living-off-savings/p10

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards