We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

The Old Regular Savers Discussion Thread 28/12/24-29/1/26

Comments

-

You haven’t taken in to account that if you open it now,, when it matures on the 22/09/26 you could put the whole proceeds into an easy access account for a week until the 29/09/26, which would earn you around £2 more in interest, so the benefit of delaying is much less than you have suggested.Bobblehat said:

A good point .... but .....Stargunner said:

Why don't you open the new RS now, so that you can be earning interest on your first deposit of £200.Bobblehat said:

I'll risk it! The NW agent I spoke to insisted on looking up the rate of the current offering when I mentioned about opening a new one later in the month (I already knew the rate). His wording was slightly worrying ... "It's still 6.5%, at the moment!". I should have asked if there was an expected drop imminent, but knew I would get a non-committal answer.friolento said:

It might not be available any longer on the 29th.Bigwheels1111 said:Bobblehat said:

If it's of interest(!), opened the RS 22/09/2024, funded it 22/09 & 01/10 and then by SO on 01/11 until 01/09/2025, so closing balance was £2693.67.Bigwheels1111 said:Hattie627 said:Nationwide BS Flex Regular Saver

My Issue 3 Flex RS has its maturity date today. Interest has been added (£93.46). I have moved the balance plus interest out. The account is still showing as a Flexible RS which is preventing me opening a new one (now Issue 7). I can't remember what happened last year. Has anyone any recent experience of a Flex RS maturity and can recall when the account changes to an Instant Saver?Did you make an extra £200 payment this month, ie total £2600.I did and only got £93.42.Yes interest, I'm thinking of waiting until the 29th to open a new one so I can fund on the first as well to maxInterest this year. Then open on the 30th next year to do the same. As you need to wait a day to open.

OTOH, there might be a better offer during Savings Week, only available if you haven’t yet got the 6.5% one.

Choices, choises🤔")

It's a variable account anyway, so if it did drop between now and the 29th, I'd have probably only lost pennies. I have the choice to go elsewhere if the drop is drastic or NLA ... unlikely.

You previously said that you were leaving £400 in the current account to cover the first 2 payments. How much interest are you earning on the £400?

I could shift it out to Chase Saver and back 7 days later @ 4.65% gaining £0.28p over leaving it where it is (1%)....

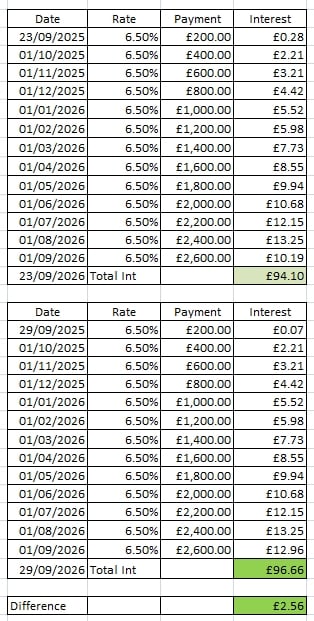

or, I could open the NW RS tomorrow and lose £2.56 over opening it on 29/09, (£94.10 maturing 22/09/2026 vs £96.66 maturing 28/09/2026).

So leaving the £400 where it is and not having to shift it around, and opening on 29th I'll have gained £2.56 over opening on 23rd but lost £0.28p for being a tad lazy! Do I loose an MSE point for being a tad lazy?1 -

This table does not take into account that the £2600 plus interest can be earning interest for 6 days from the 23/09/26 in another savings account, so the actual difference for delaying opening the account is negligiblerallycurve said:

Thanks for that. I understand now, basically you get 6 extra days at the end when you have the account full and that's what makes the difference!Bobblehat said:

OK ..... I'm glad I kept the rough working out spreadsheet! It would be 6 days BTW, as although I could have shifted the £400 I kept back today, I can't open the new RS until tomorrow at the earliest.rallycurve said:Bobblehat said:

A good point .... but .....Stargunner said:

Why don't you open the new RS now, so that you can be earning interest on your first deposit of £200.Bobblehat said:

I'll risk it! The NW agent I spoke to insisted on looking up the rate of the current offering when I mentioned about opening a new one later in the month (I already knew the rate). His wording was slightly worrying ... "It's still 6.5%, at the moment!". I should have asked if there was an expected drop imminent, but knew I would get a non-committal answer.friolento said:

It might not be available any longer on the 29th.Bigwheels1111 said:Bobblehat said:

If it's of interest(!), opened the RS 22/09/2024, funded it 22/09 & 01/10 and then by SO on 01/11 until 01/09/2025, so closing balance was £2693.67.Bigwheels1111 said:Hattie627 said:Nationwide BS Flex Regular Saver

My Issue 3 Flex RS has its maturity date today. Interest has been added (£93.46). I have moved the balance plus interest out. The account is still showing as a Flexible RS which is preventing me opening a new one (now Issue 7). I can't remember what happened last year. Has anyone any recent experience of a Flex RS maturity and can recall when the account changes to an Instant Saver?Did you make an extra £200 payment this month, ie total £2600.I did and only got £93.42.Yes interest, I'm thinking of waiting until the 29th to open a new one so I can fund on the first as well to maxInterest this year. Then open on the 30th next year to do the same. As you need to wait a day to open.

OTOH, there might be a better offer during Savings Week, only available if you haven’t yet got the 6.5% one.

Choices, choises🤔

It's a variable account anyway, so if it did drop between now and the 29th, I'd have probably only lost pennies. I have the choice to go elsewhere if the drop is drastic or NLA ... unlikely.

You previously said that you were leaving £400 in the current account to cover the first 2 payments. How much interest are you earning on the £400?

I could shift it out to Chase Saver and back 7 days later @ 4.65% gaining £0.28p over leaving it where it is (1%)....

or, I could open the NW RS tomorrow and lose £2.56 over opening it on 29/09, (£94.10 maturing 22/09/2026 vs £96.66 maturing 28/09/2026).

So leaving the £400 where it is and not having to shift it around, and opening on 29th I'll have gained £2.56 over opening on 23rd but lost £0.28p for being a tad lazy! Do I loose an MSE point for being a tad lazy?I’d be curious to know the maths behind this. How can you earn £2.56 in 7 days on £200 in an account paying 6.5%?

Here you go ... usual qualifier, if you spot an error, let me know and I'll look and correct as necessary.

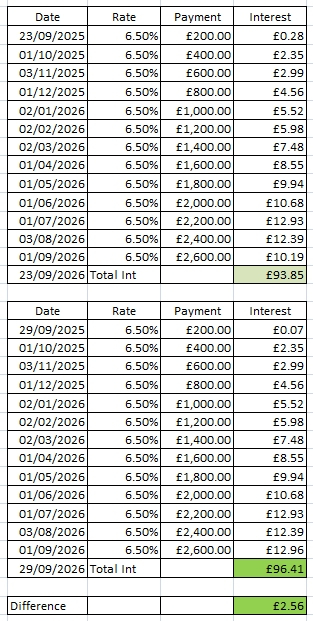

And for those who insist on a more accurate table showing payment dates for SO's on Bank working days ....

I have similar tables to above but showing a rate drop to 6.00% on 01/10/2025! Did I here a murmur of "Keep 'em to yourself"?2 -

Manchester BSMy faster payment of around 5pm is now showing in the RS. Nice, quick application as a new customer, and fast crediting of deposit. Would be even nicer if they had an app (which I gather is in the pipeline).

Withdrawals not possible until nominated account is verified, which involves them sending you a verification code in the snail mail.0 -

Well, not negligible - about 90p if my calculations are correct, if you're putting the matured funds in an easy-access account at 4%. However if the account is still available to renew at 6.5% on maturity, then any gains in funding on the 29th are wiped out. EDIT: mis-calculation, as you can only put £200 into the new account and the remainder will earn 4%. Still a gain of 84p for funding on the 29th. As you were.Stargunner said:

This table does not take into account that the £2600 plus interest can be earning interest for 6 days from the 23/09/26 in another savings account, so the actual difference for opening the account is negligiblerallycurve said:

Thanks for that. I understand now, basically you get 6 extra days at the end when you have the account full and that's what makes the difference!Bobblehat said:

OK ..... I'm glad I kept the rough working out spreadsheet! It would be 6 days BTW, as although I could have shifted the £400 I kept back today, I can't open the new RS until tomorrow at the earliest.rallycurve said:Bobblehat said:

A good point .... but .....Stargunner said:

Why don't you open the new RS now, so that you can be earning interest on your first deposit of £200.Bobblehat said:

I'll risk it! The NW agent I spoke to insisted on looking up the rate of the current offering when I mentioned about opening a new one later in the month (I already knew the rate). His wording was slightly worrying ... "It's still 6.5%, at the moment!". I should have asked if there was an expected drop imminent, but knew I would get a non-committal answer.friolento said:

It might not be available any longer on the 29th.Bigwheels1111 said:Bobblehat said:

If it's of interest(!), opened the RS 22/09/2024, funded it 22/09 & 01/10 and then by SO on 01/11 until 01/09/2025, so closing balance was £2693.67.Bigwheels1111 said:Hattie627 said:Nationwide BS Flex Regular Saver

My Issue 3 Flex RS has its maturity date today. Interest has been added (£93.46). I have moved the balance plus interest out. The account is still showing as a Flexible RS which is preventing me opening a new one (now Issue 7). I can't remember what happened last year. Has anyone any recent experience of a Flex RS maturity and can recall when the account changes to an Instant Saver?Did you make an extra £200 payment this month, ie total £2600.I did and only got £93.42.Yes interest, I'm thinking of waiting until the 29th to open a new one so I can fund on the first as well to maxInterest this year. Then open on the 30th next year to do the same. As you need to wait a day to open.

OTOH, there might be a better offer during Savings Week, only available if you haven’t yet got the 6.5% one.

Choices, choises🤔

It's a variable account anyway, so if it did drop between now and the 29th, I'd have probably only lost pennies. I have the choice to go elsewhere if the drop is drastic or NLA ... unlikely.

You previously said that you were leaving £400 in the current account to cover the first 2 payments. How much interest are you earning on the £400?

I could shift it out to Chase Saver and back 7 days later @ 4.65% gaining £0.28p over leaving it where it is (1%)....

or, I could open the NW RS tomorrow and lose £2.56 over opening it on 29/09, (£94.10 maturing 22/09/2026 vs £96.66 maturing 28/09/2026).

So leaving the £400 where it is and not having to shift it around, and opening on 29th I'll have gained £2.56 over opening on 23rd but lost £0.28p for being a tad lazy! Do I loose an MSE point for being a tad lazy?I’d be curious to know the maths behind this. How can you earn £2.56 in 7 days on £200 in an account paying 6.5%?

Here you go ... usual qualifier, if you spot an error, let me know and I'll look and correct as necessary.

And for those who insist on a more accurate table showing payment dates for SO's on Bank working days ....

I have similar tables to above but showing a rate drop to 6.00% on 01/10/2025! Did I here a murmur of "Keep 'em to yourself"?

Hopefully none of us are keeping our funds in a current account at 0% while we're waiting for the end of the month 0

0 -

I mistakenly missed out the word delaying (edited now), as i meant the difference in delaying opening the account is negligible to opening it now.clairec666 said:

Well, not negligible - about 90p if my calculations are correct, if you're putting the matured funds in an easy-access account at 4%. However if the account is still available to renew at 6.5% on maturity, then any gains in funding on the 29th are wiped out.Stargunner said:

This table does not take into account that the £2600 plus interest can be earning interest for 6 days from the 23/09/26 in another savings account, so the actual difference for opening the account is negligiblerallycurve said:

Thanks for that. I understand now, basically you get 6 extra days at the end when you have the account full and that's what makes the difference!Bobblehat said:

OK ..... I'm glad I kept the rough working out spreadsheet! It would be 6 days BTW, as although I could have shifted the £400 I kept back today, I can't open the new RS until tomorrow at the earliest.rallycurve said:Bobblehat said:

A good point .... but .....Stargunner said:

Why don't you open the new RS now, so that you can be earning interest on your first deposit of £200.Bobblehat said:

I'll risk it! The NW agent I spoke to insisted on looking up the rate of the current offering when I mentioned about opening a new one later in the month (I already knew the rate). His wording was slightly worrying ... "It's still 6.5%, at the moment!". I should have asked if there was an expected drop imminent, but knew I would get a non-committal answer.friolento said:

It might not be available any longer on the 29th.Bigwheels1111 said:Bobblehat said:

If it's of interest(!), opened the RS 22/09/2024, funded it 22/09 & 01/10 and then by SO on 01/11 until 01/09/2025, so closing balance was £2693.67.Bigwheels1111 said:Hattie627 said:Nationwide BS Flex Regular Saver

My Issue 3 Flex RS has its maturity date today. Interest has been added (£93.46). I have moved the balance plus interest out. The account is still showing as a Flexible RS which is preventing me opening a new one (now Issue 7). I can't remember what happened last year. Has anyone any recent experience of a Flex RS maturity and can recall when the account changes to an Instant Saver?Did you make an extra £200 payment this month, ie total £2600.I did and only got £93.42.Yes interest, I'm thinking of waiting until the 29th to open a new one so I can fund on the first as well to maxInterest this year. Then open on the 30th next year to do the same. As you need to wait a day to open.

OTOH, there might be a better offer during Savings Week, only available if you haven’t yet got the 6.5% one.

Choices, choises🤔

It's a variable account anyway, so if it did drop between now and the 29th, I'd have probably only lost pennies. I have the choice to go elsewhere if the drop is drastic or NLA ... unlikely.

You previously said that you were leaving £400 in the current account to cover the first 2 payments. How much interest are you earning on the £400?

I could shift it out to Chase Saver and back 7 days later @ 4.65% gaining £0.28p over leaving it where it is (1%)....

or, I could open the NW RS tomorrow and lose £2.56 over opening it on 29/09, (£94.10 maturing 22/09/2026 vs £96.66 maturing 28/09/2026).

So leaving the £400 where it is and not having to shift it around, and opening on 29th I'll have gained £2.56 over opening on 23rd but lost £0.28p for being a tad lazy! Do I loose an MSE point for being a tad lazy?I’d be curious to know the maths behind this. How can you earn £2.56 in 7 days on £200 in an account paying 6.5%?

Here you go ... usual qualifier, if you spot an error, let me know and I'll look and correct as necessary.

And for those who insist on a more accurate table showing payment dates for SO's on Bank working days ....

I have similar tables to above but showing a rate drop to 6.00% on 01/10/2025! Did I here a murmur of "Keep 'em to yourself"?

Hopefully none of us are keeping our funds in a current account at 0% while we're waiting for the end of the month0 -

Updated version:

All hypothetical of course, and assuming interest rates remain unchanged and that the same account is available on maturity.

(P.S. not trying to steal Bobblehat's thunder - you are still the champion spreadsheeter!)4 -

Well, you need to consider where the money would end up for the 6 days after an account opened today matures. Likely the difference will be under a quid. But could be nothing if inflation picks up and interest rates soar.Stargunner said:

I mistakenly missed out the word delaying (edited now), as i meant the difference in delaying opening the account is negligible to opening it now.clairec666 said:

Well, not negligible - about 90p if my calculations are correct, if you're putting the matured funds in an easy-access account at 4%. However if the account is still available to renew at 6.5% on maturity, then any gains in funding on the 29th are wiped out.Stargunner said:

This table does not take into account that the £2600 plus interest can be earning interest for 6 days from the 23/09/26 in another savings account, so the actual difference for opening the account is negligiblerallycurve said:

Thanks for that. I understand now, basically you get 6 extra days at the end when you have the account full and that's what makes the difference!Bobblehat said:

OK ..... I'm glad I kept the rough working out spreadsheet! It would be 6 days BTW, as although I could have shifted the £400 I kept back today, I can't open the new RS until tomorrow at the earliest.rallycurve said:Bobblehat said:

A good point .... but .....Stargunner said:

Why don't you open the new RS now, so that you can be earning interest on your first deposit of £200.Bobblehat said:

I'll risk it! The NW agent I spoke to insisted on looking up the rate of the current offering when I mentioned about opening a new one later in the month (I already knew the rate). His wording was slightly worrying ... "It's still 6.5%, at the moment!". I should have asked if there was an expected drop imminent, but knew I would get a non-committal answer.friolento said:

It might not be available any longer on the 29th.Bigwheels1111 said:Bobblehat said:

If it's of interest(!), opened the RS 22/09/2024, funded it 22/09 & 01/10 and then by SO on 01/11 until 01/09/2025, so closing balance was £2693.67.Bigwheels1111 said:Hattie627 said:Nationwide BS Flex Regular Saver

My Issue 3 Flex RS has its maturity date today. Interest has been added (£93.46). I have moved the balance plus interest out. The account is still showing as a Flexible RS which is preventing me opening a new one (now Issue 7). I can't remember what happened last year. Has anyone any recent experience of a Flex RS maturity and can recall when the account changes to an Instant Saver?Did you make an extra £200 payment this month, ie total £2600.I did and only got £93.42.Yes interest, I'm thinking of waiting until the 29th to open a new one so I can fund on the first as well to maxInterest this year. Then open on the 30th next year to do the same. As you need to wait a day to open.

OTOH, there might be a better offer during Savings Week, only available if you haven’t yet got the 6.5% one.

Choices, choises🤔

It's a variable account anyway, so if it did drop between now and the 29th, I'd have probably only lost pennies. I have the choice to go elsewhere if the drop is drastic or NLA ... unlikely.

You previously said that you were leaving £400 in the current account to cover the first 2 payments. How much interest are you earning on the £400?

I could shift it out to Chase Saver and back 7 days later @ 4.65% gaining £0.28p over leaving it where it is (1%)....

or, I could open the NW RS tomorrow and lose £2.56 over opening it on 29/09, (£94.10 maturing 22/09/2026 vs £96.66 maturing 28/09/2026).

So leaving the £400 where it is and not having to shift it around, and opening on 29th I'll have gained £2.56 over opening on 23rd but lost £0.28p for being a tad lazy! Do I loose an MSE point for being a tad lazy?I’d be curious to know the maths behind this. How can you earn £2.56 in 7 days on £200 in an account paying 6.5%?

Here you go ... usual qualifier, if you spot an error, let me know and I'll look and correct as necessary.

And for those who insist on a more accurate table showing payment dates for SO's on Bank working days ....

I have similar tables to above but showing a rate drop to 6.00% on 01/10/2025! Did I here a murmur of "Keep 'em to yourself"?

Hopefully none of us are keeping our funds in a current account at 0% while we're waiting for the end of the month0 -

Nothing stopping you nipping over there to enter the comp!ForumUser7 said:

lol, excludes their England based customerssaverkev said:Savings Week

Very disappointing upto now

Here's Progressive's contribution

UK Savings Week 2025 Branch Competition

It’s UK Savings Week! Helping to ease the burden of the dreaded grocery shop bill (leaving you with a little extra in your pocket to save!), we’re offering you the chance to WIN £250 Tesco voucher! Enter by visiting your local Progressive branch for your chance to win. T&Cs apply.

Competition T&Cs 0

0 -

That's the rule I followclairec666 said:I've always been a bit sceptical of the "open at the end of the month" thing, and have generally followed the rule of "open now if you have the money". But now Bobblehat's spreadsheet is making me doubt myself...

It's not worth overthinking these things though - for example when my last Coop RS matured, it took 5 days for my new account to open, so this could tip you over into the next month. Others like Principality are more predictable (if your maturity instructions are accepted, of course...)

If I have £250 in EA earning 5% waiting for a better home - 6.5% is more than 5% so the money go there. I'm not sure how keeping this £250 at 5% for an extra 6 days can deliver a better return. It is unpredictable what this £250 will be doing in few months time (e.g. impact of variable rates), so I tend to move money as soon as there is a better opportunity available.4 -

Would cost so much more to reside in Northern Ireland for a period than it would to just forgo the competition!saverkev said:

Nothing stopping you nipping over there to enter the comp!ForumUser7 said:

lol, excludes their England based customerssaverkev said:Savings Week

Very disappointing upto now

Here's Progressive's contributionUK Savings Week 2025 Branch Competition

It’s UK Savings Week! Helping to ease the burden of the dreaded grocery shop bill (leaving you with a little extra in your pocket to save!), we’re offering you the chance to WIN £250 Tesco voucher! Enter by visiting your local Progressive branch for your chance to win. T&Cs apply.

Competition T&CsIf you want me to definitely see your reply, please tag me @forumuser7 Thank you.

N.B. (Amended from Forum Rules): You must investigate, and check several times, before you make any decisions or take any action based on any information you glean from any of my content, as nothing I post is advice, rather it is personal opinion and is solely for discussion purposes. I research before my posts, and I never intend to share anything that is misleading, misinforming, or out of date, but don't rely on everything you read. Some of the information changes quickly, is my own opinion or may be incorrect. Verify anything you read before acting on it to protect yourself because you are responsible for any action you consequently make... DYOR, YMMV etc.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.6K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.7K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards