We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

UC and if you go over 16k?

Comments

-

That regulation normally applies to money taken from a pension, in defining whether it is a lump sum (capital) or a regular payment (income).Spoonie_Turtle said:The part about income is very reassuring for me, NedS!

As to PIP/DLA/etc., would it fall under this?

"(3) Subject to paragraph (4), any sums that are paid regularly and by reference to a period, for example payments under an annuity, are to be treated as income even if they would, apart from this provision, be regarded as capital or as having a capital element."

[Paragraph (4) referenced deals with capital payable in installments, which does not sound like it applies to normal benefit payments.]

I am a Forum Ambassador and I support the Forum Team on the Benefits & tax credits, Heat pumps and Green & Ethical MoneySaving forums. If you need any help on those boards, do let me know. Please note that Ambassadors are not moderators. Any post you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own & not the official line of Money Saving Expert.1 -

HillStreetBlues said:

Isn't a possible issue is the DWP can claim the income has been spent during the AP, as it's been spent they have taken the income into account but there is no income left to deduct.ADM H1050 states:When income becomes capital

H1050 Income becomes capital if it has not been spent by the end of the assessment period after the

one in which it was received.For the purposes of this case, it is important to remember the fundamental difference between INCOME and CAPITAL.Any income received in the AP, which has been treated as income (either earned income under UC Reg 22; ADM H3) or unearned income (UC Regs 65-66; ADM H5002) cannot then be also treated as capital in the same AP. It's either income or it's capital, but never both at the same time. This is why H1050 specifically refers to the assessment period after the one in which it was received.So you can clearly argue that UC has taken your £4k of income into account as income (either earned income or unearned income) and therefore those amounts cannot also be considered as capital in the same AP. This should allow you to deduct any amounts of income received within the AP from the total monies held on the last day of the AP.

I hope this isn't the case, but I haven't found anything that states a claimant always spends capital first. Logically a person would spend the income first and any monies left over at the end of AP going into a savings accountI don't know, as there is no mention in the legislation other than what I have covered above, and there is no mention in the ADM guidance other than the example in H1050 which does not include the income (in full) in the AP in which it is received. There is no discussion of whether income or capital has been spent, only the total remaining amount in the next AP (once the income has subsequently become capital). Note the example refers to the capital amount on the 6th March (the first day of the AP), but of course we all know that Pearl's capital will change throughout the AP and it is the amount on the last day of the AP that is relevant in calculating their entitlement to UC.So I do not think it is particularly relevant what has been spent during the AP, and whether it is spent from capital or income. The UC Regs and ADM example are clear, the income (in full) is not to be treated as capital in the AP in which it is received. I think arguments otherwise simply obfuscate the issue. If DWP want to argue otherwise at a tribunal, I would ask where is the legislation to support the rabbit hole they are taking us down?My interpretation is that it's simple, it's income, so it's not capital in that AP. There is legislation and ADM guidance to support that position, and anyone on a tribunal can easily understand that argument.

I am a Forum Ambassador and I support the Forum Team on the Benefits & tax credits, Heat pumps and Green & Ethical MoneySaving forums. If you need any help on those boards, do let me know. Please note that Ambassadors are not moderators. Any post you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own & not the official line of Money Saving Expert.0 -

@NedS

https://assets.publishing.service.gov.uk/media/6894a69d3080e72710b2e237/dmg-ch-29.pdf29053 The amount of income is reduced when money is withdrawn from a fund such as a bank account

which includes income and capital. The amount of capital is reduced if there is evidence to show the

money withdrawn is from capital.

There is a reference in the capital guidance, if monies are all in a bank account then it's income that is being spent. The claimant needs proof that is capital that is being spent. The guidance seems to be at odds with DWP current practice.

I've always thought of it as you can spend capital first, as that has been the practice, but a few threads on here has made me look further into it and now unsure.

Good point about PIP, now that has me now wondering about that, is it just capital

Let's Be Careful Out There0 -

HillStreetBlues said:

Good point about PIP, now that has me now wondering about that, is it just capitalI don't know - I doubt anyone has actually ever thought about it, to the point I bet DWP wouldn't even argue otherwise. But I'm rubbish at finding legal precedent / searching tribunal outcomes.It's definitely not earned income.UC Regs state "unearned income" has the meaning in Chapter 3 of Part 6, which is essentially Reg 66. Anything not defined therein is by definition not "unearned income" for UC purposes. PIP/DLA are not there (and neither is UC), so by definition PIP/DLA (and UC) do not fall within the definition of income for UC purposes. So if they are not recognised as income, it's hard to argue in the legal sense that they should not be included (as they are income) in any capital decision. That said, my point above is I wonder if anyone would actually be smart enough to realise and argue that, as it's not unreasonable to assume they may be income (they look like income under any reasonable definition of the term, just they do not meet the UC definition of income).Part of the issue here is that UC has no mechanism other than to deduct pound for pound anything defined as unearned income (student income being the exception to the rule), so if you specifically define PIP as unearned income, you then have to introduce a separate regulation to specifically disregard it, and what's the point of that (in legislative terms), it's just double handling.You note the example in H1050 is very careful to only talk about earned income.I am a Forum Ambassador and I support the Forum Team on the Benefits & tax credits, Heat pumps and Green & Ethical MoneySaving forums. If you need any help on those boards, do let me know. Please note that Ambassadors are not moderators. Any post you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own & not the official line of Money Saving Expert.0 -

HillStreetBlues said:@NedS

https://assets.publishing.service.gov.uk/media/6894a69d3080e72710b2e237/dmg-ch-29.pdf29053 The amount of income is reduced when money is withdrawn from a fund such as a bank account

which includes income and capital. The amount of capital is reduced if there is evidence to show the

money withdrawn is from capital.

There is a reference in the capital guidance, if monies are all in a bank account then it's income that is being spent. The claimant needs proof that is capital that is being spent. The guidance seems to be at odds with DWP current practice.

I've always thought of it as you can spend capital first, as that has been the practice, but a few threads on here has made me look further into it and now unsure.The example in 29053 talks about expenditure for car insurance, which can be thought of as regular expenditure (monthly or annually) and therefore something that would reasonably be met from income. The DM concludes that this is the case, but because the income is insufficient to meet the cost of the car insurance in full, the DM adjudges that the remainder has come from capital.The example is fairly simplistic and I think the interpretation is reasonable.If you want things to be interpreted differently, keep your capital and income in separate accounts, and make payments accordingly, then it will be difficult for DWP to interpret otherwise.I am a Forum Ambassador and I support the Forum Team on the Benefits & tax credits, Heat pumps and Green & Ethical MoneySaving forums. If you need any help on those boards, do let me know. Please note that Ambassadors are not moderators. Any post you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own & not the official line of Money Saving Expert.0 -

How I interpreted the guidance is income needs to be depleted and only then capital is spent if in a mixed account. If in the example "Pearl " had more income, that would have been spent rather than the capital.NedS said:HillStreetBlues said:@NedS

https://assets.publishing.service.gov.uk/media/6894a69d3080e72710b2e237/dmg-ch-29.pdf29053 The amount of income is reduced when money is withdrawn from a fund such as a bank account

which includes income and capital. The amount of capital is reduced if there is evidence to show the

money withdrawn is from capital.

There is a reference in the capital guidance, if monies are all in a bank account then it's income that is being spent. The claimant needs proof that is capital that is being spent. The guidance seems to be at odds with DWP current practice.

I've always thought of it as you can spend capital first, as that has been the practice, but a few threads on here has made me look further into it and now unsure.The example in 29053 talks about expenditure for car insurance, which can be thought of as regular expenditure (monthly or annually) and therefore something that would reasonably be met from income. The DM concludes that this is the case, but because the income is insufficient to meet the cost of the car insurance in full, the DM adjudges that the remainder has come from capital.The example is fairly simplistic and I think the interpretation is reasonable.If you want things to be interpreted differently, keep your capital and income in separate accounts, and make payments accordingly, then it will be difficult for DWP to interpret otherwise.

I certainly would also be arguing that the income needs to be deducted from total amount if it comes to that, but have now started to wonder if that will be a legal arguing backed up with any sort of case law. I'm not sure I know the answer (I thought I did), but trying to look at it from both sides.

It has got me thinking how I do manage my accounts and have a clear dividing line between capital and income, which has never crossed my mind before it cropped up with the threads on here.

Let's Be Careful Out There1 -

If someone happened to be over 55 (soon to be 57) and only had UC income then they could "store" some of their capital as cash in a SIPP (both Hargreaves and AJ Bell and I assume others dont charge any fees for a cash only SIPP) , then for UC purposes it would no longer count as capital. I would argue that the primary reason for using the SIPP would be the almost instant 25% uplift which is better than anything else.

If they were stoozing then they could take a lump sum to pay off the balance within the same AP, as paying off debt is never deprivation of capital (that might take a bit of careful timing, but worst case they apply for the lump sum early and pay of the debt early).

If worried about affecting future pension contributions (MPAA) then they could use the small pots rule 3 times

1 -

I haven't read though the kind replies yet but will do this evening and respond.

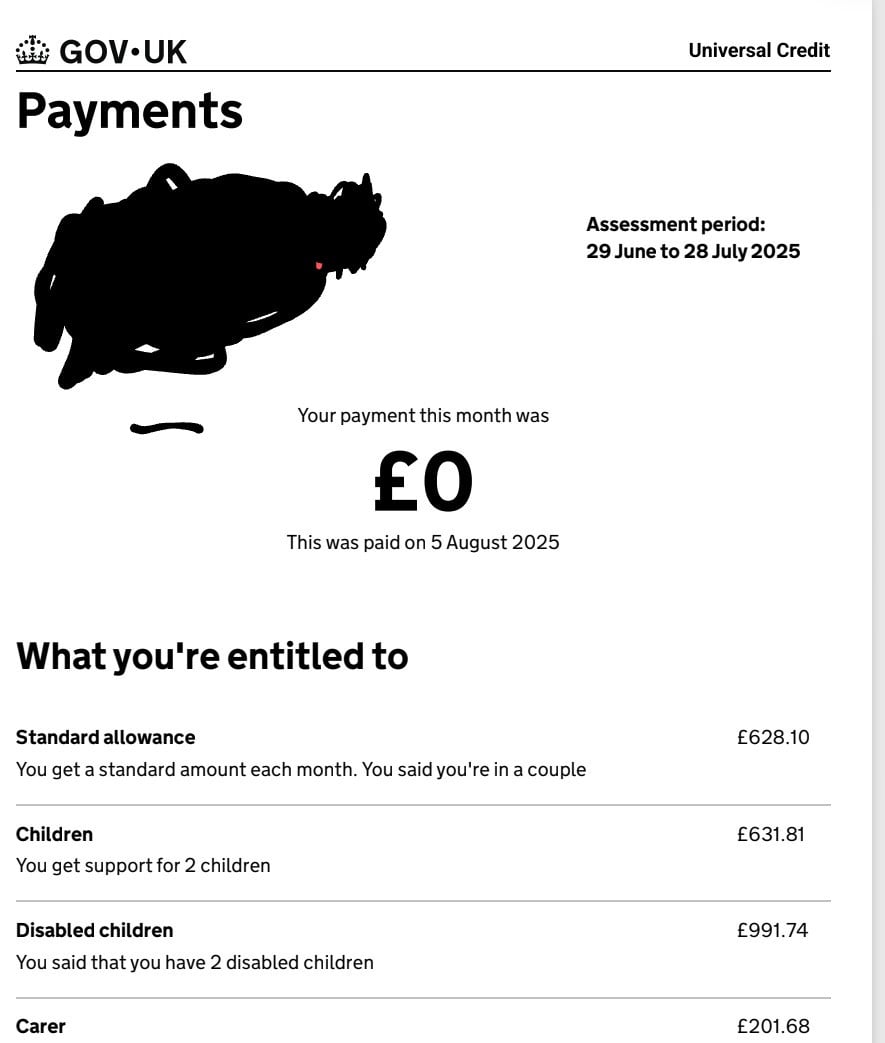

I did get this to wake up to this morning to the attached £0 award which was nice...

Ofcourse they included our children's direct payments SDS (uploaded) and our income both of which should be disregarded we received this month which took us over 16k hence no award. Our savings are really only 6k.

0

0 -

Is it mot true that H1050 covers earned (salary etc) and also unearned income (ie all benefits DLA UC, ESA etc? There's no where that says in legislation that UC is not unearned income I dont think so it should also be considered as income.

Obviously things like gifts are immediately considered as capital and similar things.

Now, sorry dont remember who mentioned if te DWP could argue for example "ohh but you have spent £300 for your £1,000 monthly wage that you received in that AP before the end of the AP so you cant now ask for that £1,000 to be disregarded as capital, only £700".....

That like someone mentioned would be an absolute rabbit hole and makes a great point below.....

"So I do not think it is particularly relevant what has been spent during the AP, and whether it is spent from capital or income. The UC Regs and ADM example are clear, the income (in full) is not to be treated as capital in the AP in which it is received. I think arguments otherwise simply obfuscate the issue. If DWP want to argue otherwise at a tribunal, I would ask where is the legislation to support the rabbit hole they are taking us down? "

So in my situation it looks like each month they will continue to tell me to declare all our monies we have access too, our payment is given a £0 award, I wait for a DM to correct it, each month a different DM comes up with a different random amount under 16k without explaining how they came to that or as I do worry they will come up with something over 16k and we have to go though a mandatory reconsideration and if unsuccessful then a tribunal.

So this is what we have to go through every month.

I did request a MR on the first month as the DM got the capital far off what it should have been but still under 16k thankfully, I only requested a MR so I could see how he worked it out for our reference and to share on here as think it will be very interesting to see what he disregarded and what he didn't and the reasons why.

We are still waiting on the MR from our AP in May, still waiting for the DM to calculate our Capital for our June AP as our UC is on hold until then. So am awaiting 2 outcomes here.

Yes the job centre staff just see what's in your bank account and say "that's your capital". That's what happened to me yesterday at the JC.1 -

Just got an update today.

What are others thoughts on this if you dont mind please? I've uploaded the documents they ask for already.

'I'm currently reviewing your mandatory reconsideration.Whilst you have provided some evidence, there are no bank statements provided to show the earnings or benefits were no longer being in the account at the end of the assessment period.Given this, I would require evidence supporting the earnings and benefits used within the assessment period, to disregard them.As you have stated earnings are to be disregarded if they are no longer held within the account at the end of the assessment period.ESA benefits themselves are not considered capital. However, unspent ESA payments at the end of a payment period are treated as capital,Disability Living Allowance (DLA) is generally disregarded as income, but if not spent within the period it's paid, it can be considered capital.any remaining of your daughters would be disregarded however, any remaining DLA for yourself at the end of the assessment period would be considered capital.A full bank statement covering the 29 June till 31st July would be required with any outgoings marked, so that a correct review can be completed.I have set a document upload for the evidence to be provided and can allow until 14 September 2025, for this action to be complete.After that the decision will be made on the evidence held."0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards