We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

PLEASE READ BEFORE POSTING: Hello Forumites! In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non-MoneySaving matters are not permitted per the Forum rules. While we understand that mentioning house prices may sometimes be relevant to a user's specific MoneySaving situation, we ask that you please avoid veering into broad, general debates about the market, the economy and politics, as these can unfortunately lead to abusive or hateful behaviour. Threads that are found to have derailed into wider discussions may be removed. Users who repeatedly disregard this may have their Forum account banned. Please also avoid posting personally identifiable information, including links to your own online property listing which may reveal your address. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Offer under asking price

Comments

-

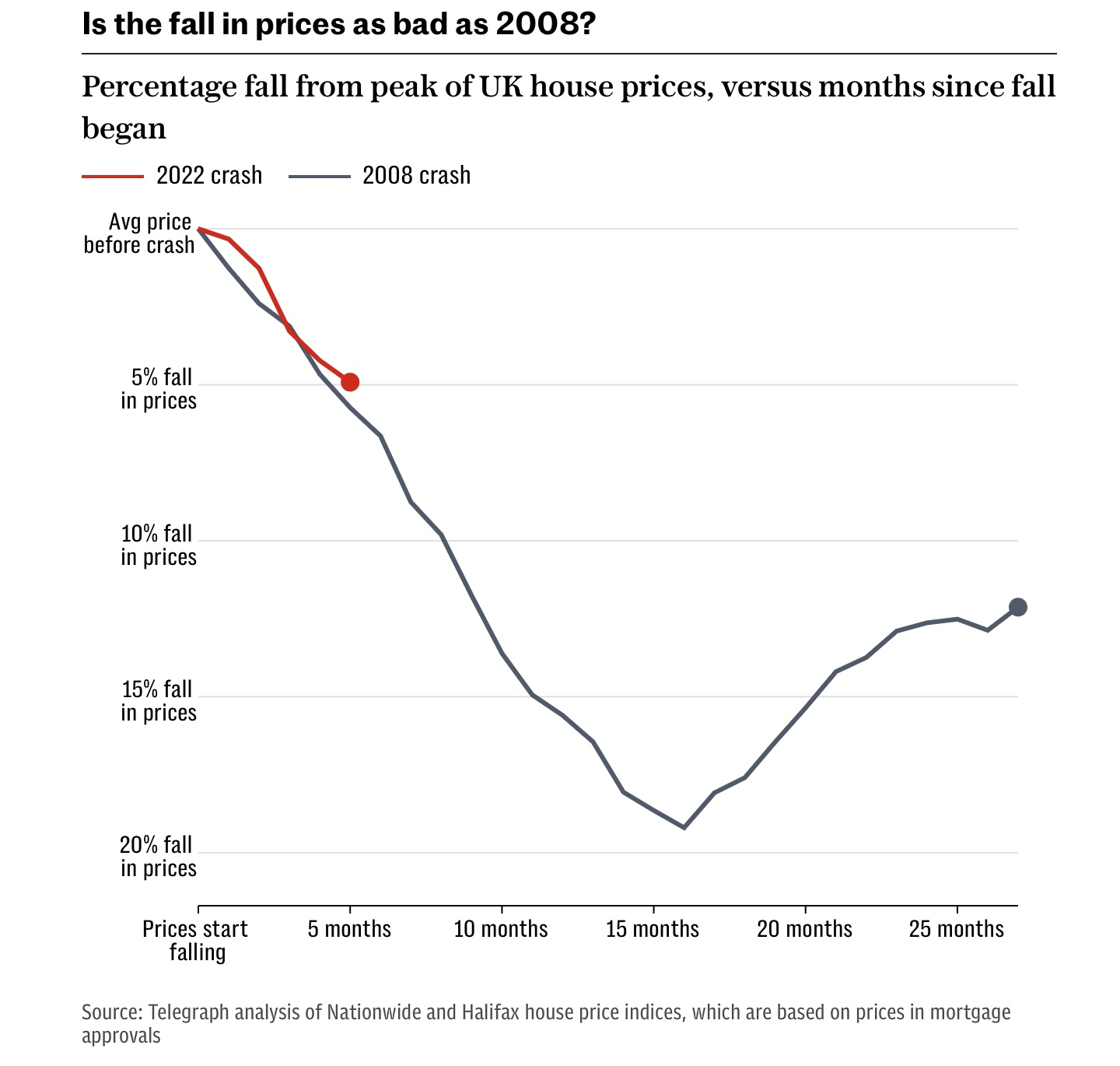

Daily Telegraph have a tracker.arthurdick said:TonyTeacake said:

That's funny as I was listening to LBC radio last week and they where inadated with calls from people whose mortgages where up for renewal and they couldn't afford the new rates. This is what happens when people overpay for houses and interest rates go up.

Oh and I nearly forgot to mention we have rampant inflation which we didn't have 2 years ago.

Not sure how old you are but the previous crashes took at least 2 years or more before we seen the bottom of the market. This crash will be between 20-50% depending on where you live.I am old enough to remember the last crash, I wasn't looking to sell or buy at the time, had a house with a tiny £21000 mortgage on it, so really didn't pay attention to it. I am also old enough to remember interest rates at 15%, great times for me, I had £60000 in the Chelsea building society in Lewisham for a year at least and when I took in my passbook to be updated, I had a nice £9000 given to me, which more than made up for the higher mortgage payments.Could you please tell me more about this crash please, I am inbetween properties at the moment and the areas I am struggling to buy in are around Blackheath and Greenwich, will these be any of the areas getting this big crash, I hope so, I will hang on for a little bit until you give me the heads up, cheers.

https://www.telegraph.co.uk/money/house-prices-data-tool-forecast-interest-rates-markets/

3 -

A lot of the issues can be related back to short sighted ( isn't hindsight great) policy decisions from politicians with vested interests in cutting social housing stock (selling off the family silver and it still goes on) keeping interest rates deliberately low, introducing a number of policies that were "designed to assist people to get on the housing ladder" amongst other policies that have only contributed to massively driving up housing costs to the point where many single buyers cannot afford to purchase and those that can are tied into mortgage terms of 30+ years.MobileSaver said:

Agreed but a lot of those costs are short-sighted policy changes (stamp duty, mortgage interest relief and more onerous tenancy laws) from the government, the underlying fundamentals were fine until then even with interest rate increases.[Deleted User] said:

If you look at what is actually happening, a lot of former BTL landlords are selling up because costs are outstripping their ability to force rent increases.MobileSaver said:

The "cost of living crisis" has been going on for well over a year yet on average 100,000 properties are still being bought and sold every single month in the UK... remind me again which one of us is so out of touch with the real world?TonyTeacake said:

OMG you are so out of touch with the real world. Plenty of wealth where I live in Cheshire but this doesn't reflect the rest of the UK.MobileSaver said:TonyTeacake said:

Factor in the cost of living crisis with all the lay offs happening I think you know which way the market is heading.MobileSaver said:

Er, maybe that's because they can?TonyTeacake said:

I totally agree we are in a totally different market now but unfortunately, there are many sellers who still think they can achieve last year's prices.Sarah1Mitty2 said:

Last year is a very different market, PropertyLog is full of 100k reductions, and not on million pound houses either, most people don`t know how to price correctly in my opinion.mi-key said:

I wonder whyReadyto said:Last year I offered 100k below asking price and sadly I lost on that house Well unless you are talking about something in the millions !

Well unless you are talking about something in the millions ! A friend of mine put their house on the market almost a year ago and just completed last week at the same full asking price...

A friend of mine put their house on the market almost a year ago and just completed last week at the same full asking price... ")

A typical FTB will have at least a 15% deposit and can currently get a 5 year fix at 4.2%, most of us here who have had mortgages will think that's a pretty good deal!TonyTeacake said:Some of the commentators on MSE have said you can get a mortgage rate of under 4%, but fail to mention you will only get this rate with a 33% deposit, this means most FTB are priced out of the marketThe cost of living crisis is massively ever-egged in the context of the housing market; the people affected the most were never going to be in a position to buy a house anyway.Obviously this is anecdotal but we've been out for lunch a few times in the last fortnight and the restaurants were literally packed. We also went out for dinner one night last mid-week and while not packed the pub restaurant was very busy which I thought was impressive when food and drink for two came to £95.Similarly a couple of weeks ago we shopped and had lunch in Merthyr Tydfil (hardly renowned for being a prosperous and vibrant Welsh town) and everywhere was teeming with people - I know it doesn't fit your utopia of doom and gloom leading to a house price crash but the fact of the matter is that a lot of people out there have a lot of spare cash and they don't mind spending it...

How wrong you are. I've no plans to buy or sell property any time soon, it makes no difference to me whether prices rise or fall.TonyTeacake said:It seems to me you can't stand the fact house prices are falling.[Deleted User] said:It's kind of a good thing and we definitely needed to make BTL much less attractive, but this isn't the best way of achieving that.People wanting to rent are already struggling, there are constant threads here bemoaning the lack of availability, higher rents and excessive hurdles before being accepted for a new tenancy.Unless there was a public housing alternative already in place (which there isn't) then why would you want to make the private sector even more unattractive? Or do you not care about renters suffering even more if it means you can buy your next house a little cheaper?

Yes you can argue this will all inflate away but in the same way that the universe is expanding, how realistic is it that people will actually be able to hold their position on the much lauded property ladder, never mind progress upwards?Your life is too short to be unhappy 5 days a week in exchange for 2 days of freedom!0 -

Only part of the picture though as the legend demonstrates. Perhaps my area is peculiar in that when selling recently, two thirds of our viewers were cash buyers. We sold to a cash buyer and made our onward purchase without a mortgage. To be fair i was somewhat surprised at how many cash buyers there were.Aberdeenangarse said:

Daily Telegraph have a tracker.

https://www.telegraph.co.uk/money/house-prices-data-tool-forecast-interest-rates-markets/1 -

BikingBud said:

A lot of the issues can be related back to short sighted ( isn't hindsight great) ... many single buyers cannot afford to purchase and those that can are tied into mortgage terms of 30+ years.MobileSaver said:

Agreed but a lot of those costs are short-sighted policy changes (stamp duty, mortgage interest relief and more onerous tenancy laws) from the government, the underlying fundamentals were fine until then even with interest rate increases.[Deleted User] said:

If you look at what is actually happening, a lot of former BTL landlords are selling up because costs are outstripping their ability to force rent increases.MobileSaver said:

The "cost of living crisis" has been going on for well over a year yet on average 100,000 properties are still being bought and sold every single month in the UK... remind me again which one of us is so out of touch with the real world?TonyTeacake said:

OMG you are so out of touch with the real world. Plenty of wealth where I live in Cheshire but this doesn't reflect the rest of the UK.MobileSaver said:TonyTeacake said:

Factor in the cost of living crisis with all the lay offs happening I think you know which way the market is heading.MobileSaver said:

Er, maybe that's because they can?TonyTeacake said:

I totally agree we are in a totally different market now but unfortunately, there are many sellers who still think they can achieve last year's prices.Sarah1Mitty2 said:

Last year is a very different market, PropertyLog is full of 100k reductions, and not on million pound houses either, most people don`t know how to price correctly in my opinion.mi-key said:

I wonder whyReadyto said:Last year I offered 100k below asking price and sadly I lost on that house Well unless you are talking about something in the millions ! A friend of mine put their house on the market almost a year ago and just completed last week at the same full asking price...

A typical FTB will have at least a 15% deposit and can currently get a 5 year fix at 4.2%, most of us here who have had mortgages will think that's a pretty good deal!TonyTeacake said:Some of the commentators on MSE have said you can get a mortgage rate of under 4%, but fail to mention you will only get this rate with a 33% deposit, this means most FTB are priced out of the marketThe cost of living crisis is massively ever-egged in the context of the housing market; the people affected the most were never going to be in a position to buy a house anyway.Obviously this is anecdotal but we've been out for lunch a few times in the last fortnight and the restaurants were literally packed. We also went out for dinner one night last mid-week and while not packed the pub restaurant was very busy which I thought was impressive when food and drink for two came to £95.Similarly a couple of weeks ago we shopped and had lunch in Merthyr Tydfil (hardly renowned for being a prosperous and vibrant Welsh town) and everywhere was teeming with people - I know it doesn't fit your utopia of doom and gloom leading to a house price crash but the fact of the matter is that a lot of people out there have a lot of spare cash and they don't mind spending it...

How wrong you are. I've no plans to buy or sell property any time soon, it makes no difference to me whether prices rise or fall.TonyTeacake said:It seems to me you can't stand the fact house prices are falling.[Deleted User] said:It's kind of a good thing and we definitely needed to make BTL much less attractive, but this isn't the best way of achieving that.People wanting to rent are already struggling, there are constant threads here bemoaning the lack of availability, higher rents and excessive hurdles before being accepted for a new tenancy.Unless there was a public housing alternative already in place (which there isn't) then why would you want to make the private sector even more unattractive? Or do you not care about renters suffering even more if it means you can buy your next house a little cheaper?I don't think many people need hindsight to realise that making BTL less attractive leads to a world of pain for the millions of renters in the UK!Similarly I don't think you need to be a genius to understand that buying something as a singleton rather than as a couple is going to be much more expensive, sometimes to the point of being unaffordable.BikingBud said:how realistic is it that people will actually be able to hold their position on the much lauded property ladder, never mind progress upwards?Yet well over a million people in the UK do exactly that year after year after year...Every generation blames the one before...

Mike + The Mechanics - The Living Years0 -

There are some down the road from there for £500k. They are priced to discourage ownership, they want you to buy a £125k stake and pay rent on the rest. It's a scam, but almost all the new builds around here are doing it now. They all want rental income and service charges.mi-key said:

How much are comparable new builds in the area though?[Deleted User] said:Just looking locally, there are some houses that were new build 10 years ago. £200k initial sale, now on for £300k. No way wages have kept up with that.0 -

So unlike a lamb steak that is a luxury you can live without, everyone needs a roof over their head. Due to human biology they need to have children when they are young too. There is a limit to how cheap they can go, especially as FTBs who are stretched to the limit then won't have the money to fix up a complete wreck.MobileSaver said:[Deleted User] said:Just looking locally, there are some houses that were new build 10 years ago. £200k initial sale, now on for £300k. No way wages have kept up with that.I'm sure you're right but so what? Indeed I'm sure wages haven't kept up with lots of things in recent times but it is what it is.If lamb steaks are too expensive at Tesco then you can either- Buy a cheaper product, or

- Compromise financially elsewhere so you can afford what you want, or

- Refuse to buy until the the price comes back down and go without in the meantime

The fact is that buying a suitable home has got much, much harder over the years. All these people saying they bought a £60k house when interest rates were much higher are not appreciating that things today are much harder than they were then, despite the lower interest rate.

Here's another interesting stat. Back in 2021 the average help FTBs got from parents was £32k. Everyone I still know from school who bought a house did so only after inheriting a big deposit, although admittedly it's not that many people and anecdotes are not data. How much help did FTBs get from their parents and inheritance back in the 80s?

It's a vicious circle because as property prices go up, the amount people inherit increases too, so they can afford to pay more for property. The price keeps going up, and people without money to inherit get left behind.0 - Buy a cheaper product, or

-

Aberdeenangarse said:

Daily Telegraph have a tracker.arthurdick said:TonyTeacake said:

That's funny as I was listening to LBC radio last week and they where inadated with calls from people whose mortgages where up for renewal and they couldn't afford the new rates. This is what happens when people overpay for houses and interest rates go up.

Oh and I nearly forgot to mention we have rampant inflation which we didn't have 2 years ago.

Not sure how old you are but the previous crashes took at least 2 years or more before we seen the bottom of the market. This crash will be between 20-50% depending on where you live.I am old enough to remember the last crash, I wasn't looking to sell or buy at the time, had a house with a tiny £21000 mortgage on it, so really didn't pay attention to it. I am also old enough to remember interest rates at 15%, great times for me, I had £60000 in the Chelsea building society in Lewisham for a year at least and when I took in my passbook to be updated, I had a nice £9000 given to me, which more than made up for the higher mortgage payments.Could you please tell me more about this crash please, I am inbetween properties at the moment and the areas I am struggling to buy in are around Blackheath and Greenwich, will these be any of the areas getting this big crash, I hope so, I will hang on for a little bit until you give me the heads up, cheers.

https://www.telegraph.co.uk/money/house-prices-data-tool-forecast-interest-rates-markets/

This graph is even more interesting:

People were buying with very small deposits. Then suddenly they were locked out of the market if they couldn't put down a much more substantial deposit.

The gap between asking and completion prices is massive too.

0 -

Looking at some of the replies I would like to apologize if I kept anyone from sleeping last night.

Here are the hard facts.

1. Help to buy finished in Oct 2022.

2. Interest rates have more than doubled in the last 12 months and will need to go higher to fight this inflation monster.

3. Money printers are turned off.

4. Layoffs have started and unfortunately will get a lot worse.

5. Inflation is still high at 10.1% and will not be coming down anytime soon (We all know it is well over 20%).

6. Wages are not keeping up with inflation.

7. House sales for January 2023 are 11% down on 2019's levels & 27% lower than December 2022.

8. UK property asking prices show the weakest February gain on record: Rightmove

9. Land registry sold prices in Fulham are down 11.6% in the past 3 months (October 3.2%, November 5.1%, December (3.3%). Just because folks don't see reductions in their area yet doesn't mean it isn't coming and I am not blind to think this reflects everywhere in the UK. Some sellers are starting to reduce the asking price by huge amounts

9. I could go on and on but I don't have the time.

I'm afraid far too many people live in an economic fantasy world and try to pretend it will just go away. Interest rate hikes were always going to be damaging for many people and I am not just talking about mortgages, we have credit cards, car loans, bank loans, etc.

Everything I said in my posts early last year has happened.

Let us see where we are at Christmas as I would love to hear the excuses from certain commentators on here with a vested interest, please don't disappear on me.

1 -

Erm. So far nothing that you said early last year has happened!TonyTeacake said:Looking at some of the replies I would like to apologize if I kept anyone from sleeping last night.

Here are the hard facts.

1. Help to buy finished in Oct 2022.

2. Interest rates have more than doubled in the last 12 months and will need to go higher to fight this inflation monster.

3. Money printers are turned off.

4. Layoffs have started and unfortunately will get a lot worse.

5. Inflation is still high at 10.1% and will not be coming down anytime soon (We all know it is well over 20%).

6. Wages are not keeping up with inflation.

7. House sales for January 2023 are 11% down on 2019's levels & 27% lower than December 2022.

8. UK property asking prices show the weakest February gain on record: Rightmove

9. Land registry sold prices in Fulham are down 11.6% in the past 3 months (October 3.2%, November 5.1%, December (3.3%). Just because folks don't see reductions in their area yet doesn't mean it isn't coming and I am not blind to think this reflects everywhere in the UK. Some sellers are starting to reduce the asking price by huge amounts

9. I could go on and on but I don't have the time.

I'm afraid far too many people live in an economic fantasy world and try to pretend it will just go away. Interest rate hikes were always going to be damaging for many people and I am not just talking about mortgages, we have credit cards, car loans, bank loans, etc.

Everything I said in my posts early last year has happened.

Let us see where we are at Christmas as I would love to hear the excuses from certain commentators on here with a vested interest, please don't disappear on me.

Inflation will come down substantially in April once energy prices have been factored into the 12 month period and falling fuel prices start to come into account. This is a given.

Interest rates are unlikely to go much, if any higher than they currently are. Forecasts are for them to peak this summer before starting to fall back again. Mortgage interest rates are already falling with the best 5 year deals now in the 3.7% range.

My wages increased 11.1% last year. So far this year we have had a 3.5% increase in January, are due another 3.5% in July + performance based increase and will then receive a further inflation based rise in December. This is not uncommon in the industry. My other half has also received inflation based wage increases in a completely different sector. It may be that public sector pay isn't keeping up with inflation but then that is almost always the case and people know that when they take employment in that sector.

House sales being down 11% on January 2019 is hardly surprising. In 2019 we completed on a sale in 3.5 weeks. Since Covid you just can not get those timescales. A simple sale now takes at least 12 weeks and is often 16 or more.

Asking price data is pretty much useless. Anyone can market their property at whatever price they like. We need to be looking at sales price data.

Land Registry sales prices being down in one specific area could be down to any number of factors not least the types of property that have sold. If the previous year was made up of mainly detached property sales and the next year is mainly terraced house or flat sales then yes it will show a drop. But that number needs to be taken in context not just assuming that prices have fallen by 11% across the board as you seem to be assuming.1 -

A lot of nonsense and opinion in your hard "facts".TonyTeacake said:Looking at some of the replies I would like to apologize if I kept anyone from sleeping last night.

Here are the hard facts.

1. Help to buy finished in Oct 2022.

2. Interest rates have more than doubled in the last 12 months and will need to go higher to fight this inflation monster.

3. Money printers are turned off.

4. Layoffs have started and unfortunately will get a lot worse.

5. Inflation is still high at 10.1% and will not be coming down anytime soon (We all know it is well over 20%).

6. Wages are not keeping up with inflation.

7. House sales for January 2023 are 11% down on 2019's levels & 27% lower than December 2022.

8. UK property asking prices show the weakest February gain on record: Rightmove

9. Land registry sold prices in Fulham are down 11.6% in the past 3 months (October 3.2%, November 5.1%, December (3.3%). Just because folks don't see reductions in their area yet doesn't mean it isn't coming and I am not blind to think this reflects everywhere in the UK. Some sellers are starting to reduce the asking price by huge amounts

9. I could go on and on but I don't have the time.

I'm afraid far too many people live in an economic fantasy world and try to pretend it will just go away. Interest rate hikes were always going to be damaging for many people and I am not just talking about mortgages, we have credit cards, car loans, bank loans, etc.

Everything I said in my posts early last year has happened.

Let us see where we are at Christmas as I would love to hear the excuses from certain commentators on here with a vested interest, please don't disappear on me.

2. Most industry expectations are that interest rate rises have almost peaked and are likely to start falling from early next year

4. Based on what exactly?

5. Industry expectations are that inflation will be down to 2-4% by the end of the year

7. Seasonally adjusted sales volumes show a drop of about 3% from December 2022 and less than 1.5% down on the average for 2019. January sales figures are always low so comparing the unadjusted figures is misleading

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604.1K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards