We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

GMP equalisation workings - Barclays pension

Comments

-

By the way, on the subject of claiming back the over-payment of tax on the GMP equalisation payment, having submitted my claim, and being told I would receive a “decision” by around the beginning of August, I decided to give them a ring today when I didn’t hear anything.

Apparently my case had been inadvertently allocated to the wrong queue and marked as case closed (with no action taken) on the 18th July.

I was then promised that my letter had now been allocated to the right place and that I could hope to receive a decision in 2-4 weeks.

I would also mention that, last week I received a phishing scam text message regarding my “HMRC tax refund claim, and could I click on this secure link to update my details.”1 -

This was my latest question to WTW as the previous reply stated they could not provide figures for the calculation at 65 until nearer the date.

I was asking about the GMP calculation at 60 on the alternative basis (female) not at 65.I have now attached a spreadsheet which shows the methodology that WTW agreed in 2018 was correct. Next to that is a column for what I think should have happened at 60 for equalisation .Can you confirm the figures and methodology relating to GMP equalisation.Many thanks

The reply to this was a copy of the original letter setting out the actual amount paid and ‘new’ figure plus the tax implications etc etc.

I am going to ask for the figures of accumulated pension and GMP in the ‘Barber period’.

I assume I am allowed these? Then I’ll work through the example on P10 of the leaving book.

If the methodology for franking has changed since 2018 I need to know to plan so I think it is reasonable to continue to pursue the finer details.0 -

Firstly, my feeling was that’s it’s straightforward to reconstruct one’s accumulated pension (GMP + Excess) from the original data; including one’s GMP at leaving COE. The components of the relevant progression of this accumulation can then be extracted to verify the WTW Equalisation chart. Something I’ve already done, as I mentioned.DT2001 said:This was my latest question to WTW as the previous reply stated they could not provide figures for the calculation at 65 until nearer the date.

I was asking about the GMP calculation at 60 on the alternative basis (female) not at 65.I have now attached a spreadsheet which shows the methodology that WTW agreed in 2018 was correct. Next to that is a column for what I think should have happened at 60 for equalisation .Can you confirm the figures and methodology relating to GMP equalisation.Many thanks

The reply to this was a copy of the original letter setting out the actual amount paid and ‘new’ figure plus the tax implications etc etc.

I am going to ask for the figures of accumulated pension and GMP in the ‘Barber period’.

I assume I am allowed these? Then I’ll work through the example on P10 of the leaving book.

If the methodology for franking has changed since 2018 I need to know to plan so I think it is reasonable to continue to pursue the finer details.

To my mind, as I also mentioned, the difficulty (not impossibility, if one has kept old PAYE data) lies in verifying the aforementioned starting GMP figures; since these form the basis of a large proportion of one’s pension.

Secondly, like you, I spent many years curiously waiting to see if the figures agreed with WTW would actually appear in my payslip at age 65.

Thankfully they did!0 -

Secondly, like you, I spent many years curiously waiting to see if the figures agreed with WTW would actually appear in my payslip at age 65.Thankfully they did!

Proverbs 23:18 1

1 -

Personally I think the GMP/Excess calculation is going to be there or thereabouts. The reason I would like their figures is then to be able to create a table for the alternative at 60 to try, yet again, to confirm the process at 65. At the moment I cannot see why the excess reduces by so much - it should reduce, but only by the increases from ERD and the original GMP figure.

If you look at Mike’s figures on P1 of this thread I think they back up that process. My excess drops by £2.5k so how does this figure come about?0 -

Firstly, I’m not really clear about this. When you say your “excess drops by £2,500”, when does this happen and where are the figures you’re quoting coming from? Not the equalisation chart presumably.DT2001 said:

...At the moment I cannot see why the excess reduces by so much - it should reduce, but only by the increases from ERD and the original GMP figure.

If you look at Mike’s figures on P1 of this thread I think they back up that process. My excess drops by £2.5k so how does this figure come about?

Also, do you know how much your excess actually (will have) increased between ERD and GMP?

Secondly, you mention the Franking of Excess from GMP date back down to ERD date.

For the purposes of comparing the calculation of my figures with yours, it’s probably worth bearing in mind that this aspect is different from me in two slightly different respects:

1. I took a NRA (NRD) pension whereas you took an ERD pension. As previously discussed they are calculated very differently.

2. My pension got a “GMP step-up” at age 65 with my excess being Franked back to NRA (60). Your pension INCLUDED your assumed GMP step-up (less actuarial adjustment) from ERD; subject to a possible minor adjustment at GMP age reflecting “actual against assumption”.

I assume that the pension you were offered also reflected the aforementioned Franking that “normally” takes place at GMP age.

0 -

MikeFloutier said:

Firstly, I’m not really clear about this. When you say your “excess drops by £2,500”, when does this happen and where are the figures you’re quoting coming from? Not the equalisation chart presumably.DT2001 said:

...At the moment I cannot see why the excess reduces by so much - it should reduce, but only by the increases from ERD and the original GMP figure.

If you look at Mike’s figures on P1 of this thread I think they back up that process. My excess drops by £2.5k so how does this figure come about?

Also, do you know how much your excess actually (will have) increased between ERD and GMP?

Secondly, you mention the Franking of Excess from GMP date back down to ERD date.

For the purposes of comparing the calculation of my figures with yours, it’s probably worth bearing in mind that this aspect is different from me in two slightly different respects:

1. I took a NRA (NRD) pension whereas you took an ERD pension. As previously discussed they are calculated very differently.

2. My pension got a “GMP step-up” at age 65 with my excess being Franked back to NRA (60). Your pension INCLUDED your assumed GMP step-up (less actuarial adjustment) from ERD; subject to a possible minor adjustment at GMP age reflecting “actual against assumption”.

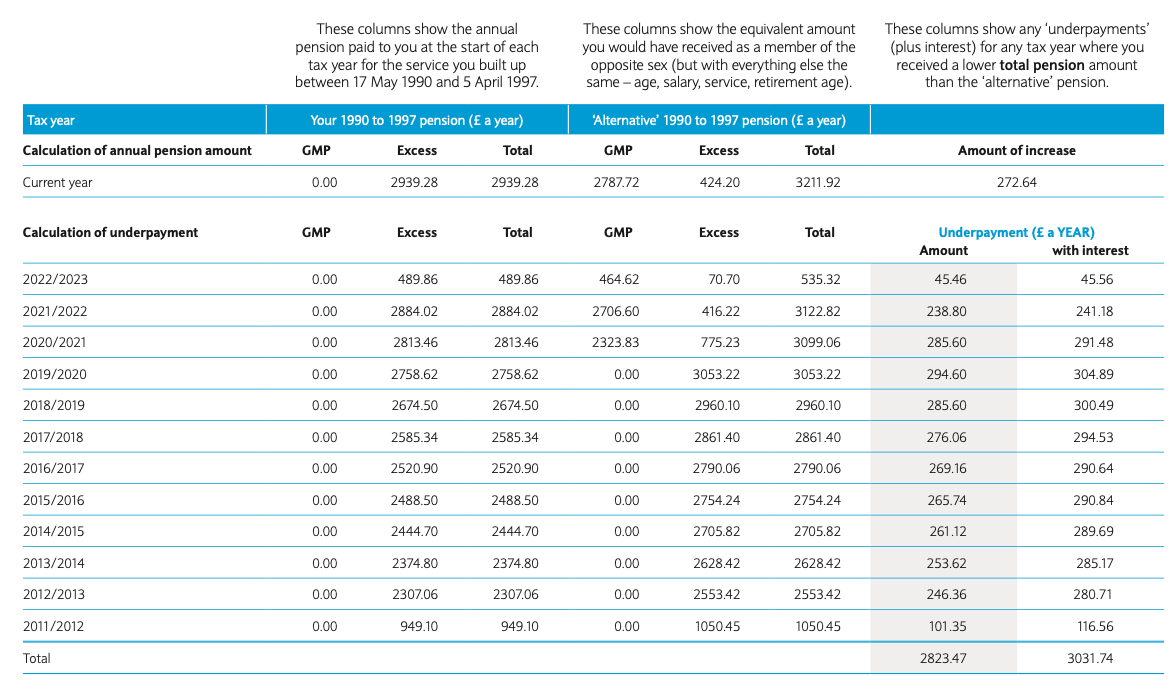

I assume that the pension you were offered also reflected the aforementioned Franking that “normally” takes place at GMP age. The equalisation chart above shows excess on alternative calculation in 2019/20 as £3053.22. In 2020/21 at £775.23 and 2021/22 at £416.22.

The equalisation chart above shows excess on alternative calculation in 2019/20 as £3053.22. In 2020/21 at £775.23 and 2021/22 at £416.22.

At ERD the pension was circa £2500 inc the GMP element (exact figure unknown as drawn part way through tax year).

I am suggesting (using the information provided in 2018 by WTW for my calculation at 65) that the excess of £3053.22 should reduce by say £553 (for the increases since ERD) and another circa £500 for the GMP (original value at date of leaving).

Whilst I follow your point 2 above I think it presumes fully franking my excess which WTW in 2018 confirmed was not the case.What concerns me is that the methodology has changed from 2018 to now. If it is now considered legally correct ‘my calculation’ at 65 will leave me with a pension wholly made up of GMP half of which will not increase at all and about 1/3 rd less than WTW’s confirmed methodology of 2018.1 -

Ok, there seem to be a few issues here:The equalisation chart above shows excess on alternative calculation in 2019/20 as £3053.22. In 2020/21 at £775.23 and 2021/22 at £416.22.

At ERD the pension was circa £2500 inc the GMP element (exact figure unknown as drawn part way through tax year).

I am suggesting (using the information provided in 2018 by WTW for my calculation at 65) that the excess of £3053.22 should reduce by say £553 (for the increases since ERD) and another circa £500 for the GMP (original value at date of leaving).

Whilst I follow your point 2 above I think it presumes fully franking my excess which WTW in 2018 confirmed was not the case.What concerns me is that the methodology has changed from 2018 to now. If it is now considered legally correct ‘my calculation’ at 65 will leave me with a pension wholly made up of GMP half of which will not increase at all and about 1/3 rd less than WTW’s confirmed methodology of 2018.

1. My understanding of the “Excess”, is that it is simply a term used to describe a variable that is derived by subtracting the GMP figure from the Total Pension. I’m not sure it really has a life of its own.

2. I wonder if we need to clarify this term “Full Franking”.

a) My understanding is that (with an ERD pension) Barclays have decided to Frank the Excess (at GMP age) back down to its level at ERD.

b) With a NRA pension (like mine) the Excess is Franked back down from GMP age level to NRA level.

c) To my mind “Full Franking” would calculate the GMP increase from retirement date to GMP age and then Frank the Excess by this amount; unless, by doing so, the total pension was less than the GMP, when the pension would then be set at the level of the GMP at GMP age.

3. Regarding your first para, my understanding is that:

a) Your GMP step up was included in your pension from ERD and therefore no step up is to be expected at GMP age (60 in the case of the Alternate’s figures you quote)

b) The Alternate’s (and by extension your) Total Pension figure is increasing correctly, as you would expect (there being no step up)

c) What is being introduced into the equation here (2020/21) is the newly revalued GMP figure. The “reduction” in the Excess variable is simply a notional artefact of this process of description. It doesn’t mean your pension has been reduced; as the continual increase in the Total Pension figure bears out.

d) The fact that the Excess figure also reduces in 2021/22 is, to my mind, a reflection of the fact that your Alternate’s, and your GMP ages occur in the middle of a tax year and therefore two tax years are affected. But, again, the Total Pension figure is not adversely affected, it continues to rise steadily, if slowly.

4. To my mind, what we want to verify is the extent of the Franking you have suffered. Importantly, in section 2 above, proving that the calculation is as per a) and not c), assuming you agree that a) is correct.0 -

I’m still waiting for my tax refund, will chase them again in a couple of weeks, BUT, whilst browsing the subject, I came across this - https://www.pensionsage.com/pa/further-clarity-given-on-GMP-equalisation-tax-guidance.php?utm_source=jsrecent - which you’ll see included the phrase; “it [HMRC] confirmed that the interest element should be covered by the personal savings allowance”DT2001 said:

It is taxable according to HMRC tax manual Saim9115.MikeFloutier said:I'm still trying to puzzle through this BUT, in the meantime, whilst working out the tax overpayment Barclays have applied to my GMP equalisation payment I started to wonder about the interest element of the payment.

The monthly bank statement entry for our pensions always includes (in the details) our gross pay and our tax code. Having checked, it's clear that the interest isn't included in this figure.

What is not clear, is whether the interest is taxable, AND also, whether it's included in Barclays's tax calculations.

Any ideas?

It does not qualify as tax on savings interest (annual £1k allowance) https://www.gov.uk/apply-tax-free-interest-on-savings

However WTW does include a letter to send to HMRC to give you the option to spread the payment across the tax years that your GMP compensation related to.

I’ll bear this in mind when checking the workings of the refund.0 -

https://www.pensionsage.com/pa/GMP-working-group-publishes-anti-franking-guidance.php

Also, this link appeared in the linked article I mentioned in my previous post. I found it eye-opening to the extent that it mentioned that “Anti-franking sub-group chair and Aon consultant, Felicity Boyce, commented: “Following requests from the industry, we have produced a supplement to the original methodology guidance which examines the interaction of anti-franking and GMP equalisation in more detail.””

Clearly if the Administrators (“the Industry”) are asking for this sort of advice, it behoves us to look carefully at it.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards