We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

GMP equalisation workings - Barclays pension

Comments

-

Thanks Mike and Mavwa

My son has calculated the GMP from the implementation points 60 and 65. He has calculated at 7% compounded increases for 19 and 24 years (not 100% sure if your calc is 19 or 20 for your 60th). Anyway there is circa £55 difference between the two - as expected as a female accrued at a slightly higher rate.

I do not understand two things

Why the excess is so different in the two methods in 2014/15 when it is GMP equalisation. Did the accrual of pension ‘excess’ differ between male and female employees between 1990 and 1997

Why the excess reduces by £600 when you turn 65. I know there was some franking between 60 and 65 but could not see why. Having said that we know your figures for your whole pension at 65 were correct as they have been cross checked. So at a loss.

We await WTW0 -

Just seen this after posting above.MikeFloutier said: STOP CONSIDER THE FOLLOWING BEFORE GOING ON

STOP CONSIDER THE FOLLOWING BEFORE GOING ON

I know that sounds a little dramatic but this has just occurred to me and it’s very straightforward.

Barclays agreed that my pension should receive a (GMP revaluation) step-up at my GMP age of 65. This step-up was over £5,000 pa. (see attached pic for details)

Had I been a woman, my GMP age would have been 60.

You see where I’m going. Should I not have received my step-up at age 60 (under Barber/Lloyds).

So shouldn’t my GMP equalisation payment be 5 x my step-up?

Or am I missing something?

Simple answer is no because your step up would have been lower. Why - your GMP increases had 5 years less to build up and the equalisation only applies to 1990 onwards.0 -

Why the excess reduces by £600 when you turn 65.

Does this have anything to do with the state pension age reduction imposed by the Barclays Scheme?

0 -

Ok, I was about to delete my last post, having read more fully about the Lloyds decisions.DT2001 said:Just seen this after posting above.

Simple answer is no because your step up would have been lower. Why - your GMP increases had 5 years less to build up and the equalisation only applies to 1990 onwards.

Yes, clearly my suggestion was unreasonable but I simply made it to check what looked a reasonable suggestion.

Yes, I wouldn’t have built up so much GMP if my GMP date was on my 60th birthday. In fact the £25,000 I was suggesting will be covered by 10 years’ worth of extra GMP included in my pension. So, ironically I will probably be much better off with a GMP age of 65.

So, I now realise that the figures in WTW’s chart are derived from pension figures drawn from service within the Barber Window only.

They look reasonable to me and I’m guessing they will check out ok when the arithmetic is done.

I'm going to sleep on it and wait to hear WTW’s response

0 -

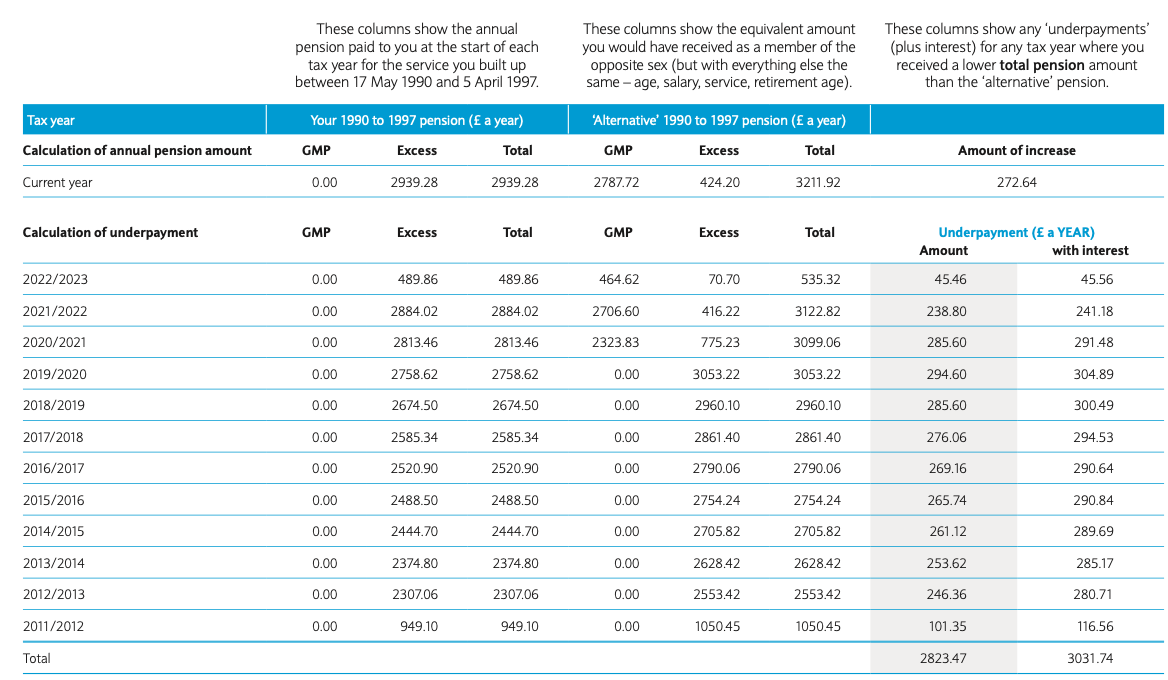

My figures with big reduction at 60 in excess under the alternative scheme.

My figures with big reduction at 60 in excess under the alternative scheme.

1 -

so not sure that can be the case?

Neither am I - it's just that the amount in question is very close to Mike's abatement ( but this could be pure co-incidence).

And yes, Barclays do impose the Abatement which in my case is £672.49 pa.1 -

Yes, Barclays do impose this Abatement, which they refer to as “State Pension Deduction”. In my chart you can see (although for some reason it’s missing from the bottom of DT2001’s) that they mention that figures quoted are before this deduction.xylophone said:so not sure that can be the case?Neither am I - it's just that the amount in question is very close to Mike's abatement ( but this could be pure co-incidence).

And yes, Barclays do impose the Abatement which in my case is £672.49 pa.

Something else I noticed on your chart DT, was in the Alternate (woman) column. You will notice that at “her” GMP date/year (2020/21) there is no GMP step-up.

Naturally your columns don’t show a GMP step-up since you haven’t reached your GMP date yet.

However, it’s possible that a step-up is not to be expected for cases, such as I was offered and declined, where a “taking pension early” option is accepted. I recall that in these cases, the step up (due much later) is added to the immediate, early pension; hence no step-up.

Whether or not this is beneficial depends on how long you live.

I’m not sure which option you selected DT, but if it was for the “early” pension, that would probably explain the lack of a GMP step-up in the Alternate “her” figures.

If, like me, you opted for a Normal Retirement Date pension start, then I’d expect to see a step-up in the “her” figures; which would, I suppose, imply a correspondingly higher lump sum.

As I said this is all supposition, me thinking out loud, but perhaps worth considering.2 -

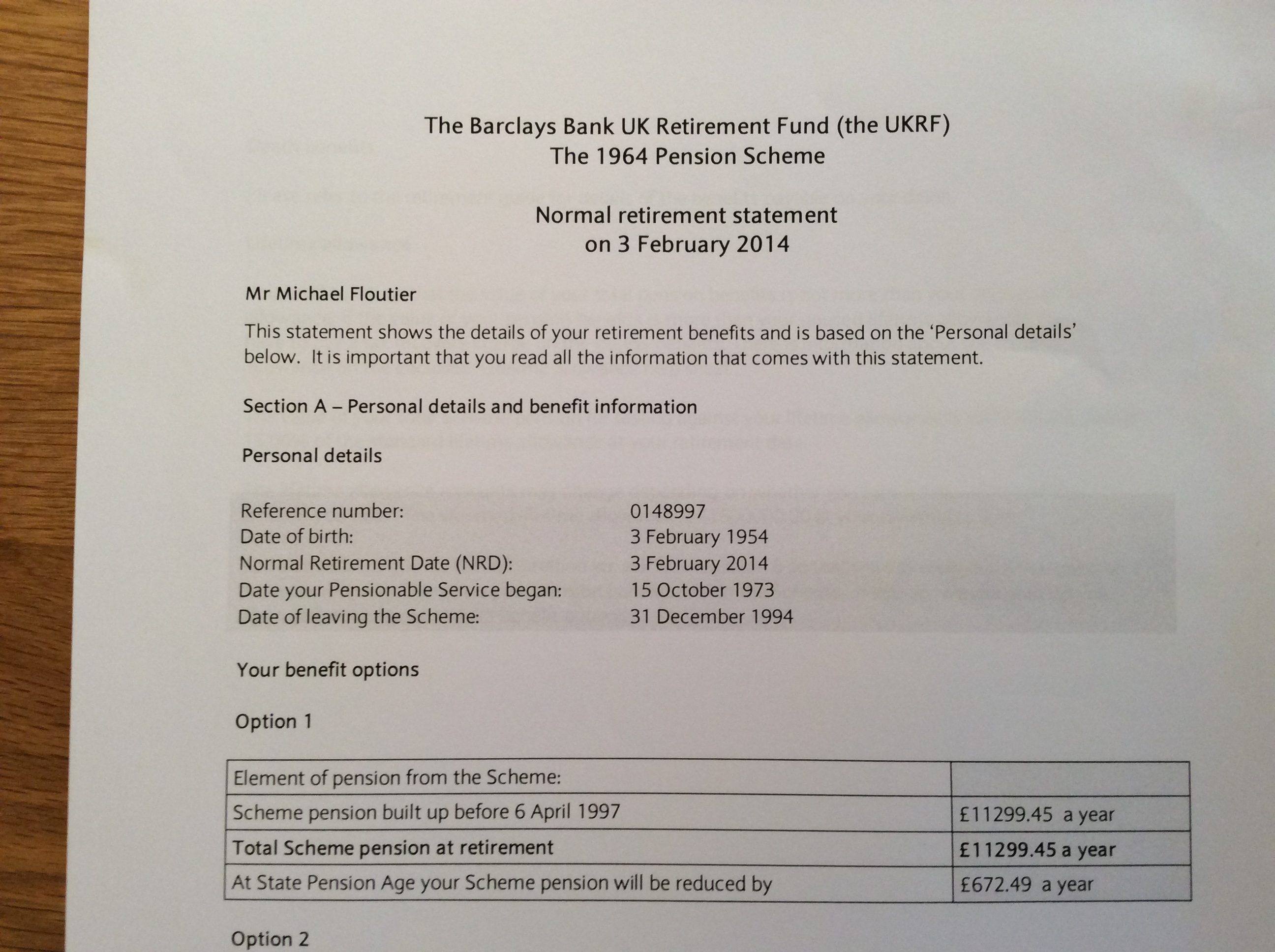

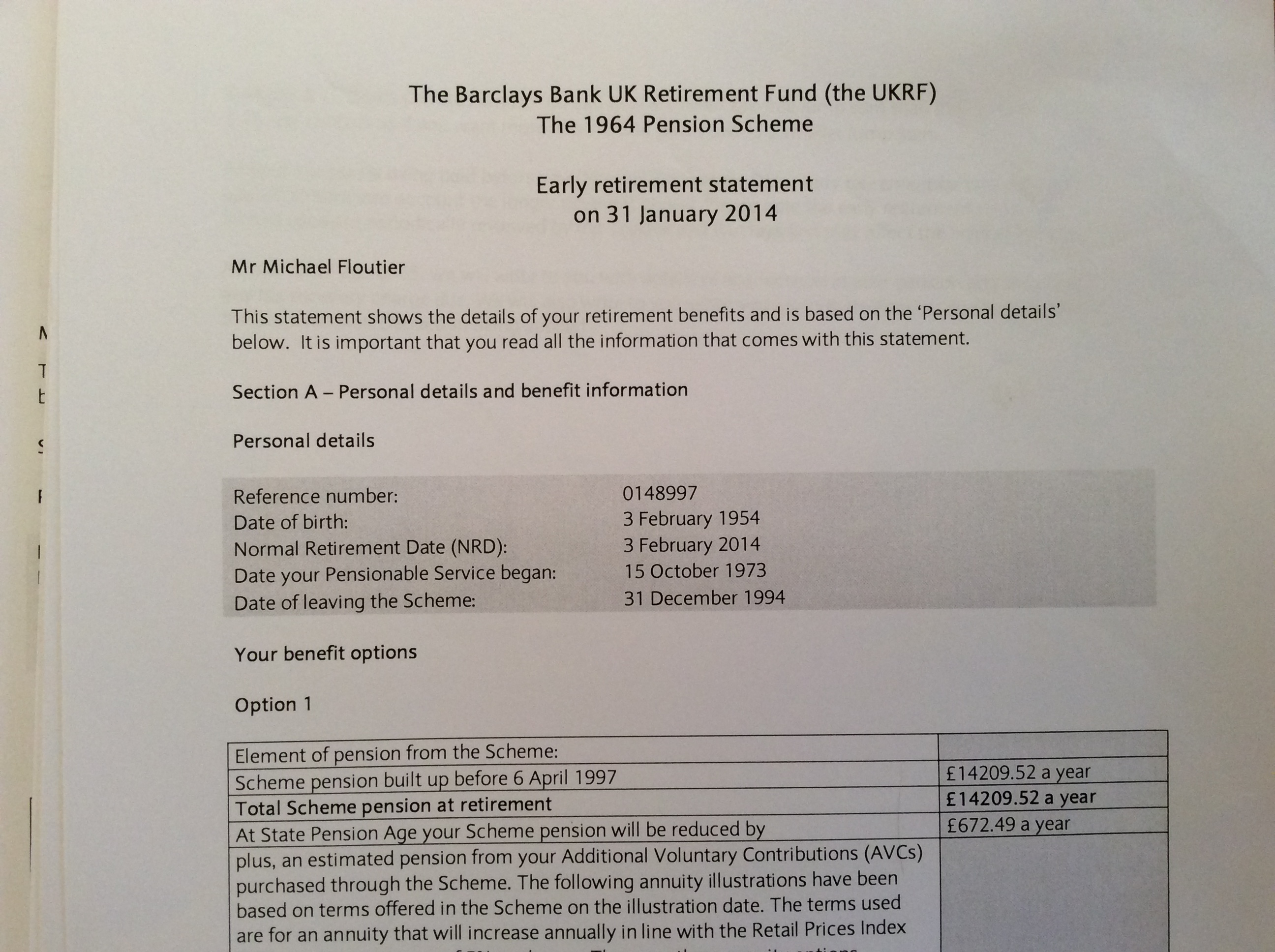

For the sake of completeness, here are pics of two of the pension offers I received at NRD, as you can see the difference in dates is only 3 days.

1

1 -

WTW’s reply is below

I do not think it answers my question as why the excess is reduced by so much as with what I have been told before you only frank increases in the excesses.

As we are equalising just part of the pension and do not have the original figures for the GMP earned it becomes more complicated but I wonder if I need to produce a ‘what if’ scenario as Mike Floutier did originally.

Any thoughts?

The GMP equalisation calculation takes your pension earned between 17 May 1990 and 5 April 1997 and compares it to the pension a member of the opposite sex would have received. When a member reaches GMP payment age, the GMP is incorporated into the total value of the pension and is not added on top, so the excess is reduced. As the GMP age for a woman is age 60, the alternate calculation splits the pension at age 60. Please note that the equalisation exercise only relates to your pension between 17 May 1990 and 5 April 1997, not your entire pension.

When you took early retirement from the Scheme, a test was carried out to ensure that upon reaching age 65 your total pension amount would be enough to cover the level of GMP that you are entitled to.

In order to calculate your early retirement pension, your excess, or non-GMP, benefits were revalued to the date the calculation is produced and then assumed future increases were applied up to your Normal Retirement Age (NRA) of 60. Your GMP (as at your date of leaving) was then added to this value and an early retirement reduction factor was then applied to these benefits, which gave you your Total Pension amount (at your early retirement date).

Your Total Pension will continue to increase in line with the Retail Price Index (RPI) capped at 5% each October until your GMP payment age of 65. Upon reaching age 65, your GMP will be incorporated into the total value of your pension and your pension is split into three sections, and increased as follows:

Non-GMP (increased in line with RPI capped at 5% each October)

Pre 1988 GMP (no increases applied by the Scheme)

Post 1988 GMP (increased in line with CPI capped at 3% each April)

Total Pension as at 65

I appreciate that it may appear that your excess value is being reduced to incorporate your GMP into your pension. However, your GMP value is already included in your Total Pension when you retire but can only be broken down, as shown above, upon reaching age 65.

However, as your GMP benefits could receive a large increase when you reach age 65, a test is carried out to determine whether your benefits are entitled to receive a ‘step-up’. This test involves comparing the increases applied to your pension between your actual retirement date and age 65 against the increase in the GMP. If the increase in the GMP is higher, then the difference is given to you as a ‘step-up’ in your benefits. The example in page 10 of the ‘What happens to your pension when you leave Barclays’ booklet is demonstrating a ‘step-up’.

An early retirement calculation does this ‘step-up’ test immediately at your actual retirement age. It projects the future increases applied to your pension based on assumptions provided by the Scheme Actuary and then compare this to the GMP that will come into payment at age 65, which is known as it revalues at a fixed rate. If the value of your GMP is higher, then a ‘step-up’ will be given at your retirement date.

Please be assured that when working out your pension increases in future, we will check that we are treating benefits equally for men and women, and will make the necessary adjustments.

If you have any further questions, please do not hesitate to contact us.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards