We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

GMP equalisation workings - Barclays pension

Comments

-

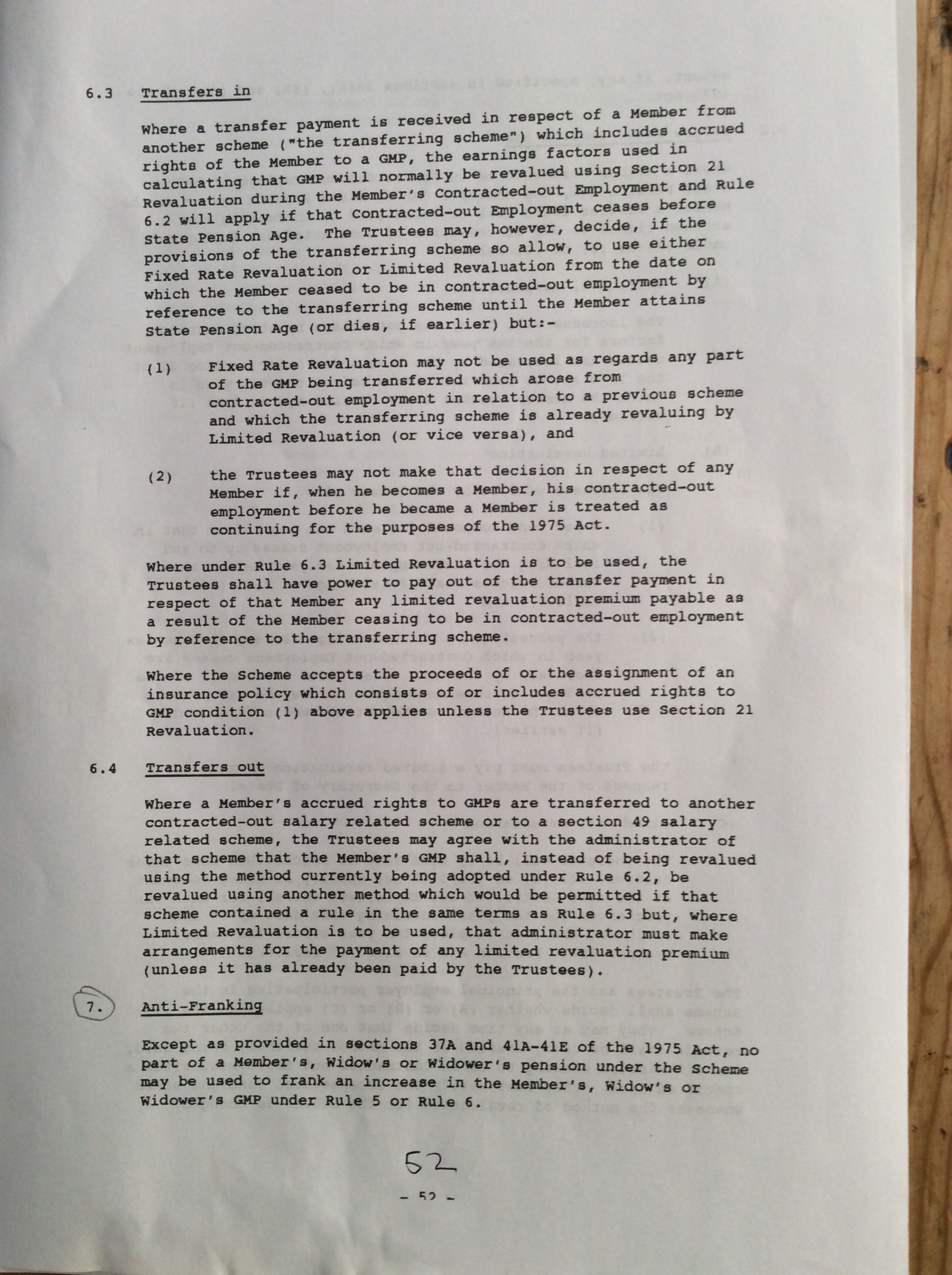

29th deed of variation 15/1/91 page 52

0 -

Again, this seems to be a slight aside to the original question but I think it may be worth looking at:

DT2001 said: My understanding of Franking is that increases in the excess since drawdown can be offset against the GMP revaluation.

———-

Aah, I see where I’ve misunderstood now, plus some additional confusion:

1. In my case Drawdown occurred at my Normal Retirement Date.

2. In Barclays’ proforma (see hopefully attached pic) they say “Increases to Mr Floutier’s pension since Normal Retirement Date are offset against his GMP revaluation”

3. So I thought (not unreasonably) that everyone had their excesses Franked back to their level at NRD (ie. age 60)

4. To add further confusion, I thought I’d have a good read of the Fund rules dated 15/01/1991. (These were the latest set applicable at the time of my calculations; and just post-Barber, which may or may not be instructive.)

5. I had planned to comment on what I’d read, but because of its (to me) complexity, I’ve decided to post pics of the relevant pages.

——

The only comments I’d make are that section 6.2 (c) on page 51 says: “The increase [in GMP from date of leaving COE] will be at such rate [usually 7%]...up to and including the last complete tax year before the Member reaches State Pension Age...”

The question is, should increases in pension be Franked:

1. Back to Drawdown,

2. Back to NRD (60), or

3. Not at all?

PS for some reason I’m having trouble with Quoting and Pic posting within comments so I’ll try to post the relevant pics separately. I may have to repost to sort out formatting; grrr!0 -

And finally, if you really want something to get your teeth into, you may have noticed the exception in the Anti-Franking section “7.” on page 52 which says “Except as provided in sections 37A and 41A - 41E of the 1975 act.”

Here are links to 37A and 41A...I gave up at this point...

https://www.legislation.gov.uk/ukpga/1975/60/section/37A/1991-03-04

https://www.legislation.gov.uk/ukpga/1975/60/section/41A/1991-02-28

Anyone see if there’s any relevance to “the question” in the previous post?0 -

As a matter of interest, have you tried a calculation on this theoretical basis.

When the pension came into payment, the GMP was not included at all, so that all you received at that point was the excess revalued to Scheme NRA.

Up to GMP age, this increased under scheme rules. (x)

To this figure add the GMP revalued to GMP age. (y).

Is there much difference between (x + y) and what you actually received after the step up calculation at GMP age?0 -

Ok, I’ll answer my own question. I’ve just re-read WTW’s reply through again carefully and got a little upset. I then read it through again, a little slower, because they were quoting from their own proforma (see my pic from earlier today). What I then realised they were actually saying was that they were NOT Franking the pension/excess back to Drawdown levels BUT rather, from GMP age (65) to NRD age (60) levels, as per my pro-forma. Something we agreed was acceptable back in the day. So, I think we can agree with the rationale of their calculating AND it remains to check those calculations. By the way, the only element of the calculations I haven’t seen mentioned is the actuarial early retirement factor you accepted for retiring at age 51.5. For example, I was offered the two following factors: Age 58 - 0.891 Age 59 - 0.951 What do you think?

The question is, should increases in pension be Franked:

1. Back to Drawdown,

2. Back to NRD (60), or

3. Not at all?0 -

I am not sure! (No surprise with GMP). I am away enjoying some of The Hundred so will look at next week. The thing that I can’t tally in my mind is if the email in 2018 with the calculation at 65 was correct (and WTW agreed it’s methodology) the ‘excess’ was £4.6k and the period from 1990 to Dec 1995 (when I left) related to about a 1/3 of my total service the excess for this calc should be say £1500.MikeFloutier said:

Ok, I’ll answer my own question. I’ve just re-read WTW’s reply through again carefully and got a little upset. I then read it through again, a little slower, because they were quoting from their own proforma (see my pic from earlier today). What I then realised they were actually saying was that they were NOT Franking the pension/excess back to Drawdown levels BUT rather, from GMP age (65) to NRD age (60) levels, as per my pro-forma. Something we agreed was acceptable back in the day. So, I think we can agree with the rationale of their calculating AND it remains to check those calculations. By the way, the only element of the calculations I haven’t seen mentioned is the actuarial early retirement factor you accepted for retiring at age 51.5. For example, I was offered the two following factors: Age 58 - 0.891 Age 59 - 0.951 What do you think?

The question is, should increases in pension be Franked:

1. Back to Drawdown,

2. Back to NRD (60), or

3. Not at all?

In 2018 WTW said they could not confirm figures until nearer the time so I wonder if there is an obligation to divulge how they arrived at the current ones?

I will look at Xylophone’s theoretical calculation as well. If we knew the GMP starting figures for ‘the alternative’ it would be ideal but my son (who is an A level mathematician) has worked back from the GMP figure in payment (again not exact as we have a part year payment).

I do disagree with the the GMP was not included at all statement as, again on the 2018 calc., we have been able to split the figure into excess and original/starting GMP. Relatively small but still identifiable.

As usual my head hurts starting to contemplate this. I think I have the gist but not the details ….1 -

Not sure if you’ve seen this one but it shows clearly the method of calculating GMP (ie. the base/starting figure that is calculated AT the date of leaving COE) for both men and women AND it’s also clear that the figure for women will be different from men.DT2001 said:

If we knew the GMP starting figures for ‘the alternative’ it would be ideal but my son (who is an A level mathematician) has worked back from the GMP figure in payment (again not exact as we have a part year payment).I do disagree with the the GMP was not included at all statement as, again on the 2018 calc., we have been able to split the figure into excess and original/starting GMP. Relatively small but still identifiable.

As usual my head hurts starting to contemplate this. I think I have the gist but not the details ….

https://www.gov.uk/guidance/how-to-calculate-your-scheme-members-guaranteed-minimum-pension

1 -

I have copied my follow up question and WTW ‘s reply.

It seems to imply that my previous understanding and their confirmation of the methodology is incorrect (unless I have misunderstood it). I think he is saying GMP will replace my excess in its entirety if the GMP element is larger than the amount in payment at 65 less one day.

Does anyone read that differently ?Thank you for your detailed reply.I think I understand the process and include a PDF below. On the left handside I have annotated the figures and methodology that your colleagues agreed in Sept 2018 relating to the GMP calculation at 65.I think that the excess does reduce not only by the splitting into GMP and excess but also by franking any increases from the date of drawdown. I cannot confirm your original figures relating to equalisation as I could with the figures to 65 however I have worked back from those on your letter.The excess should revert to the actuarially reduced figure that would have been paid at in 2011 and I cannot tally with how you have come to the figure that you have.Can you please explain if I am correct or if not why as I think I have applied the rules your colleagues were happy with in 2018 (I know that the method has been applied to a few other pensioners when reaching 65).WTW reply isAs you have taken early retirement from the scheme when you reach your Guaranteed Minimum Pension (GMP) age of 65 your pension benefits will only be increased if the Pre 6 April 1997 Excess Scheme Pension amount is less than the GMP amount. If this is the case the Pre 6 April 1997 benefits will be replaced by the GMP amount.

As part of the early retirement calculation a “step-up” test is carried out. This test compares the assumed increases that will be applied to your pension between your actual retirement date and age 65 against the increase in the GMP element of the pension. If the increase in the GMP is higher then the difference is given as a ‘step-up’ in the pension benefits from the early retirement date and not the GMP date.

If you have any questions please contact us.

0 -

Is this fairly recent article of interest in this connection?

https://expertpensions.co.uk/lets-be-frank-what-do-you-know-about-gmp-franking-by-douglas-watson/#:~:text=Simply put, the term “franking,member left contracted out employment.

1 -

Firstly,DT2001 said:...As part of the early retirement calculation a “step-up” test is carried out. This test compares the assumed increases that will be applied to your pension between your actual retirement date and age 65 against the increase in the GMP element of the pension. If the increase in the GMP is higher then the difference is given as a ‘step-up’ in the pension benefits from the early retirement date and not the GMP date.

If you have any questions please contact us.

It seems to me that the “step-up test” mentioned by WTW amounts to full Franking, ie. the GMP increase is reduced by the level of the increase in “the pension” between (in your case) ages 51.5 and 65.

Four things:

1. According to Xylophone’s “expert pensions” link, ERD pensions can be fully Franked.

2. It's unclear to me, when referring to “the pension”, whether WTW mean the entire pension, or just the excess. Clearly this would make a big difference.

3. They refer to the: “Pre 6 April 1997 Excess Scheme Pension amount”. I’ve not come across this term before, any ideas?

4. Also WTW mention that, “a ‘step-up’ in the pension benefits from the early retirement date and not the GMP date.” It’s unclear, to me, just what this means; is it a back-dated increase?

—-

Secondly,

I wonder if you have, as I did, roughly worked out the benefits of your ERD pension, calculating forward to say age 85, and compared this with the benefits that would have accrued, had you taken the NRD pension.

This would go some way to allaying any doubts you may have regarding the calculation of your ERD pension.

Presumably you would need to factor in a figure to represent the opportunity cost of deferment implicit in the NRD figures (although I'm just speculating here)0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards