We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

GMP equalisation workings - Barclays pension

I have received notification from Willis Tower Watson administrators of Barclays 1964 Pension Scheme that I have been underpaid as a result of GMP equalisation since drawing my pension early 10 years ago at 51 1/2. They are paying me a lump sum plus interest to cover the whole time and increasing my current payments.

It is a pleasant surprise as although I thought the Lloyds Bank case might work in my favour as I had taken redundancy in 1995 so my GMP has had many years to build up, the complexity of GMP made me wonder if I had interpreted the information correctly.

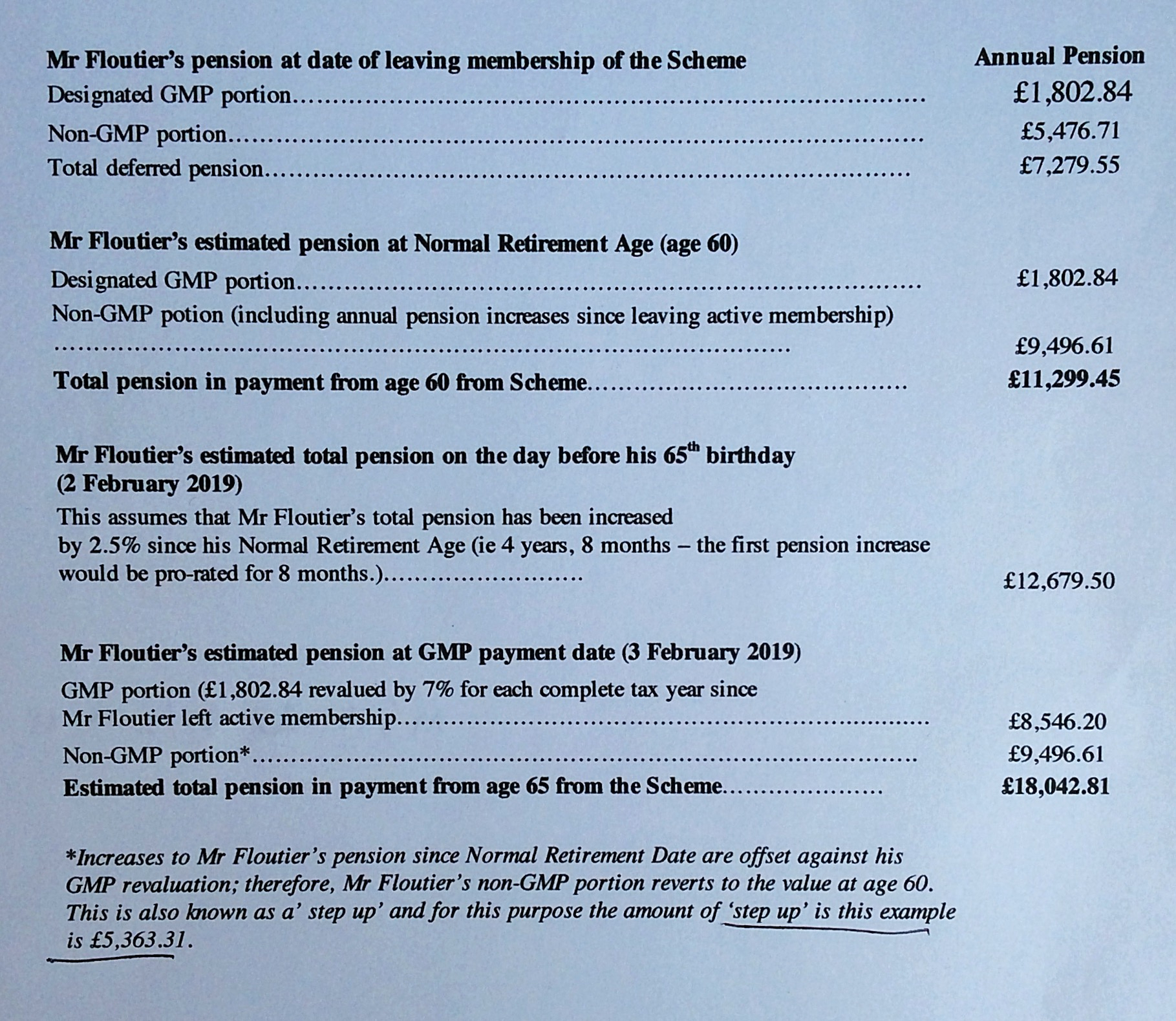

4 years ago with the help of xylophone and Mike Floutier I unravelled what would happen to my pension at 65. Simply I would end up with about £4.5k GMP pre 88 (subject to no increases), £4.5k GMP post 88 with CPI max. 3% increases and £4.5k ‘excess’ with RPI increases max. 5%. My ‘excess’ at 64 would be about £7.5k (dependent on increases during the intervening years) however it reverts to the original figure that I first drew at 51 1/2 as the increases ‘suffer’ franking.

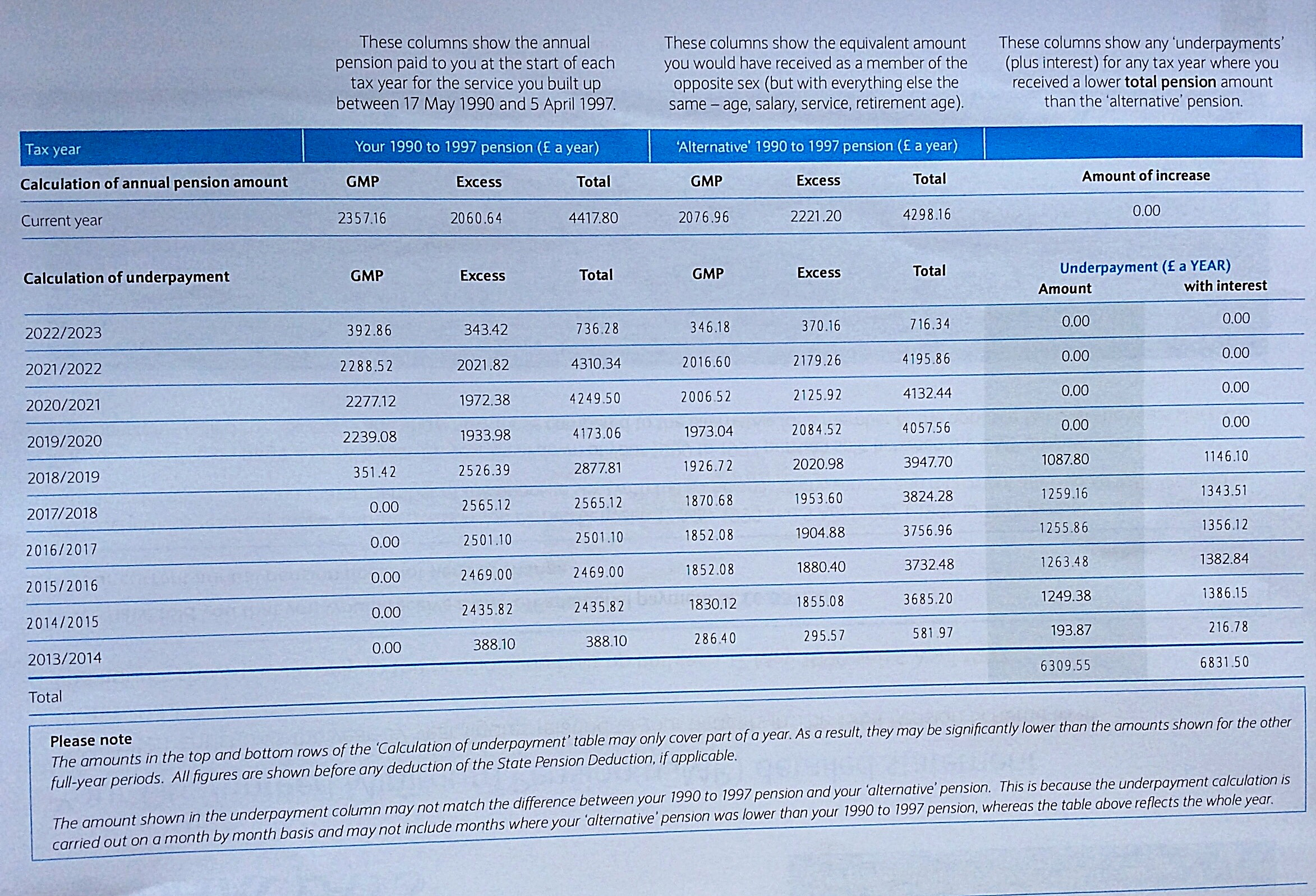

I have been provided with a table which shows the year by year figures for the build up in pension post 1990, as they were and as they would have been had I been female.

In 2020/21 the total figure for the equivalent pension is GMP £2.3k excess £775. The following tax year GMP is £2.7k and the excess £416. I have worked out that the drop in excess and increased GMP between those 2 years is down to 2 months of the former being before I turned 60.

The 1st year of the table only covers a part year however the 2nd shows the excess as £2553 (I think this figure should be part excess and part original GMP amount) So I am wondering how a figure of £400+ is arrived at as I thought the excess would revert to the amount (portion post 1990) when drawn 10 years ago.

I have asked WTW to explain how they arrive at that figure and what effect it has on the calculation at 65.

It is complex as the GMP is split and the equalisation comes in 2 years after the split. Of my current pension £5.5 k is pre 1990 and £2.9k post. GMP was £1339 at date of leaving in 1995. The whole pension receives inflation increases in deferment and payment but the GMP is revalued from date of leaving to 65 less a franking adjustment on the excess.

WTW were contradictory last time before we managed to ask the correct question in a format they were willing to answer so can anyone explain how they think it should be worked out?

Comments

-

I have received notification from Willis Tower Watson administrators of Barclays 1964 Pension Scheme that I have been underpaid as a result of GMP equalisation since drawing my pension early 10 years ago at 51 1/2.

Snap....

") You and Mike F are in sync

You and Mike F are in synchttps://forums.moneysavingexpert.com/discussion/comment/79290779/#Comment_79290779

Its been a good week, yesterday Barclays (my final-salary pension) just sent me £4,700 having done the equalisation calculations on my GMP. Plus it looks like the good old HMRC will be refunding me around £800 of the tax Barclays sent them.WTW were contradictory last time before we managed to ask the correct question in a format they were willing to answer so can anyone explain how they think it should be worked out?What anyone thinks won't help you - you'll need to ask WTW for their methodology as there is a choice of methods of equalisation.

2 -

Thanks xylophone, great link. I think I know which method they used but cannot see anything about why franking appears to apply.

Also interested to see if it affects my calculation at 65.

Will post WTW’s reply in due course.2 -

DT2001 said:Thanks xylophone, great link.

Will post WTW’s reply in due course. I’ll be very interested also, as having read quite a bit about this subject, I find I’m having trouble knowing how to approach thinking it through.

I’ll be very interested also, as having read quite a bit about this subject, I find I’m having trouble knowing how to approach thinking it through.

Initially I was happy simply to receive the lump sum but now I feel it’s probably worth checking things, an approach that yielded much fruit in the past.

Here is a copy of the highly simplified version of the general methodology along with the calculations relating my own circumstances.

It would appear that the methodology is sound, but the checking of the figures would could be somewhat difficult.

If someone could suggest an approach for checking these figures I do be happy to give it a go, but without knowing what I was doing I don’t think I’d like to even start.

Anyway, let’s wait for WTW...1 -

Ok, so looking at the figures in the photo sheet, in the previous post, I have attempted to confirm the calculation of one of the figures.

The figure I chose is the Total pension for me for the year 2019/2020, ie. £4173.06. The heading of this column is "Your 1990 to 1997 pension (£ a year)".

To do the calculation I took my total pension for that year (before SPD, as stated), approximately £17,000 and apportioned 21.78% of it, ie. £3,702. The proportion percentage is based on "My years of service during the Barclays Barber Window (1990 to 1997), (4.62) divided by my total years service (21.21), giving 21.78%.

This result, ie £3,702, is considerably less than the figure of £4173.06 mentioned above and contained in the chart.

I'm quite happy to concede that my method or calculations may be awry, but that's just my "starter for 10" to get the ball rolling.

Any thoughts?0 -

Although I’m usually right behind people checking their pension figures, I have to say I think it’s going to be really hard to get anywhere here (and I say this as a scheme actuary myself to a number of DB schemes going through this process). GMP equalisation is a complex area at the best of times, and your scheme seems more complicated than normal with its treatment of GMP (i.e. ‘funky’ non-standard step ups, which is not the way most schemes do it). By all means ask WTW, nothing to lose, and good luck! But I think you need to expect that it might remain very hard to understand, even if you get through to someone knowledgable at WTW, which is going to be hard in itself.

Thanks for sharing the correspondence, as someone who works for a different firm of actuaries it is interesting to see the level of detail that WTW are providing (which is higher that I would instinctively have expected).5 -

Thanks for this Mavwa, it’s certainly eye-opening to hear a view from the coal-face.mavwa said:Although I’m usually right behind people checking their pension figures, I have to say I think it’s going to be really hard to get anywhere here...

It is also our experience that the process of checking is hard. However, since some members have, in the past, been asked (through Franking) to accept smaller pensions than implied by scheme rules and pension law my feeling is that it’s worth the effort; especially given the huge number of people affected by GMP equalisation.

You also mentioned being surprised at the level of detail offered by WTW. Barclays do have a history of doing this; I imagine it is intended to stave off enquiries. It is to be welcomed though. In fact it was through this kind of disclosure that we were helped to agree fair pension figures in connection with the Franking dispute.

In that spirit, I would ask that folk cast an eye over my methodology and calculations contained in my posts yesterday.

Many thanks!

Mike0 -

STOP CONSIDER THE FOLLOWING BEFORE GOING ON

STOP CONSIDER THE FOLLOWING BEFORE GOING ON

IVE SINCE RETRACTED THE SUGGESTIONS IN THIS POST BE HAVE NOT DELETED IT TO HELP WITH THE FLOW OF COMMENTS

I know that sounds a little dramatic but this has just occurred to me and it’s very straightforward.

Barclays agreed that my pension should receive a (GMP revaluation) step-up at my GMP age of 65. This step-up was over £5,000 pa. (see attached pic for details)

Had I been a woman, my GMP age would have been 60.

You see where I’m going. Should I not have received my step-up at age 60 (under Barber/Lloyds).

So shouldn’t my GMP equalisation payment be 5 x my step-up?

Or am I missing something?

0 -

You see where I’m going. Should I not have received my step-up at age 60 (under Barber/Lloyds).

My two penn'orth, I'd say no to this.

B/L did not change the fact that GMP age for men and women was different. It simply sought to address any inequality which might have arisen from the difference.

Nor did it change the fact that SPA for men and women was different (and at that stage GMP age and SPA were intimately connected).

And in 1990, the change to SPA for women had not been brought forward to parliament nor was any increase in SPA for both sexes under formal discussion (although when you read through the linked paper below) it's clear a head of steam was building).

So shouldn’t my GMP equalisation payment be 5 x my step-up?Wanting jam on it?

And what saith the Good Book about the love of money?

") 0

0 -

And now all your days are spent in a deckchair ... you might need some light reading

https://commonslibrary.parliament.uk/research-briefings/cbp-7405/#:~:text=Supporting documents&text=The Pensions Act 1995 provided,period April 2010 to 2020.

0 -

Incidentally, I've a relative who has received the news that Barclays have actually "done the deed" in respect of GMP equalisation with great interest (and envy alas...) - he was a member of a DBFS scheme between 1990 and 1997 but while the Trustees acknowledge the Lloyds judgement so that "something must be done", they are in no hurry to say what!0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards