We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Assistance with improving my pension fund choices

danlightbulb

Posts: 950 Forumite

Hi all,

Further to recent thread on savings rates where I'd posted an ad-hoc comment about my pension fund, I was prompted to go online and have a more detailed look.

For background, I am in a defined contribution scheme ran by Aegon. My employer puts in 6% which is the maximum, and I have been putting in 8% for a while but recently upped it to 10%.

When it was all set up the company I work for, along with Aegon, originally configured a fund choice which was meant to be balanced, and as you approach retirement they automatically adjust the proportions to move more of your fund into lower risk investments. I am still in this default fund choice because I have never changed it.

I have occasionally logged in (but not for a couple of years now) and looked at the other fund options available as if I want to I can configure my own mix of funds. There are around 80 different funds to choose from.

I have had a more detailed look at the two funds Im currently invested in, and a handful of the others. Unfortunately, the two default ones I'm currently in, chosen by the company at the time it was all set up, do not appear to have performed as well as some of the other (even lower risk) ones.

I don't know how best to evaluate what I should do here?

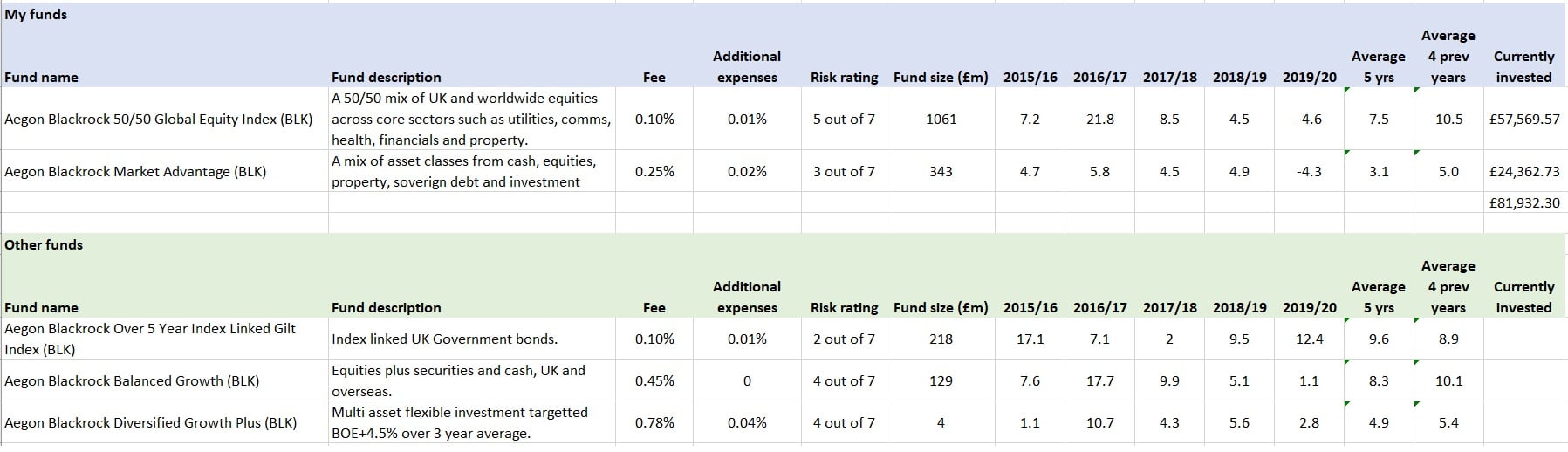

As examples initially, until I get some ideas going, here is the performance of my two funds that I'm currently in. I have 70% in the first one and 30% in the second.

In particular, I notice that funds such as a '5 year gilt index' are badged as nominally lower risk, have a lower management fee and appear to have performed better.

How do I begin to improve my position, as with 80 funds available, its a bit of a minefield?

Thanks

Further to recent thread on savings rates where I'd posted an ad-hoc comment about my pension fund, I was prompted to go online and have a more detailed look.

For background, I am in a defined contribution scheme ran by Aegon. My employer puts in 6% which is the maximum, and I have been putting in 8% for a while but recently upped it to 10%.

When it was all set up the company I work for, along with Aegon, originally configured a fund choice which was meant to be balanced, and as you approach retirement they automatically adjust the proportions to move more of your fund into lower risk investments. I am still in this default fund choice because I have never changed it.

I have occasionally logged in (but not for a couple of years now) and looked at the other fund options available as if I want to I can configure my own mix of funds. There are around 80 different funds to choose from.

I have had a more detailed look at the two funds Im currently invested in, and a handful of the others. Unfortunately, the two default ones I'm currently in, chosen by the company at the time it was all set up, do not appear to have performed as well as some of the other (even lower risk) ones.

I don't know how best to evaluate what I should do here?

As examples initially, until I get some ideas going, here is the performance of my two funds that I'm currently in. I have 70% in the first one and 30% in the second.

In particular, I notice that funds such as a '5 year gilt index' are badged as nominally lower risk, have a lower management fee and appear to have performed better.

In particular, I notice that funds such as a '5 year gilt index' are badged as nominally lower risk, have a lower management fee and appear to have performed better.How do I begin to improve my position, as with 80 funds available, its a bit of a minefield?

Thanks

0

Comments

-

Just one point to be aware of is that the info you are looking at is only up to 30/06 . Probably a more up to date valuation would look a bit better .

Default funds tend to be middle of the road, with average performance at best . Companies usually play safe in their choice as it reduces the risks of big drops in employees pension funds, during a market downturn , which would kick off a lot of complaints as nearly all employees will be in the default fund . Only a small % venture into changing the funds.

In particular, I notice that funds such as a '5 year gilt index' are badged as nominally lower risk, have a lower management fee and appear to have performed better.

Note the investment mantra ' past performance is no guarantee of future performance '

0 -

@Albermarle thanks.

I do understand that investments can go down as well as up, and past performance is no guarantee. I do want to ensure I have a good level of diversity in my choices. Obviously there is a lot of data here - there is a pdf giving lots of information for all 80 of these funds so there is alot to try and absorb. I'm making a spreadsheet of fund performance and fees for each one, along with a description of what sectors or asset classes it is made up of.

Regarding the timespan, my online dashboard shows me my fund value as of today, and I can access various timescales over which to analyse performance. The pdf's themselves appear to be updated quarterly, and they show previous years performance and then 3 months, year to date, etc as you can see.

So there is potentially lots of data here I could use, and far too much for me to post here.

0 -

comparing your presumably equity heavy current investments with a 5 year gilt fund is chalk and cheese. You probably need to do some basic reading on investments, look at the monevator website and maybe buy a book or two. Once you have a basic understanding of investments then you can asses your situation and determine a portfolio that you would be comfortable with in terms of risk and which may meet your future requirements. That will allow you to have an asset allocation and you can then compare that against your fund options and select one or more that align with your researched needs1

-

There'll always be an investment that performs better than the one you are invested in. Better to target an optimum outcome rather than a maximum outcome. How much do you currently have invested in the funds? It's good to have a solid core before diversifying further.0

-

The 50/50 Global equity fund has performed poorly because 50% of the allocation is toward UK equity which is 20% down over a year compared to other markets (like the US) which are positive.

It's not necessarily a bad investment, it's just, with hindsight, been a bad investment this past twelve months. Next twelve months could be different though.

If you want to amend the portfolio you should do so with the future not the past in mind. If you want to go chase gains and dial up the risk then ditch the bonds and go equity, and inside the equity introduce EM, small cap. If you'd rather have less volatility and are willing to sacrifice some gains to achieve that, then potentially reduce equity exposure, and don't have EM/small cap.

What has happened has happened. You can't change the past.1 -

One place I go to compare funds is Trustnet. This link should give you a filtered list of all of the Aegon pension funds but it seems there are over 1000, whereas you have access to just 80? Still should be enough to pick from.

https://www.trustnet.com/fund/price-performance/p/pension-funds?tab=fundOverview&manager=SCOE&pageSize=25

0 -

@NottinghamKnight thanks, I will do some more research for sure. I appreciate the types of funds are different (yes my current one is equity split across a range of sectors from utilities to healthcare to financial sector).

Thrugelmir said:

Hi I have £82k currently, having been in the scheme for 16 years now. I have 25 years left in it taking me to 65, and as I stated I have begun to increase my contribution (Ive been getting about 2% payrise for the past couple of years which Ive put straight onto my pension contribution, which is tax efficient).There'll always be an investment that performs better than the one you are invested in. Better to target an optimum outcome rather than a maximum outcome. How much do you currently have invested in the funds? It's good to have a solid core before diversifying further.

I understand that just comparing numbers is not enough and I certainly don't want to target maximum outcome because that comes with higher risk, so yes 'optimal' is a word that fits very well with what I want to achieve.

Looking at the numbers though, the historic year on year for my funds compared to a couple of other ones (see below):MaxiRobriguez said:The 50/50 Global equity fund has performed poorly because 50% of the allocation is toward UK equity which is 20% down over a year compared to other markets (like the US) which are positive.

It's not necessarily a bad investment, it's just, with hindsight, been a bad investment this past twelve months. Next twelve months could be different though.

If you want to amend the portfolio you should do so with the future not the past in mind. If you want to go chase gains and dial up the risk then ditch the bonds and go equity, and inside the equity introduce EM, small cap. If you'd rather have less volatility and are willing to sacrifice some gains to achieve that, then potentially reduce equity exposure, and don't have EM/small cap.

What has happened has happened. You can't change the past.

When I look at this I think the following:

* The 50/50 global equity fund (70% of my investment) is ok apart from this last year. Its averaged 7.5% pa over 5 years and 10.5% if this last year is discounted.

* However the Market Advantage fund, which has a higher fee, (30% of my investment) looks to be letting me down. I could have done better in all of the three other funds I have picked as examples at the bottom, but particularly the UK Government bonds fund jumps out because not only has it done better but its got a lower fee, and its lower risk as well.

0 -

Ive continued compiling my list of available funds and am noticing some patterns which means I have a couple of general questions.

Alot of these funds are comprised of different mixes of equity (directly and via other funds) across the developed world. Obviously there will be some commonality between these funds, i.e some correlation and they will have the equities of the same sectors just in different mixes. There are many of these, across risk levels 3 to 5 out of 7, so around medium.

Is it worth diversifying into different funds which are essentially just different mixes of the same type of thing? So for example my current 50/50 global equities fund has 70% of my investment. But there is also a 40/60 fund and presumbly a 60/40 fund or a 30/70 fund. Instead of putting 70% in the 50/50 fund, I could put a third in each of the 50/50, 60/40 and 70/30 funds for example. Its still equities, and its still various sectors, and probably in many cases the same underlying companies.

Ive also noticed that when emerging markets start to be included, the risk factor goes up to 6 or 7 out of 7. Some of these funds have done quite well but obviously I wouldn't put much more than 5% (?) in these, so is it worth it?

Same question with gold funds. Again they appear to have done exceptionally well, but are they worth it for small amounts (5%)?

Some funds are a mix of equities and bonds/gilts/debt instruments. Should I aim to put a proportion into these kinds of funds as well as entering the solely equity funds like the 50/50 or 60/40?

There doesn't seem to be much of a correlation between fund performance and management fee, which is disappointing as one might assume paying a bigger fee gets you a better fund manager.

Also Im noticing that funds with an 'ethical' component seem to do worse. I'll not be bothering with these then?0 -

OP - You really need to do some basic research as you are just floundering around. Take some time to read and come back in a few weeks with a structured plan, you can set up free portfolio accounts with trustnet or morningstar and this will give you a breakdown of asset allocation so allow you to see investments by geography, class, industry etc2

-

Hi. I am doing research, and those are the questions I have, I don't feel like I am floundering. I can see all the details of the asset classes, geographical regions of all these funds from the information I am given in my online dashboard, but that is far too much information to post here. For example the pdf's of each fund give me information like this:NottinghamKnight said:OP - You really need to do some basic research as you are just floundering around. Take some time to read and come back in a few weeks with a structured plan, you can set up free portfolio accounts with trustnet or morningstar and this will give you a breakdown of asset allocation so allow you to see investments by geography, class, industry etc

My outline plan would be to have a percentage of my money in a few different funds that would give a good spread of investment in the different asset classes and geographies without having too much risk.

I'm currently 70% invested in a 5 out 7 risk fund, 50/50 global equities, and 30% invested in a 3 out of 7 risk rating fund which is also equities plus some cash, property and sovereign debt.

I could still be invested in those things but instead of being in just two funds I could be in several at lower proportions.

I'm not sure what you think I need to research further? Im not going to be making minute detail decisions like 'I want to be 2% invested in Japan", because that's just guesswork? But instead I could choose a fund which has a bit of Japan already in it?

It looks to me like the main variables are:

* Asset class mix

* Geographical region or country

* Risk level

* Whether the fund is aiming to track a benchmark or beat it

* The management fee

* Whether the fund includes emerging markets or emerging companies (higher risk)

* How it has historically performed

* How it might perform in the future (guesswork)

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards