We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Regular Savings Accounts: The Best Currently Available List!

Comments

-

I'm sure I've seen an option within the App and/or online banking where we can change the limits? Perhaps you've already tried it and it was a no go or the option is greyed out?

1 -

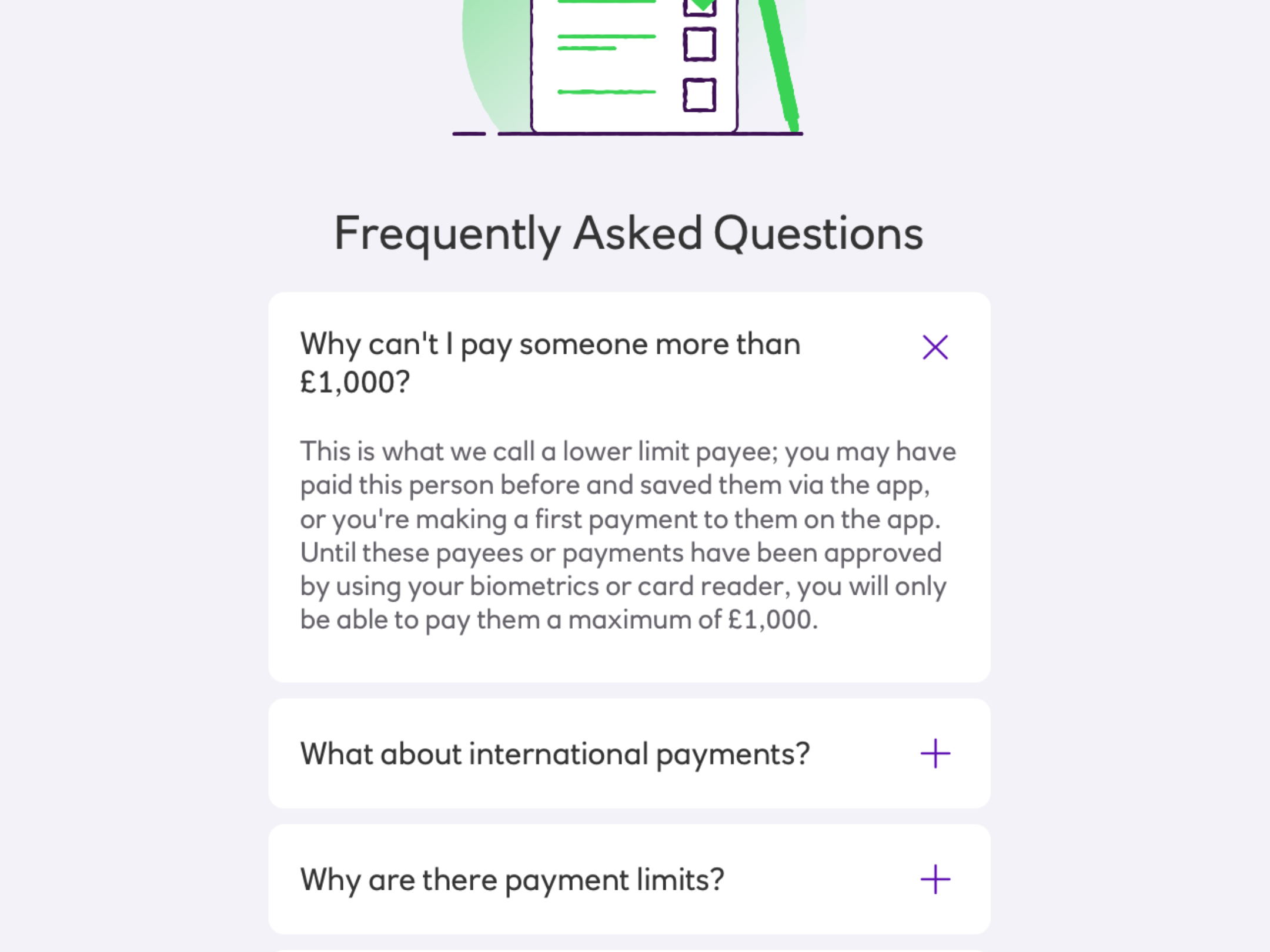

The £1,000 limit is only for new payees set up on the app. See the NatWest FAQ below.

5

5 -

I've used Natwest for my main bank account for years and never had any problems.

The Regular Saver is an excellent account. It might be a pain waiting for the first standing order to be activated but after that it's plain sailing. The 'double roundups' on the current account is a good way of squeezing more cash into the savings account each month.

I've not had a problem with payment limits but I have biometric authentication enabled in the app - I think this allowes you to make larger payments.

3 -

Natwest (like RBS/Ulster) accounts take ages to set up when you are completely new to them. Once set up, they are plain sailing.

Payments to new payees can be authenticated with the app.

As has been discussed on here before, for their digital regular saver, you have to set up an SO from a Natwest current account as part of the application for the RS, but you can immediately cancel it, you never have to use it. As soon as you have completed the application for the RS, you have the sort code and account number for it and you can instantly transfer your first £150, either by internal transfer or by FP from a non-Natwest accounts. Any subsequent regular monthly £150 deposits can again be done by manual deposit/transfer or by an SO, from a Natwest or a non-Natwest account.

For completeness, I should mention that you don't have to deposit anything at all each month, and you can make as many deposits as you like up to the £150 limit per month. On top of those monthly £150, you can also make an unlimited number of deposits from Round-Ups/Double Round-Ups created from your Natwest debit card spending. I don't bother with round-ups myself but if it floats your boat, you can add extra to your RS balance.

You can also do the exact same thing again with RBS. Sadly not at Ulster Bank though.

3 -

I have biometric authentication in the app, but I'm limited to £1k, and that has been blocked by the fraud team.

It is just so archaic compared to most banks, particularly the challenger banks, where you can open an account and use it instantly.

1 -

It seems clear that Natwest, and therefore RBS, is not for you.

I, on the other hand, think they are brilliant for newbies because you can start with a switch bonus, and the RS is really nice. They also have a Reward credit card which pays 1% cashback on all supermarket shopping (and 0.25% on everything else) and is free for Reward account holders. All in all, a lot more than some other banks are offering. What's more, having a Natwest/RBS account doesn't stop you from also having accounts at any number of other banks 😎2 -

I've just looked at my Natwest DRS and at the interest paid for this month (£8.68) to see that is lower than the interest paid last month (£9.07). I've paid the £150 in monthly ever since the increase allowed this so I'm confused.

Any thoughts as to why this would be?

0 -

Interest is paid based on the number of days in the month. March = 31, April =30.

4 -

29 days / 33 days = 87.88%

(The first day of May was a bank holiday and added to April, but the first two days of April were a weekend and added to March.)The balance increase from March to April would have needed to be more than 13.79% (33/29) to surpass the interest earned from the extra days of the previous interest period.

1 -

OK. Trying to withdraw £1000 of the £1250 that I paid in resulted in my account being blocked. That prevented me from linking Paypal and Currensea.

The Fraud Team have lifted the block on the account, and I have now been able to link Paypal and Currensea.

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.3K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 248K Work, Benefits & Business

- 605.2K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards