We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Regular Savings Accounts: The Best Currently Available List!

Comments

-

colsten said:

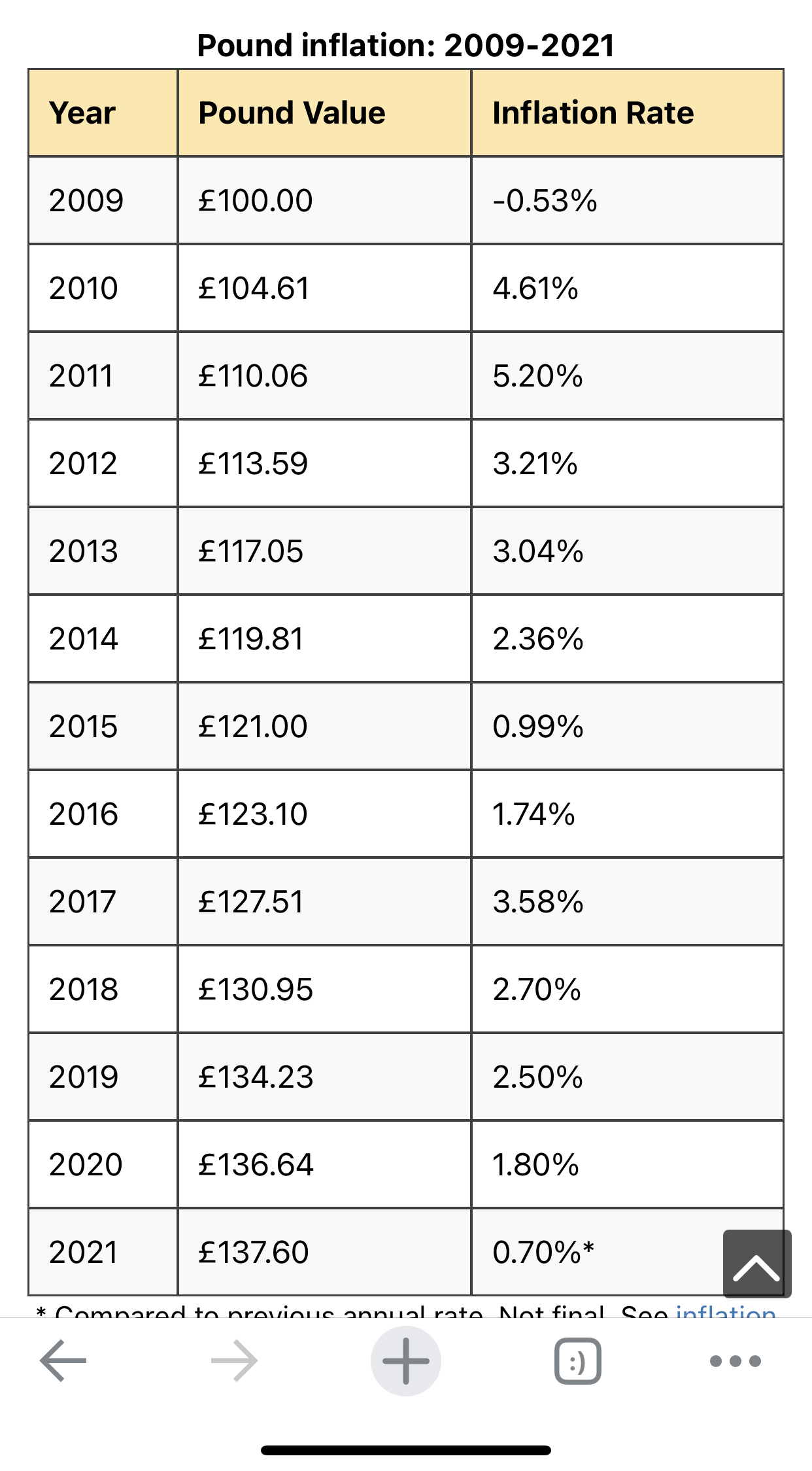

What was inflation then, what is it now?SA100 said:Was chucking out some paperwork from my Grandmothers house and found her 10% HSBC Reg Saver. It was mid-2000's. Oh, how I wish I was saving then. Currently nearing the end of my 2.75% HSBC/FD Saver. Will be sticking everything in Premium bonds at renewal.I addressed this a few months ago.I had an HSBC Regular 10%, started 11/2008. The RPI for 2009 was MINUS 0.5%Also a Halifax Regular at 12%.

1 -

glider3560 said:

For the Bath Homestart Regular Saver, there is no locality requirement (it's the only one of their RSs that don't have this). I just opened one last week as a new member and don't live or work anywhere near Bath.Special_Saver2 said:Bath BS Homestart Regular Saver

Interest rate: 1.15% gross p.a. variable

Monthly payment: £50-£250

Miss any payments: Yes, as long as you do not miss payments for two consecutive months

Penalty-free withdrawals: Yes, you can make two withdrawal per calendar year

Age of applicant: Aged 18-34

How to open account: Branch or post

Special conditions: Maximum balance £57,000. Payments from other Bath BS accounts are not allowed. You must be able to prove that you live, work or study in Bath.Additional information

- Available for UK residents only, applicants must be aged over 18 and apply before their 35th birthday.

1 -

The RPI for 2009 was actually 2.4% https://www.swanlowpark.co.uk/retail-price-indexpolymaff said:colsten said:

What was inflation then, what is it now?SA100 said:Was chucking out some paperwork from my Grandmothers house and found her 10% HSBC Reg Saver. It was mid-2000's. Oh, how I wish I was saving then. Currently nearing the end of my 2.75% HSBC/FD Saver. Will be sticking everything in Premium bonds at renewal.I addressed this a few months ago.I had an HSBC Regular 10%, started 11/2008. The RPI for 2009 was MINUS 0.5%Also a Halifax Regular at 12%.

But I was asking what the inflation rate was, so I now looked it up. You are right, it was negative in the aftermath of the financial crisis but wuickly rocketed again.

1 -

colsten said:

The RPI for 2009 was actually 2.4% https://www.swanlowpark.co.uk/retail-price-indexpolymaff said:colsten said:

What was inflation then, what is it now?SA100 said:Was chucking out some paperwork from my Grandmothers house and found her 10% HSBC Reg Saver. It was mid-2000's. Oh, how I wish I was saving then. Currently nearing the end of my 2.75% HSBC/FD Saver. Will be sticking everything in Premium bonds at renewal.I addressed this a few months ago.I had an HSBC Regular 10%, started 11/2008. The RPI for 2009 was MINUS 0.5%Also a Halifax Regular at 12%.

But I was asking what the inflation rate was, so I now looked it up. You are right, it was negative in the aftermath of the financial crisis but wuickly rocketed again.The monthly figure for December 2009 was 2.395% - but we are discussing a 12-month account, predominantly in 2009 - and I quoted the government's figure for all of 2009.The point is that - see previous posters - it is generally assumed that, in the past, inflation was wiping out high interest rates. Not so. The case in hand was an extreme case of that being not true - but over the previous 20 or so years, you could get rates well in excess of inflation.The best I ever got was 17% easy access during a period when inflation was about 8%. Where would you get over double the rate of RPI, easy access, now?EDIT: BTW, the "RPI for 2009" started at 214.8 and ended at 213.7. You're not alone in quoting a figure derived from the division of two RPIs as being, itself, "RPI". This misdescription makes the understanding of RPI data by the public (even) more difficult.

2 -

I have just looked at the ONS website, and cannot see either of the figures you have quoted. Am I missing something? If you wish you can reply on a new thread to avoid digressing too much on this one.polymaff said:EDIT: BTW, the "RPI for 2009" started at 214.8 and ended at 213.7. You're not alone in quoting a figure derived from the division of two RPIs as being, itself, "RPI". This misdescription makes the understanding of RPI data by the public (even) more difficult.RPI

Dec 2008 212.9

Jan 2009 210.1

Dec 2009 218.00 -

RG2015 said:

I have just looked at the ONS website, and cannot see either of the figures you have quoted. Am I missing something? If you wish you can reply on a new thread to avoid digressing too much on this one.polymaff said:EDIT: BTW, the "RPI for 2009" started at 214.8 and ended at 213.7. You're not alone in quoting a figure derived from the division of two RPIs as being, itself, "RPI". This misdescription makes the understanding of RPI data by the public (even) more difficult.RPI

Dec 2008 212.9

Jan 2009 210.1

Dec 2009 218.0Open the xls file, select Table 36, look at cells D90 and D91

1 -

Thanks @polymaff, I had just downloaded the data sets and saw how you got your figures. Now I need to get my head round what it actually means.polymaff said:RG2015 said:

I have just looked at the ONS website, and cannot see either of the figures you have quoted. Am I missing something? If you wish you can reply on a new thread to avoid digressing too much on this one.polymaff said:EDIT: BTW, the "RPI for 2009" started at 214.8 and ended at 213.7. You're not alone in quoting a figure derived from the division of two RPIs as being, itself, "RPI". This misdescription makes the understanding of RPI data by the public (even) more difficult.RPI

Dec 2008 212.9

Jan 2009 210.1

Dec 2009 218.0Open the xls file, select Table 36, look at cells D90 and D910 -

Don't feel alone. NS&I had the calculating algorithm in the terms and conditions for inflation-linked certificates wrong for many years. Basically, they didn't understand that addition and subtraction is not the same as multiplication and division. Very difficult for them to get their heads around the fact that the RPI is always positive so the ratio of two RPIs will always be positive. Yes, if you subtract two RPIs you might have a negative result - but NEVER if you divide them.That is the degree of innumeracy at NS&I. Not much different at the BBC and in the newspapers.1

-

Where did the best available regular savings thread go?

") 8

8 -

Two amendments:Special_Saver2 said:

Stafford Railway BS Regular Saver (Issue 1)

Interest rate: 1% gross p.a. variable from 1st May 2020

Monthly payment: £20-£500

Miss any payments: Yes, as long as you do not miss payments three payments in one Society year (I am not sure what a Society year is!)

Penalty-free withdrawals: Yes, you can make three withdrawals per Society year

Age of applicant: Age not stated

How to open account: Branch or post

Special conditions: Maximum balance £100,000. Deposits to this account must come from your nominated bank account via standing order. Locals only (indicated near the top of the page under "Availability" - you must live within one of the following postcodes (ST14, ST15, ST16, ST17, ST18, ST19, ST20, ST21 and WS7, WS11, WS12, WS13, WS15).

4 withdrawals not 3 permitted per society year;

Society year ends 31 October0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards