We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

London Capital and Finance

Comments

-

Do not necessarily agree with the Damn lies as the 11 companies stated in the LCF April 2017 accounts as there were only 5 for the previous ( stated in the last accounts) year where the other 6 were formed prior to the accounts being made up to 30 April 2017s.

The 11 companies as of 30 April 2017 is on the record at Companies House. Administrators have confirmed only 12 companies now so the average loan has jumped from £5 million to £19 million per company since 2017 as the bonds increased from £60m to £236mRemember the saying: if it looks too good to be true it almost certainly is.0 -

I asked 2 years back visiting ther Eastbourne office the question on the loan side as the focus was on selling. I was told it was all done by brokers an< I queried if the bonds were not matched with loans there woukd be no interst earned I was told the demand for loans was much greater than that of incoming bonds nd there was a waiting list. Clearly lied to and stupidly I invested. Later they provided a loan brochure but no longer have it and tried applying for a loan but no response then started getting concerned especially then reading this forum but it was too late. In Hind sight had I challenged them back then for a refund what obstacles would I have hitThere is the blatant discrepancy of the frequent update on the LCF website of the number of commercial loans reaching approx 800 I recall. When asked about loans LCF directors and the contracted Surge staff said when the monies returned as short term loans fell due they were quickly relent. A lot of work for the illusive lending team. It was repeatedly emphasised that re the LCF bonds LCF was a direct lender not a broker, although it turns out they were a wholesale lender and were not lending directly to hundreds of SME businesses as the LCF website commercial lending statements led readers to believe. The Accounts Return 2017 said eleven, a lot less. Borrowers' terms included no re lending of loaned monies. LCF membership of the National Association of Loan Brokers was cancelled as it was a direct lender not a broker.0 -

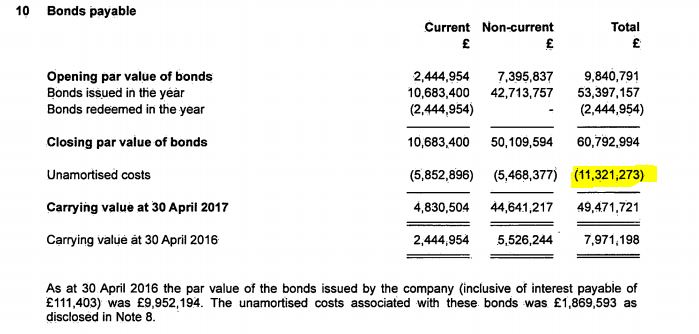

It would be useful for any feedback on this item in the LCF accounts for 2017. Does this prove that they were paying nearly 25% of the bonds value as setup costs and commission?

Plus a separate item for amortised costs of £3.9 million so total of £15.2 million for £60.7 million of bonds.

This cost for commission and setting up bonds equates to 25% of the £60.7 million of bonds issued.Remember the saying: if it looks too good to be true it almost certainly is.0 -

Isn't underwriting loans a regulated activity?0

-

Do you include FB group admin who have been in touch and feedback from that

I agree with you, nothing between official announcements but then should investors be able to phone, occasional, concise announcements makes things clearer0 -

Probably not. I think we were misinterpreting the term in earlier discussion.Botheredin wrote: »Isn't underwriting loans a regulated activity?

Underwriting does not mean the same as it does in the insurance industry - where an underwriter offers a guarantee.

Loan underwriters are just lenders who have made a commitment to put their money into a loan to fill it while other lenders are found to take their place. They would not need to be FCA authorised providing they were underwriting loans made by an authorised firm such as LCF.

Presumably, Surge was underwriting LCF loans to give legitimacy to the payments it received. I doubt much of its money was tied up in the loans and of course it was only invested temporarily and replaced with bondholder money as quickly as possible.0 -

Did you mean to say "comments ought not to be ambiguous"? I am bothered by the school boy excuses which are emerging as a result of phone calls to the administration team such as needing a finance manager to help with accounting and how they were just about to a point somebody before they got caught0

-

Catrina777 wrote: »Do you include FB group admin who have been in touch and feedback from that

I agree with you, nothing between official announcements but then should investors be able to phone, occasional, concise announcements makes things clearer

No, you misunderstand me. The comments should be ambiguous. They should not be doing interviews. They should not be hopping on to conference calls with people who run facebook groups. They should not be reassuring people.Catrina777 wrote: »Did you mean to say "comments ought not to be ambiguous"? I am bothered by the school boy excuses which are emerging as a result of phone calls to the administration team such as needing a finance manager to help with accounting and how they were just about to a point somebody before they got caught

This is a very serious matter. People have life changing amounts of money riding on the outcome of this administration. It is not a time for mucking around and telling people what they "hope" will happen. Finbarr O'Connell will be charging £500+ per hour for the PR work he has been doing and bondholders will be paying for it.

A good administrator would say nothing more than that it is too early to comment on the likely outcome for bondholders. They would not be doing interviews, and they would not be arranging private discussions with creditors. They would accept questions from bondholders, but answer these in the form of an FAQ sent to all known creditors.

They would seek to keep such activities to a minimum so that their focus is on more important tasks such as investigating the status of bondholders, their rights, and where their money has gone, investigating borrowing the companies, tracing and securing assets, and determining whether the LCF directors acted in the best interests of bondholders.

But I agree with you about the sympathetic tone towards LCF and the excuses being made for them. It wouldn't surprise me if at some point they suggest everything would have been ok if it wasn't for the FCA interfering - they've all but said it already.0 -

It would be useful for any feedback on this item in the LCF accounts for 2017. Does this prove that they were paying nearly 25% of the bonds value as setup costs and commission?

Plus a separate item for amortised costs of £3.9 million so total of £15.2 million for £60.7 million of bonds.

This cost for commission and setting up bonds equates to 25% of the £60.7 million of bonds issued.

Sorry don't know how to insert with this URL so typing it

From page 18 item 7 of 2017 accounts

Opening par value of loans 9,312,978

addition 50,392,963

Repaid Loans 488,500

Loans written off 418,802

Closing value of loans 58,798,639

From Page 15 item 2 Revenue

Loan interest receivable 2,825,094

Amortisation of loan 3,913,803

Arrangement fees 1,083,667

Bank Interest

Total revenue 7,822,771.

Reading the accounts at face value and glad I am not an accountant

Q1 So the closing value of the Bonds 60,792,994 is not that far short of the closing balance of the loans 58,798,639. So if you loaned out 58,8 million how does this SURGING 11,321,273 figure enter the equation if its a shortfall

Q2 There does not appear to be any mention of regular loan drawdown payments. So does this imply interest only.

Q2, The arrangement fee and Amortisation fee Page 15 indicates its been paid back by the borrower or am I mistaken.

Q3. Page 23 item 17 states cash GENERATED from Operations but can anybody clarify this 33,974.283 million figure (the starting point figure on page 10)

Q4, LCF have had no defaults WHATABOUT the 418,802 written off???0 -

In my previous life:o I came across several, shall we call them 'tame' administrators.

Obviously, in no way am I suggesting that is the case with LCF's administrators.

https://www.bbc.co.uk/news/business-11514708

Has anyone considered:

https://www.gov.uk/government/publications/reporting-misconduct-by-companies-directors-and-bankrupts-to-the-insolvency-service/reporting-misconduct-by-companies-directors-and-bankrupts-to-the-insolvency-service

or

https://www.gov.uk/complain-about-insolvency-practitioner

though complaint has to be made to authorising body first0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards