We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

London Capital and Finance

Comments

-

Thanks Masonic, that was very helpful.0

-

A few more statements from the administrators that seem to be at odds with other information.

https://damn-lies-and-statistics.blogspot.com/2019/02/lcf-administrators-new-claims.html

Interesting claim that the issue with LCF accounts was due to the lack of a finance director.Remember the saying: if it looks too good to be true it almost certainly is.0 -

I smell a rat.A few more statements from the administrators that seem to be at odds with other information.

https://damn-lies-and-statistics.blogspot.com/2019/02/lcf-administrators-new-claims.html

Interesting claim that the issue with LCF accounts was due to the lack of a finance director.

"land holds its value very well", but valuations on land for a property development loan are rarely based on the value of the land itself. These developments usually become worth less when building commences, those sitting as land with planning lose value as the clock ticks down on expiry of planning permission, those without planning usually carry hope value that planning permission can be obtained.

I've seen some frightening losses from loans secured on land, such that I would never invest in such loans. Neither would I invest in property developments, where I have been badly burned.

If these loans were underwritten by Surge, then there would be some documentary evidence of the fact, which appears not to be the case. Even if true, a company whose assets consisted almost entirely of cash at bank at the time of its last accounts, and no charges registered, is probably not going to be good for the money if it were ever to be held liable. Why was this important layer of additional protection not mentioned at all when LCF was telling potential bondholders how safe these loans were?

On the comments around the formation of a creditor committee, the standard practice is for the administrators to request nominations after releasing their proposals (~6 weeks after appointment). If more than 5 creditors are nominated, then there would be a vote, weighted by the value of each creditor's total claim.0 -

I smell a rat.

"land holds its value very well", but valuations on land for a property development loan are rarely based on the value of the land itself. These developments usually become worth less when building commences, those sitting as land with planning lose value as the clock ticks down on expiry of planning permission, those without planning usually carry hope value that planning permission can be obtained.

I completely agree. There is a suggestion that land purchased by companies lent money by LCF was seriously overvalued when purchased from linked individuals so they were essentially able to extract money from that company and ultimately from LCF. I've no idea if this is true but based on the information on the companies that is public it could certainly make sense.

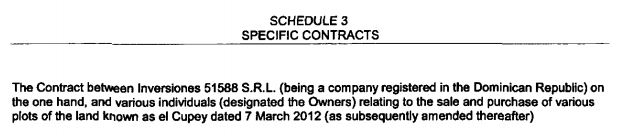

This is the security for one loan that LCF made:

It's not even ownership of the land itself. Another security was loans made by an LCF borrower. If those loans fail the security disappears for both companies. Remember the saying: if it looks too good to be true it almost certainly is.0

Remember the saying: if it looks too good to be true it almost certainly is.0 -

If these loans were underwritten by Surge, then there would be some documentary evidence of the fact, which appears not to be the case. Even if true, a company whose assets consisted almost entirely of cash at bank at the time of its last accounts, and no charges registered, is probably not going to be good for the money if it were ever to be held liable. Why was this important layer of additional protection not mentioned at all when LCF was telling potential bondholders how safe these loans were?

Since the LCF bond first issue in 2015 LCF directors, staff and Surge staff were repeatedly asked, as part of LCF commercial due diligence, for evidence of underwriting of the commercial loans re the secured assets. There was a complete lack of response either through unwillingness to comply and or lack of information to the extent that the conclusion was that no underwriters had been contracted or employed by LCF to verify asset value re LCF commercial borrowers.0 -

Re Jim James earlier post

Ehttps://damn-lies-and-statistics.blogspot.com/2019/02/lcf-administrators-new-claims.html

Do not necessarily agree with the Damn lies as the 11 companies stated in the LCF April 2017 accounts as there were only 5 for the previous ( stated in the last accounts) year where the other 6 were formed prior to the accounts being made up to 30 April 2017 as filed in companies house "OR" LCF topped up the existing 5 or left all the bond money idle for almost a year and loaned it at the 11th hour to the last 6, I don't know how to determine when m oney was paid into each of these initial 5 companies or further top up payments made from April 2016 to April 2017 but recall the bond money in 2016 being about 6 million in April 2016 to about 60million in April 2017 less the SURGE payment identified by Jim James.0 -

Finbarr's comments are so ambiguous are there others out there who would agree with the guy who posted the YouTube about the property he bought abroad and got no redress0

-

There is the blatant discrepancy of the frequent update on the LCF website of the number of commercial loans reaching approx 800 I recall. When asked about loans LCF directors and the contracted Surge staff said when the monies returned as short term loans fell due they were quickly relent. A lot of work for the illusive lending team. It was repeatedly emphasised that re the LCF bonds LCF was a direct lender not a broker, although it turns out they were a wholesale lender and were not lending directly to hundreds of SME businesses as the LCF website commercial lending statements led readers to believe. The Accounts Return 2017 said eleven, a lot less. Borrowers' terms included no re lending of loaned monies. LCF membership of the National Association of Loan Brokers was cancelled as it was a direct lender not a broker.0

-

Given the ambiguous nature of many of finbarr's comments since the administrators took over, are there others out there who have concerns about this particular administration following on from the YouTube video posted earlier?0

-

What you want is for an administrator to keep quiet and get on with the task at hand. Comments ought to be ambiguous, to the point of revealing little or nothing about the nascent process. I'd say we've seen the opposite, which is why I'd have concerns. It is quite unprofessional to speculate about matters that are the subject of ongoing investigations.Catrina777 wrote: »Given the ambiguous nature of many of finbarr's comments since the administrators took over, are there others out there who have concerns about this particular administration following on from the YouTube video posted earlier?

We've also seen certain creditors be given privileged information that ought either to have been communicated to all creditors, or kept under wraps.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards