We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Cash ISAs: The Best Currently Available List

Comments

-

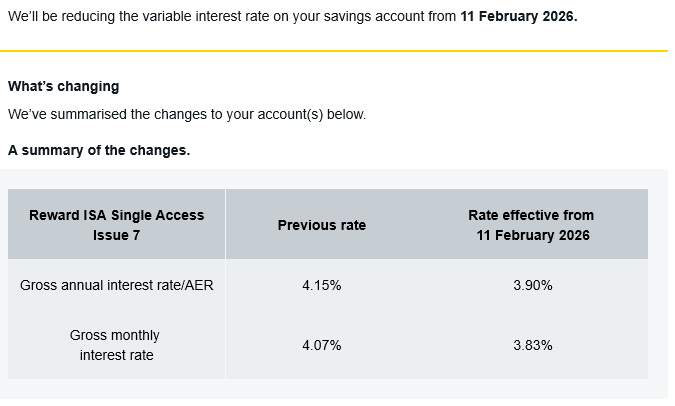

I can't see any actual figures anywhere...does beg the question of, does the requirement to notify rate reductions to customers in advance include having to publish the new rate with the advance notification or not?Growingold said:Vida Savings Defined Access ISA (issue 3) - 4.11% Banner on account saying interest rate reducing on 29/01/26.

I have had no notification. Does anyone have any idea what it is reducing to please. Many thanks2 -

I too haven't received any rate reduction notifications for either my isa or general savings account with them. My isa is a NLA issue 1.2

-

Yes I have ISA Iss 1 and ISA Iss 3. I have messaged them but haven't heard back yet.1spiral said:I too haven't received any rate reduction notifications for either my isa or general savings account with them. My isa is a NLA issue 1.1 -

Regarding individuals not receiving personal notifications, that is not unusual…what do the T&Cs say about how rate changes will be notified?

0 -

"If we decrease the interest rate, we’ll notify you at least 14 days ahead of the change. See the Savings T&C for more information."

0 -

Chaps, 4 posts now with no mention of which product is being discussed - helps if you just stick the name at the top of your post (or quote a post where it's mentioned).

14 -

The same one that was last mentioned...

0 -

…which is on a previous page

0 -

Aldermore

I just moved from Cynergy at 4.05% to Aldermore for the 4.15% and kept a pound in Cynergy just in case. They now luanched a 4.10% ISA, which I opned and made an internal transfer to materialise the accrued interest and now Aldermore is reducing rates. Quite dispapointing and now having to move back I guess.

1 -

Surely that's always going to happen with a variable rate isa.

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards