We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

New £12,000 limit on Cash ISA

Comments

-

Is that allowed to be bought, or allowed to be held? For instance if a gilt maturing in 6 years was bought, could it be held to maturity or would it have to be sold after a year?wmb194 said:

The pre-2014 Isa rules were that gilts and corporate bonds with at least 5 years to redemption were allowed.zagfles said:

Be interesting to see whether gilts will be allowed - if not it'll be rough on those who've built a gilts ladder in an ISA.wmb194 said:

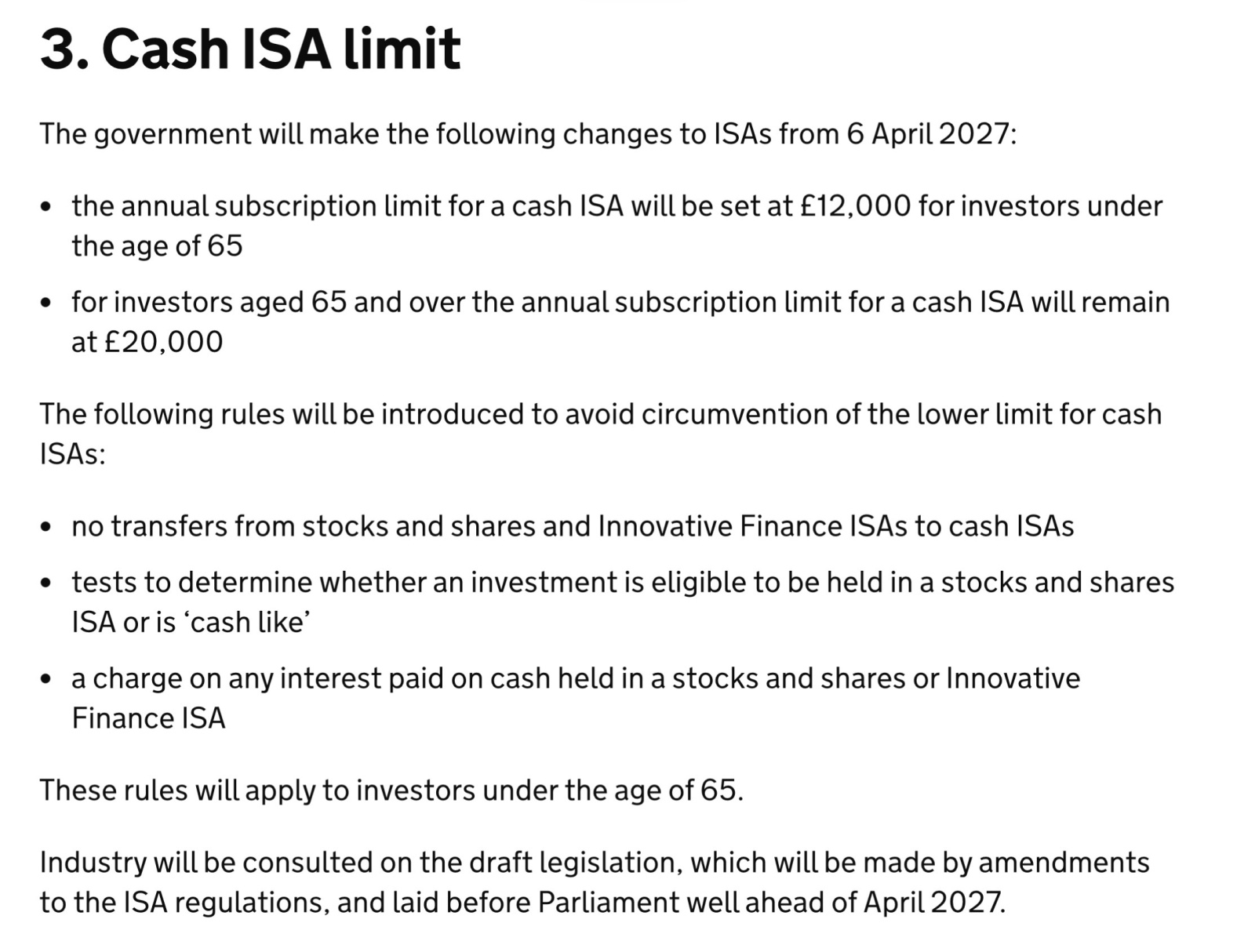

The link to this: https://www.gov.uk/government/publications/tax-free-savings-newsletter-19/tax-free-savings-newsletter-19-november-2025Time2Go_25 said:The following rules will be introduced to avoid circumvention of the lower limit for cash ISAs:

- no transfers from stocks and shares and Innovative Finance ISAs to cash ISAs

- tests to determine whether an investment is eligible to be held in a stocks and shares ISA or is ‘cash like’

- a charge on any interest paid on cash held in a stocks and shares or Innovative Finance ISA

Also some people will have been feeding the full ISA allowance into a S&S ISA for years and maybe have structured it to say 50% "cash like" and 50% equities, and it seems they'll now be forced to either remove/sell the "cash like" element or pay tax on it. Whereas if they'd been investing half in a cash ISA and half in a pure equity S&S ISA they'd be fine.

They really should allow existing ISAs to remain under current rules, they could easily do this by saying the new rules only apply to ISAs that have been contributed to from 2027.

If we're lucky we'll be allowed to keep anything that's newly disallowed and just restricted from buying additional.1 -

I could not agree more! Presumably it has all come about as a result of ‘intensive discussions’ between the Chancellor of the Exchequer and those she works with on a regular basis in the Treasury, with the overall objective being to appear on the surface to be ‘encouraging’ (in reality, forcing) under 65s to invest 40% of their annual ISA allowance whilst knowing full well that once a significant proportion of under 65s realise that all cash-like investments (i.e. some of the least riskiest) will effectively be taxed they will be even less inclined to invest the remaining £8k of their allowance than they already would be when they’re being forced to do so in this way!thunderroad88 said:This whole thread just reinforces what a dumb and ill thought through idea the whole thing is … to me anyway

Thus these naturally cautious under 65s will probably end up leaving the remaining £8k in taxable savings accounts where they will now be subjected to up to a 10% increase in tax on their interest under the new 22%, 42%, 47% rates for savings interest for basic, higher & additional rate taxpayers respectively! It really is stealth taxation at its very worst and it will be extremely unpopular imo!

If the government really wanted to encourage young and middle aged people to invest a significant proportion of their annual ISA allowance, surely the best way to do this is to leave the ISA allowance exactly as it is now - with every saver / investor having complete freedom within the £20k limit to save and/or invest in the proportions that they are personally most comfortable with - whilst at the same time, through a public advertising campaign, strongly encouraging the real, tangible potential benefits of investing rather than saving to both the individual investor and the range of businesses, companies etc. that are being invested in, in a typical moderately cautious to moderately adventurous mixed investment portfolio!5 -

Almost all economic goals can be achieved with either a stick or a carrot. Unfortunately the carrots appear to have disappeared.

The beatings will continue until morale improves.8 -

MMFs could be sold and held as cash instead - and transferred to a cash ISA in the next 18 months. They're effectively cash anyway, which is why until this afternoon all the geniuses were telling us that they were going to get round the new rules by investing in money market funds within S&S ISAs.zagfles said:

Where would gilts, MMFs etc go?Aretnap said:

Well, they'll have 18 months to transfer the 50% from a S&S ISA to a cash ISA if they want to. So a bit of minor hassle but hardly a disaster if they're reasonably aware of what's happening (which they should really be, if they're savvy enough to set up an investment structure like that).zagfles said:

Also some people will have been feeding the full ISA allowance into a S&S ISA for years and maybe have structured it to say 50% "cash like" and 50% equities, and it seems they'll now be forced to either remove/sell the "cash like" element or pay tax on it. Whereas if they'd been investing half in a cash ISA and half in a pure equity S&S ISA they'd be fine.wmb194 said:

The link to this: https://www.gov.uk/government/publications/tax-free-savings-newsletter-19/tax-free-savings-newsletter-19-november-2025Time2Go_25 said:The following rules will be introduced to avoid circumvention of the lower limit for cash ISAs:

- no transfers from stocks and shares and Innovative Finance ISAs to cash ISAs

- tests to determine whether an investment is eligible to be held in a stocks and shares ISA or is ‘cash like’

- a charge on any interest paid on cash held in a stocks and shares or Innovative Finance ISA

Gilts, dunno, we'll have to see the finer detail on whether they can be held to maturity. Though if you have gilts with only a couple of years to run they're also effectively cash anyway at this point, so you might as well sell them and transfer to a cash ISA if that's your wont.0 -

Situation: Govt needs £££, savers want interest, Govt thinks investing earns more £££ than saving

Solution: Govt should issue savings products with attractive interest rates and then use that deposits cash to invest themselves and earn the more £££

What am I missing?3 -

intalex said:Situation: Govt needs £££, savers want interest, Govt thinks investing earns more £££ than saving

Solution: Govt should issue savings products with attractive interest rates and then use that deposits cash to invest themselves and earn the more £££

What am I missing?Wasn't there a scheme where people could see their money put towards large infrastructure products through NS&I?The problem with the bit in bold is that I don't think many people would want to lock their money up at a fixed rate for 20 years, and such a practice might be considered exploitative.1 -

Held to maturity, the test was at purchase.zagfles said:

Is that allowed to be bought, or allowed to be held? For instance if a gilt maturing in 6 years was bought, could it be held to maturity or would it have to be sold after a year?wmb194 said:

The pre-2014 Isa rules were that gilts and corporate bonds with at least 5 years to redemption were allowed.zagfles said:

Be interesting to see whether gilts will be allowed - if not it'll be rough on those who've built a gilts ladder in an ISA.wmb194 said:

The link to this: https://www.gov.uk/government/publications/tax-free-savings-newsletter-19/tax-free-savings-newsletter-19-november-2025Time2Go_25 said:The following rules will be introduced to avoid circumvention of the lower limit for cash ISAs:

- no transfers from stocks and shares and Innovative Finance ISAs to cash ISAs

- tests to determine whether an investment is eligible to be held in a stocks and shares ISA or is ‘cash like’

- a charge on any interest paid on cash held in a stocks and shares or Innovative Finance ISA

Also some people will have been feeding the full ISA allowance into a S&S ISA for years and maybe have structured it to say 50% "cash like" and 50% equities, and it seems they'll now be forced to either remove/sell the "cash like" element or pay tax on it. Whereas if they'd been investing half in a cash ISA and half in a pure equity S&S ISA they'd be fine.

They really should allow existing ISAs to remain under current rules, they could easily do this by saying the new rules only apply to ISAs that have been contributed to from 2027.

If we're lucky we'll be allowed to keep anything that's newly disallowed and just restricted from buying additional.

I'm finding it hard to find documentation from back then but the things I can find say nothing about needing to sell, just the five year and 5% test. 2

2 -

I think you might just have invented gilts. Or NS&I for that matter.intalex said:Situation: Govt needs £££, savers want interest, Govt thinks investing earns more £££ than saving

Solution: Govt should issue savings products with attractive interest rates and then use that deposits cash to invest themselves and earn the more £££

What am I missing?4 -

The point is it's quite clear all rates were planned to be raised 2% and they backed away on income tax after feedback on the supposed leaks.NorthYorkie said:

No, the 2 percentage point addition is being made to the tax rate on non-ISA interest.hoc said:The government ditched the 2% addition to income tax at the last minute so we have an increasingly complicated scheme of values. In modern speak it is bound to be 'simplified' in the next year. LISA elimination will be the first step. Then the dominoes fall.1 -

Aretnap said:

I think you might just have invented gilts. Or NS&I for that matter.intalex said:Situation: Govt needs £££, savers want interest, Govt thinks investing earns more £££ than saving

Solution: Govt should issue savings products with attractive interest rates and then use that deposits cash to invest themselves and earn the more £££

What am I missing?

At one time the Government (NS&I) issued index linked (RPI) savings certificates, with the interest income-tax free. They've not been available since 2010 because (I presume) they were too popular.

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards