We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

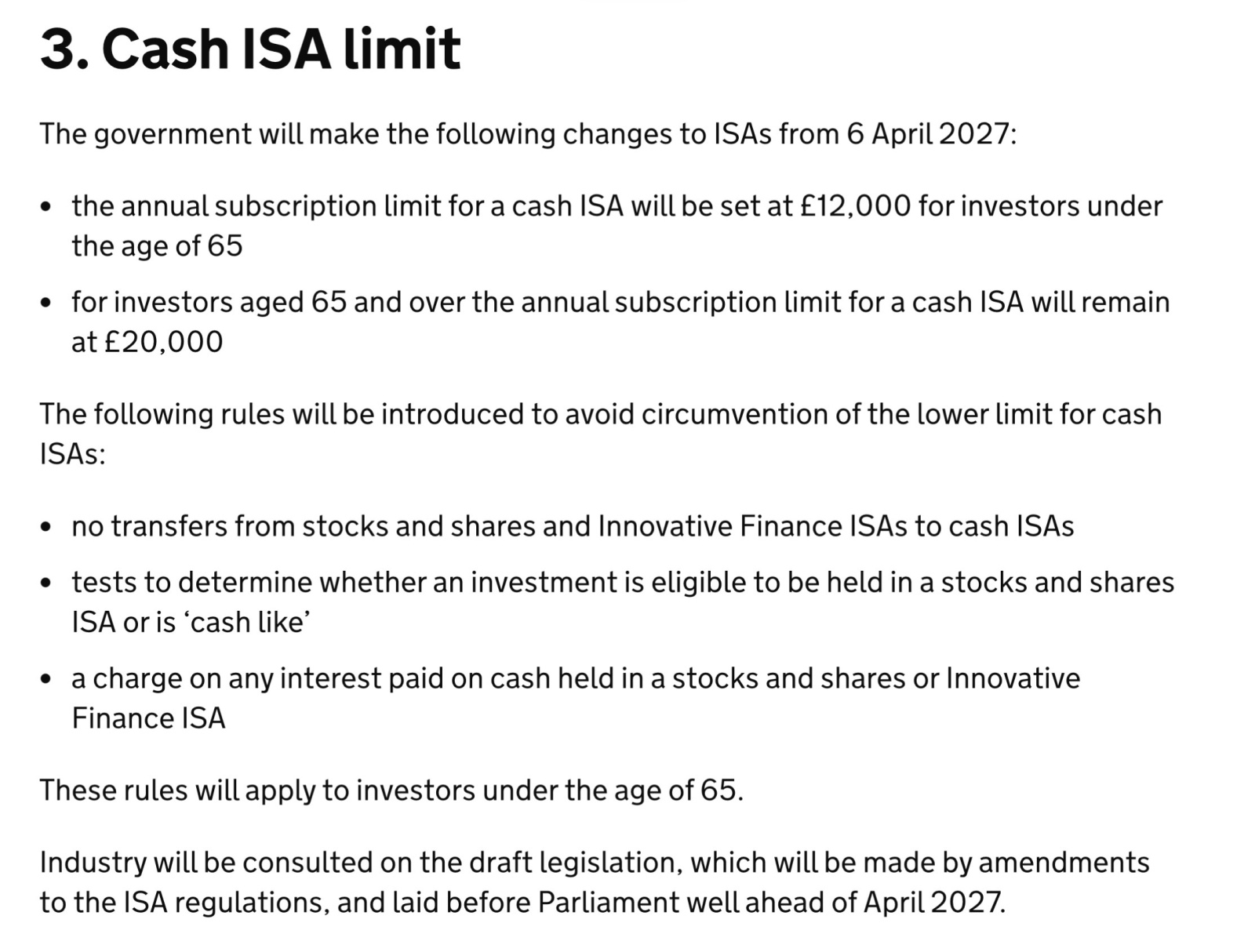

New £12,000 limit on Cash ISA

Comments

-

An outright ban on S&S transfers might have unintended consequences of course - someone who has to date been doing £20k S&S content that they could transfer to cash should that become necessary later might decide that they'd best do the £12k/£8k split, as they have no way of getting that £12k into a Cash ISA later.5

-

trickydicky14 said:

If restrictions are put in place to stop money in S&S being moved to cash ISA's what happens to those who correctly wish to de-risk later in life and move money into safer accounts. These are people who are not out to use a loophole but people who may have invested for years.MA260 said:You would expect restrictions on transfers between Cash and S&S ISA's otherwise people would just put money in S&S ISA and transfer to Cash. If the aim of the change is not to raise tax revenue but to encourage people to invest then you would expect them to leave things broadly as they are as they are halfway to getting someone to invest if they open a S&S ISA and put 8K in it. They are not going to get a great deal of tax revenue on 8K sitting in a ISA.For those who wish to gradually de-risk, someone with a £600k S&S ISA pot could transfer 2% of their pot into a cash ISA each tax year under the proposed rules. In addition they could add an unlimited amount to bonds within their S&S ISA. At the age of 65, they could transfer as much as they like from S&S to cash ISA.None of this affects what you can do within your pensions, which are the better place to hold low risk assets and the best source of funds for an annuity at retirement.3 -

No, the 2 percentage point addition is being made to the tax rate on non-ISA interest.hoc said:The government ditched the 2% addition to income tax at the last minute so we have an increasingly complicated scheme of values. In modern speak it is bound to be 'simplified' in the next year. LISA elimination will be the first step. Then the dominoes fall.1 -

The following rules will be introduced to avoid circumvention of the lower limit for cash ISAs:

- no transfers from stocks and shares and Innovative Finance ISAs to cash ISAs

- tests to determine whether an investment is eligible to be held in a stocks and shares ISA or is ‘cash like’

- a charge on any interest paid on cash held in a stocks and shares or Innovative Finance ISA

4 -

The link to this: https://www.gov.uk/government/publications/tax-free-savings-newsletter-19/tax-free-savings-newsletter-19-november-2025Time2Go_25 said:The following rules will be introduced to avoid circumvention of the lower limit for cash ISAs:

- no transfers from stocks and shares and Innovative Finance ISAs to cash ISAs

- tests to determine whether an investment is eligible to be held in a stocks and shares ISA or is ‘cash like’

- a charge on any interest paid on cash held in a stocks and shares or Innovative Finance ISA

5

5 -

Time2Go_25 said:

The following rules will be introduced to avoid circumvention of the lower limit for cash ISAs:

- no transfers from stocks and shares and Innovative Finance ISAs to cash ISAs

- tests to determine whether an investment is eligible to be held in a stocks and shares ISA or is ‘cash like’

- a charge on any interest paid on cash held in a stocks and shares or Innovative Finance ISA

Source?Only the first one seems relevant. No idea why a charge would be considered any way of preventing circumvention of a lower limit - quite the opposite it's more likely to drive people to hold cash-like investments (e.g. MMF) in a S&S ISA.0 -

That would fall foul of the second point.InvesterJones said:Time2Go_25 said:The following rules will be introduced to avoid circumvention of the lower limit for cash ISAs:

- no transfers from stocks and shares and Innovative Finance ISAs to cash ISAs

- tests to determine whether an investment is eligible to be held in a stocks and shares ISA or is ‘cash like’

- a charge on any interest paid on cash held in a stocks and shares or Innovative Finance ISA

Source?Only the first one seems relevant. No idea why a charge would be considered any way of preventing circumvention of a lower limit - quite the opposite it's more likely to drive people to hold cash-like investments (e.g. MMF) in a S&S ISA.2 -

UK GovernmentInvesterJones said:Time2Go_25 said:The following rules will be introduced to avoid circumvention of the lower limit for cash ISAs:

- no transfers from stocks and shares and Innovative Finance ISAs to cash ISAs

- tests to determine whether an investment is eligible to be held in a stocks and shares ISA or is ‘cash like’

- a charge on any interest paid on cash held in a stocks and shares or Innovative Finance ISA

Source?Only the first one seems relevant. No idea why a charge would be considered any way of preventing circumvention of a lower limit - quite the opposite it's more likely to drive people to hold cash-like investments (e.g. MMF) in a S&S ISA.1 -

InvesterJones said:Time2Go_25 said:

The following rules will be introduced to avoid circumvention of the lower limit for cash ISAs:

- no transfers from stocks and shares and Innovative Finance ISAs to cash ISAs

- tests to determine whether an investment is eligible to be held in a stocks and shares ISA or is ‘cash like’

- a charge on any interest paid on cash held in a stocks and shares or Innovative Finance ISA

Source?Only the first one seems relevant. No idea why a charge would be considered any way of preventing circumvention of a lower limit - quite the opposite it's more likely to drive people to hold cash-like investments (e.g. MMF) in a S&S ISA.In combination with the second point, that would not be possible. Ineligible investments cannot be held. The main question now is where will the line be drawn...Maybe they should allow cash-like investments to be held in a cash ISA. We have time to transfer in specie before the rules take effect. Perhaps it is time to write to our investment platforms ahead of the consultation.3 -

- a charge on any interest paid on cash held in a stocks and shares or Innovative Finance ISA

If confirmed that would be complex and absolutely disgusting. Holding cash in a shares isa is entirely normal & reasonable, and in fact unavoidable for at least a certain amount of time (between depositing and buying, or between selling and buying).

Are we now going to have to keep track of this & report it? One of the attractions of ISAs is no tax stuff to worry about keeping track of.

I recently transferred a fair chunk out of a cash ISA and into a shares ISA where it's currently in a MMF waiting to be invested. So I'm now going to be penalised for that and treated like a tax-dodger? Despite having paid a shed-load of tax every year for over 40 years and adhered to every rule there is.

8 - a charge on any interest paid on cash held in a stocks and shares or Innovative Finance ISA

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards