We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

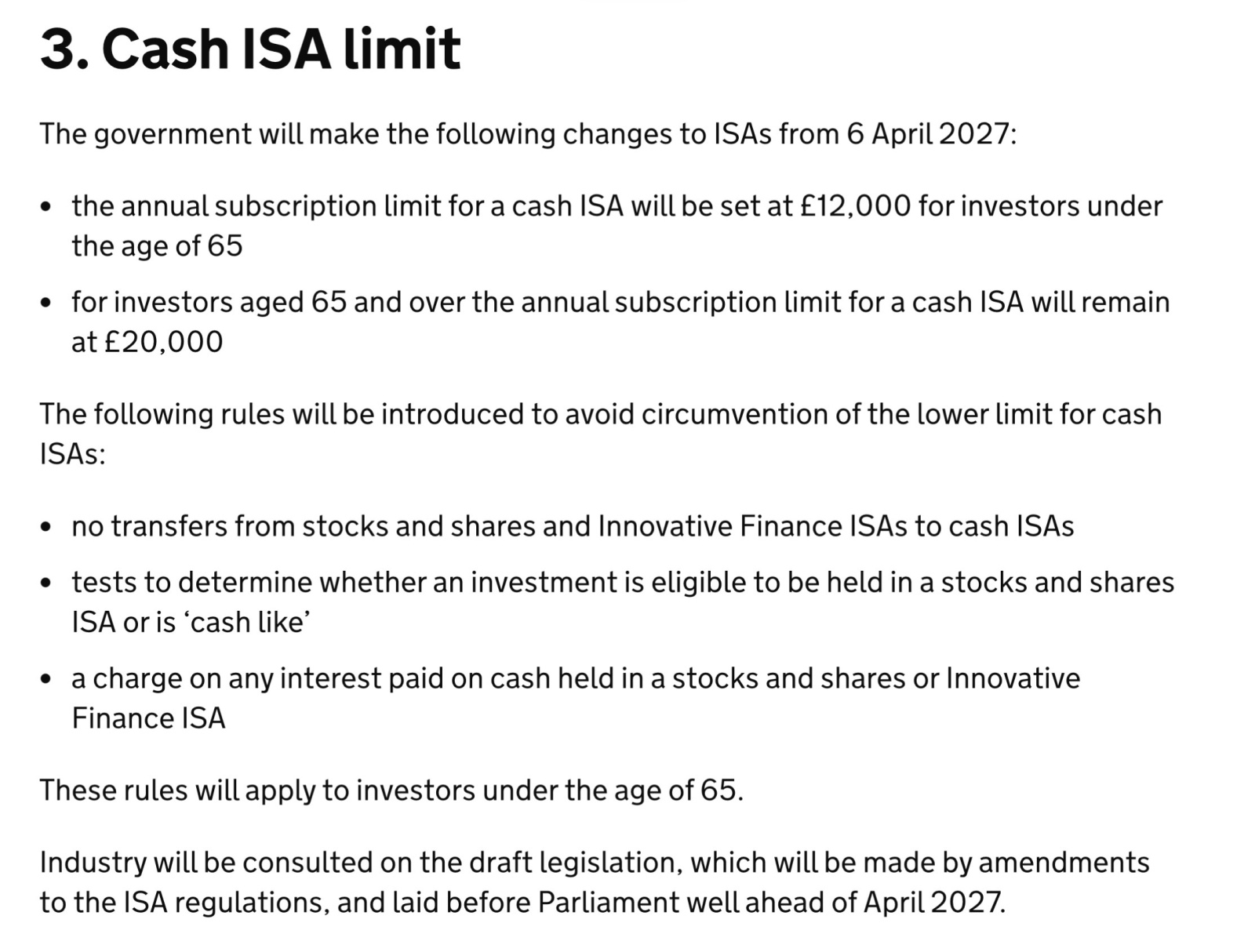

New £12,000 limit on Cash ISA

Comments

-

Gilts maturing many years in the future are not cash equivalents and nobody is talking about making them ISA ineligible. At most there is going to be some consultation over exactly what "many years in the future" will mean.MK62 said:

.......but what about gilts maturing many years in the future.......if they are no longer permitted ISA investments after 2027, you are looking at either having to sell prior to that (at potentially a large loss), or perhaps, if allowed, moving them in-specie to a GIA (so exposing the coupons to tax.....the avoidance of which was the very reason they were put into an ISA in the first place)......it would be a textbook example of moving the goalposts.Aretnap said:MK62 said:

Surely the government would not force people to sell investments which were compliant with the rules when purchased, but are suddenly no longer compliant with any new rules.......some could be looking at investment losses into the thousands.Aretnap said:

MMFs could be sold and held as cash instead - and transferred to a cash ISA in the next 18 months. They're effectively cash anyway, which is why until this afternoon all the geniuses were telling us that they were going to get round the new rules by investing in money market funds within S&S ISAs.zagfles said:

Where would gilts, MMFs etc go?Aretnap said:

Well, they'll have 18 months to transfer the 50% from a S&S ISA to a cash ISA if they want to. So a bit of minor hassle but hardly a disaster if they're reasonably aware of what's happening (which they should really be, if they're savvy enough to set up an investment structure like that).zagfles said:

Also some people will have been feeding the full ISA allowance into a S&S ISA for years and maybe have structured it to say 50% "cash like" and 50% equities, and it seems they'll now be forced to either remove/sell the "cash like" element or pay tax on it. Whereas if they'd been investing half in a cash ISA and half in a pure equity S&S ISA they'd be fine.wmb194 said:

The link to this: https://www.gov.uk/government/publications/tax-free-savings-newsletter-19/tax-free-savings-newsletter-19-november-2025Time2Go_25 said:The following rules will be introduced to avoid circumvention of the lower limit for cash ISAs:

- no transfers from stocks and shares and Innovative Finance ISAs to cash ISAs

- tests to determine whether an investment is eligible to be held in a stocks and shares ISA or is ‘cash like’

- a charge on any interest paid on cash held in a stocks and shares or Innovative Finance ISA

Gilts, dunno, we'll have to see the finer detail on whether they can be held to maturity. Though if you have gilts with only a couple of years to run they're also effectively cash anyway at this point, so you might as well sell them and transfer to a cash ISA if that's your wont.

Investment losses of thousands strikes me as rather melodramatic though. The whole point of cash-equivalent investments is that they are, well, equivalent to cash. They do not fluctuate significantly in value over time and there is little gain or loss by converting to cash a little earlier than you planned. Eg if you have a Gilt that you were planning to hold to maturity in a years' time, the difference between doing that and selling it now and putting the proceeds in a one year fixed cash account is going to be basically a transaction fee plus a rounding error.

Previously I believe it meant 5 years. The YTM on 5 year gilts is much the same as the interest rate on a best buy 5-year fixed savings account (no **** Sherlock!) - there's so no loss to the retail investor if they have to sell at that point. (Other than perhaps less favourable tax treatment - and not even that if you sell and transfer before April 2027).0 -

As far as I can see this changes the entire paradigm of using ISAs as a pension. Something many people do either instead of or in addition to traditional pensions.

Previously you could load up S&S ISAs & invest in shares, with the intention to de-risk later, possibly into MMFs, possibly by transferring to a cash ISA.

The changes being proposed remove that ability. Effectively once money is in an S&S ISA your only option will be to invest in high-risk assets (i.e. equities) forever, or withdraw the money from it's ISA wrapper.

This is going to completely wreck a lot of people's financial planning.

12 -

Several counterpoints:hallmark said:As far as I can see this changes the entire paradigm of using ISAs as a pension. Something many people do either instead of or in addition to traditional pensions.

Previously you could load up S&S ISAs & invest in shares, with the intention to de-risk later, possibly into MMFs, possibly by transferring to a cash ISA.

The changes being proposed remove that ability. Effectively once money is in an S&S ISA your only option will be to invest in high-risk assets (i.e. equities) forever, or withdraw the money from it's ISA wrapper.

This is going to completely wreck a lot of people's financial planning.

(1) You can still derisk within your S&S ISA by moving into low risk investments - just not zero risk investments. Medium to long dated gilts, corporate bond funds and the like will be fine.

(2) You can still move up to £12000 per year from a S&S ISA to a cash ISA by withdrawing and resubscribing

(3) When you're 65 you can derisk entirely by transferring to a cash ISA (or a money market fund)

(4) Moving all your investments into cash is not actually derisking entirely in any event - and certainly not something you should be doing at the tender age of 65.

(5) Having an ISA pot so large that a sensible de-risking strategy involved moving more than £12000 per year into cash savings before you are 65 would fall squarely into the category of "nice problems to have"; I'm sure that your retirement plans would survive paying some tax on cash savings interest.

2 -

hallmark said:As far as I can see this changes the entire paradigm of using ISAs as a pension. Something many people do either instead of or in addition to traditional pensions.

Previously you could load up S&S ISAs & invest in shares, with the intention to de-risk later, possibly into MMFs, possibly by transferring to a cash ISA.

The changes being proposed remove that ability. Effectively once money is in an S&S ISA your only option will be to invest in high-risk assets (i.e. equities) forever, or withdraw the money from it's ISA wrapper.

This is going to completely wreck a lot of people's financial planning.

The Government's actions show a complete lack of understanding of - or disregard for - how people use Investment ISAs as long term financial planning tools. They'll have no idea at all how this change will impact people wishing to de-risk or periodically rebalance asset allocations. We'll have to resort to various workarounds, with limited scope to do so. So disappointing.7 -

If you really want to use an ISA like a pension, then gilts and bonds would be the usual route, not cash/cash-like holdings. So I don't think this "wrecks" things. Plus, and I think this has been linked to and quoted in this thread already, what has been said is:hallmark said:As far as I can see this changes the entire paradigm of using ISAs as a pension. Something many people do either instead of or in addition to traditional pensions.

Previously you could load up S&S ISAs & invest in shares, with the intention to de-risk later, possibly into MMFs, possibly by transferring to a cash ISA.

The changes being proposed remove that ability. Effectively once money is in an S&S ISA your only option will be to invest in high-risk assets (i.e. equities) forever, or withdraw the money from it's ISA wrapper.

This is going to completely wreck a lot of people's financial planning.The following rules will be introduced to avoid circumvention of the lower limit for cash ISAs:

- no transfers from stocks and shares and Innovative Finance ISAs to cash ISAs

- tests to determine whether an investment is eligible to be held in a stocks and shares ISA or is ‘cash like’

- a charge on any interest paid on cash held in a stocks and shares or Innovative Finance ISA

These rules will apply to investors under the age of 65.

Tax-free savings newsletter 19 — November 2025 - GOV.UK

So that sounds like the intention is to allow people, once they get to a typical retirement age, to go all in on cash if they really want to. No, it doesn't help people retiring early, but there are actual pensions too - plus, once the actual rules are formed up, you get the time before 2027 to swap things around before it starts.

4 -

Also, even if you do have the good fortune to retire before 65, going all in on cash in your 50s or early 60s would be an even sillier thing to do than going all in on cash at 65.EthicsGradient said:

If you really want to use an ISA like a pension, then gilts and bonds would be the usual route, not cash/cash-like holdings. So I don't think this "wrecks" things. Plus, and I think this has been linked to and quoted in this thread already, what has been said is:hallmark said:As far as I can see this changes the entire paradigm of using ISAs as a pension. Something many people do either instead of or in addition to traditional pensions.

Previously you could load up S&S ISAs & invest in shares, with the intention to de-risk later, possibly into MMFs, possibly by transferring to a cash ISA.

The changes being proposed remove that ability. Effectively once money is in an S&S ISA your only option will be to invest in high-risk assets (i.e. equities) forever, or withdraw the money from it's ISA wrapper.

This is going to completely wreck a lot of people's financial planning.The following rules will be introduced to avoid circumvention of the lower limit for cash ISAs:

- no transfers from stocks and shares and Innovative Finance ISAs to cash ISAs

- tests to determine whether an investment is eligible to be held in a stocks and shares ISA or is ‘cash like’

- a charge on any interest paid on cash held in a stocks and shares or Innovative Finance ISA

These rules will apply to investors under the age of 65.

Tax-free savings newsletter 19 — November 2025 - GOV.UK

So that sounds like the intention is to allow people, once they get to a typical retirement age, to go all in on cash if they really want to. No, it doesn't help people retiring early...

2 -

'Early' retirement isn't always as a result of "good fortune".Aretnap said:

Also, even if you do have the good fortune to retire before 65, going all in on cash in your 50s or early 60s would be an even sillier thing to do than going all in on cash at 65.EthicsGradient said:

...

And there are circumstances where going over to cash in your 50's or 60's is far from being a 'silly' thing to do.11 -

In reply to Aretnap & EthicsGradient you both make interesting points (I don't necessarily agree with all of them).

However virtually every tax measure is introduced in a milder form than what it turns into. The measures today are bad enough but as you say potentially might allow £12k into a cash ISA or more freedom of options at 65. But we all know that could change into far less than £12K & far older than 70 at the stroke of a pen. I think it's reasonable to say we have every reason to fear that might be the case.

ISAs were a bit sacrosanct before & chancellors were scared to make changes for the worse. Now that precedent has gone I fully expect other more draconian changes will follow.9 -

Judging by the endless ISA questions even the current simple rule of - max 20K new money per tax year into one or more ISAs - isn't well understood except by the few expert frequent posters here.

The new rule to cap cash ISAs at 12K is pointless, but worse it's spawning multiple new rules - like a 65 year age factor to overcome some objections - but not yet explained how it'll work - and more rules to overcome loopholes like no S&S to cash transfers - something possibly even worse than the original 12K limit idea.

The only good solution is to revert to the current simple rules where we can choose what to do with our money.7 -

Indeed…writing a manifesto in 2028 for Reform or the Tories (I discount any other party from having any serious chance) just got quite a bit easier this weeknewlease said:

Or how people are suddenly expecting the current lot to still be in power when these changes are planned to come into effect.thunderroad88 said:This whole thread just reinforces what a dumb and ill thought through idea the whole thing is … to me anyway5

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards