We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Being nosey... How many Regular Saver accounts do you have?

Comments

-

Now surprised to find I've got 17 after the Newcastle, Hanley and Principality xmas appeared. Plus couldn't resist getting a Zopa curr acc for the 7.1% RS. It's getting addictive. Monthly total £5950.1

-

Of my 21, I intend to fully fund each month: Saffron, Principality Issue 4, Monmouthshire App Exclusive, Progressive and Principality Christmas (as the 6.5% is fixed) at £1,700. For November, this will be funded from maturities that have occurred in October. Then fund the required amounts: £25 Hanley, £25 Stafford, £10 Coventry (Prize Draw) and £10 Market Harborough (although November will be the last for that one.) Any spare change will go into NatWest DRS. So 9 receiving some form of funding going forward, although I also expect to fully fund Hanley, Melton Adcock and Principality Healthy Habits (in the interests of ensuring sufficient funds for January and also I don’t have my Scottish BS details yet) from income in November. December maturities are bigger, so most of them will be fully funded then.

Monthly funding for me is therefore £1,770+ although that includes some that aren’t funded with new money and doesn’t count some that are.EDIT: Make that 10 receiving some form of funding - forgot Loughborough though the monthly contribution varies as it’s min £1.1 -

I've two RS accounts maturing in November and I've opened 4 more this month 3 of which mature next October so my plan of one RS maturing a month has definitely gone to pot!

For the benefit of the spreadsheet I currently have 9, which will be down to 7 in November, monthly total £1800.1 -

@Bobblehat

You can now legitimately add me to the league table. I am now responsible for two RS accounts with the N/Wide! Thanks for all your help.6 -

You're welcome! I hope it was all straightforwardluci said:@Bobblehat

You can now legitimately add me to the league table. I am now responsible for two RS accounts with the N/Wide! Thanks for all your help.")

You're on the table!

Compiler of the RS League Table.

Being nosey... How many Regular Saver accounts do you have? — MoneySavingExpert Forum1 -

Hi Bobbles, I like the update on the chart, there was one thing that made me smile, I noticed that there are a few entries with the partners added, what made me chuckle was if I added my missus, it would read as my username Plus the other half, sorry, its just my mind having a giggle with me.Corduroy pillows are making headlines! Back home in London now after 27years wait! Duvet know it's Christmas, not original, it's a cover.0

-

Oh! Matron! Could be cross between a "Carry On" and a "Confessions of" there, Arthur!arthurdick said:Hi Bobbles, I like the update on the chart, there was one thing that made me smile, I noticed that there are a few entries with the partners added, what made me chuckle was if I added my missus, it would read as my username Plus the other half, sorry, its just my mind having a giggle with me. Compiler of the RS League Table.

Being nosey... How many Regular Saver accounts do you have? — MoneySavingExpert Forum1 -

Yes, it was painless. I prefer to use the laptop for things like opening accounts, but I do like the N/Wide app so used that. I had to wait until the OH came home before I could open his, so we don't have almost consecutive account numbers like we usually do when opening accounts.Bobblehat said:

You're welcome! I hope it was all straightforwardluci said:@Bobblehat

You can now legitimately add me to the league table. I am now responsible for two RS accounts with the N/Wide! Thanks for all your help.

You're on the table!1 -

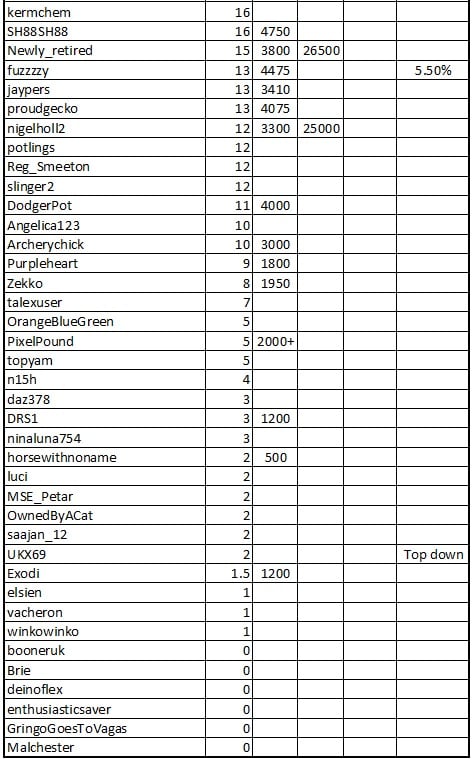

I guess a lot of members will have realised we have a new leader at 82 RS's

Excel1966 still holds the record (of those submitting figures) for a solo holding of 76 RS's. I wonder if there are still some shy high-roller Forumites out there that, for whatever reason, are keeping their figures close to their chest

I'll save the next published update until shortly after the 3rd Nov, as I expect a small flurry of updates between now and then.Compiler of the RS League Table.

Being nosey... How many Regular Saver accounts do you have? — MoneySavingExpert Forum1 -

Yes, 82 will take some beating!Bobblehat said:I guess a lot of members will have realised we have a new leader at 82 RS's

Excel1966 still holds the record (of those submitting figures) for a solo holding of 76 RS's. I wonder if there are still some shy high-roller Forumites out there that, for whatever reason, are keeping their figures close to their chest

I'll save the next published update until shortly after the 3rd Nov, as I expect a small flurry of updates between now and then.

I'll give you a proper update in the next few days, once a couple of Principality maturities are finalised, but it'll definitely be an increase on my total of accounts. Same monthly pay-in though.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards