We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Being nosey... How many Regular Saver accounts do you have?

Comments

-

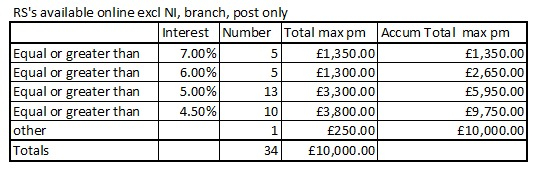

While King Bridlington1 was number bashing, I was also giving it a go too and came up with this using the King B's currently available page 1 listings

")

Roughly agreeing with Kim_13's results ...

I didn't need to go into the "Local/loyal/beta/new customer only" category as I hit the £10,000 with the open to all section. It's interesting to see that you can throw £5,950pm at the currently available greater than 5.00% RS's, which will beat most current unlimited Easy Access accounts.Compiler of the RS League Table.

https://forums.moneysavingexpert.com/discussion/6670416/how-many-regular-savers-do-you-have-the-league-table/p13 -

I've opened a Principality Christmas 2026 Regular Saver, so now on 8 total, with a monthly funding of £1,950.1

-

Worth mentioning that a lot of people in the league table will have Monmouthshire's 7% account, so we've got an extra £1000 going in at 7%. Hence why some people's monthly totals may seem rather high.Bobblehat said:While King Bridlington1 was number bashing, I was also giving it a go too and came up with this using the King B's currently available page 1 listings

Roughly agreeing with Kim_13's results ...

I didn't need to go into the "Local/loyal/beta/new customer only" category as I hit the £10,000 with the open to all section. It's interesting to see that you can throw £5,950pm at the currently available greater than 5.00% RS's, which will beat most current unlimited Easy Access accounts.

And of course other NLA accounts.3 -

I think you will find it's a lot more, I have around 44 RS now and pay in about 10k a month. Some folks have many more than that. A good handful allow you to put £500 to a £1000 in so 10k soon gets used up.20122013 said:Apologise if this has already been mentioned, I was wondering how much will be needed to fund the maximum allowed to all the RS which can be opened online (exclude the ones in Ireland, or need to be open at a branch / via post )? would it be about £10,000pcm or more? (Not looking for an exact figure as the product changes)I choose the rooms that I live in with care,

The windows are small and the walls almost bare,

There's only one bed and there's only one prayer;

I listen all night for your step on the stair.2 -

Also worth mentioning that I stopped counting once I added that last one to reach £10,000, so there are quite a few more RS's equal to or less than the 4.5% figure available to extend the £10,000 even furtherclairec666 said:

Worth mentioning that a lot of people in the league table will have Monmouthshire's 7% account, so we've got an extra £1000 going in at 7%. Hence why some people's monthly totals may seem rather high.Bobblehat said:While King Bridlington1 was number bashing, I was also giving it a go too and came up with this using the King B's currently available page 1 listings

Roughly agreeing with Kim_13's results ...

I didn't need to go into the "Local/loyal/beta/new customer only" category as I hit the £10,000 with the open to all section. It's interesting to see that you can throw £5,950pm at the currently available greater than 5.00% RS's, which will beat most current unlimited Easy Access accounts.

And of course other NLA accounts. Compiler of the RS League Table.

https://forums.moneysavingexpert.com/discussion/6670416/how-many-regular-savers-do-you-have-the-league-table/p11 -

Honorary "King of Regular Savers" ... a bit like Burger King ... but for money savers? I'll stop there!

Compiler of the RS League Table.

Compiler of the RS League Table.

https://forums.moneysavingexpert.com/discussion/6670416/how-many-regular-savers-do-you-have-the-league-table/p12 -

Presumably you haven't included multiple Principality accounts of the same issue

3

3 -

Given that the league table up-thread allows the total number of accounts held by a forumite and a spouse, then if you are over 55 with kids under 26 then even this exclusion fails! I guess if they were students in Bath it would help.Bridlington1 said:

First of all I couldn't claim the title of King Bridlington1, so far as I'm concerned there's only one person who should be given the title of King in this country and that's Charles III.Bobblehat said:While King Bridlington1 was number bashing, I was also giving it a go too and came up with this using the King B's currently available page 1 listings

Roughly agreeing with Kim_13's results ...

I didn't need to go into the "Local/loyal/beta/new customer only" category as I hit the £10,000 with the open to all section. It's interesting to see that you can throw £5,950pm at the currently available greater than 5.00% RS's, which will beat most current unlimited Easy Access accounts.

Some further figures of note, if you were to take a look at the regular savers landscape as a whole, the last time I published one of my regular savers snapshots (9/9/25) the sum of the max monthly deposits of all regular savers available (at any rate) at the time was £42,250.

The sum of the accounts that were NLA at that time but that people could still hold was £33,225.

If you then include the fact that some of these listings were for ``any issue", e.g. for Leeds BS and Chorley BS are separate issues (but taken as a whole in the listing) you'd gain a further £13,450 of deposits if I'm not mistaken.

This gives a combined max total monthly pay in of £88,925, this figure does not include children's regular savers. Note it's impossible to hold all of these regular savers simultaneously, not least because you'd need to be aged both over 55 and under 26 at the same time.1 -

Only went down to 6% because going lower would take longer 😂 Grouping them into categories in my post was part of the working, so that I then just had to total those up.20122013 said:Bridlington1 said:

First of all I couldn't claim the title of King Bridlington1, so far as I'm concerned there's only one person who should be given the title of King in this country and that's Charles III.Bobblehat said:While King Bridlington1 was number bashing, I was also giving it a go too and came up with this using the King B's currently available page 1 listings

Roughly agreeing with Kim_13's results ...

I didn't need to go into the "Local/loyal/beta/new customer only" category as I hit the £10,000 with the open to all section. It's interesting to see that you can throw £5,950pm at the currently available greater than 5.00% RS's, which will beat most current unlimited Easy Access accounts.

Some further figures of note, if you were to take a look at the regular savers landscape as a whole, the last time I published one of my regular savers snapshots (9/9/25) the sum of the max monthly deposits of all regular savers available (at any rate) at the time was £42,250.

The sum of the accounts that were NLA at that time but that people could still hold was £33,225.

If you then include the fact that some of these listings were for ``any issue", e.g. for Leeds BS and Chorley BS are separate issues (but taken as a whole in the listing) you'd gain a further £13,450 of deposits if I'm not mistaken.

This gives a combined max total monthly pay in of £88,925, this figure does not include children's regular savers. Note it's impossible to hold all of these regular savers simultaneously, not least because you'd need to be aged both over 55 and under 26 at the same time.

@Bridlington1 @Bobblehat @Kim_13 @clairec666 et alWhile I am still looking at all the RS listings to get the figures (even using the moneyfactscompare's list), you all have already worked out the totals. What did you so you got it done so much faster (than me), please? Interested to know as it will be most helpful.1 -

I ignored Moneyfacts and went straight to Bridlington1's page 1. I manually started at the top and typed in two columns for Interest and Max pm for each RS that met the criteria ... the rest was easy spreadsheet jiggery-pokery.Kim_13 said:

Only went down to 6% because going lower would take longer 😂 Grouping them into categories in my post was part of the working, so that I then just had to total those up.20122013 said:Bridlington1 said:

First of all I couldn't claim the title of King Bridlington1, so far as I'm concerned there's only one person who should be given the title of King in this country and that's Charles III.Bobblehat said:While King Bridlington1 was number bashing, I was also giving it a go too and came up with this using the King B's currently available page 1 listings

Roughly agreeing with Kim_13's results ...

I didn't need to go into the "Local/loyal/beta/new customer only" category as I hit the £10,000 with the open to all section. It's interesting to see that you can throw £5,950pm at the currently available greater than 5.00% RS's, which will beat most current unlimited Easy Access accounts.

Some further figures of note, if you were to take a look at the regular savers landscape as a whole, the last time I published one of my regular savers snapshots (9/9/25) the sum of the max monthly deposits of all regular savers available (at any rate) at the time was £42,250.

The sum of the accounts that were NLA at that time but that people could still hold was £33,225.

If you then include the fact that some of these listings were for ``any issue", e.g. for Leeds BS and Chorley BS are separate issues (but taken as a whole in the listing) you'd gain a further £13,450 of deposits if I'm not mistaken.

This gives a combined max total monthly pay in of £88,925, this figure does not include children's regular savers. Note it's impossible to hold all of these regular savers simultaneously, not least because you'd need to be aged both over 55 and under 26 at the same time.

@Bridlington1 @Bobblehat @Kim_13 @clairec666 et alWhile I am still looking at all the RS listings to get the figures (even using the moneyfactscompare's list), you all have already worked out the totals. What did you so you got it done so much faster (than me), please? Interested to know as it will be most helpful.Compiler of the RS League Table.

https://forums.moneysavingexpert.com/discussion/6670416/how-many-regular-savers-do-you-have-the-league-table/p11

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.3K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 248K Work, Benefits & Business

- 605.2K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards