We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Reeves' ISA review

Comments

-

Can this change be retrospective - taking into account existing investments? If there is a 'lifetime' cap - what happens to current investments above this?

Of course it was done for pensions when the lifetime allowance was cut massively a decade ago from £1.8m to £1.1m - albeit since abolished by Jeremy Hunt a couple of years ago.

So it can be done - even if it unfair.0 -

Anything is possible. If going down that road, the simplest option would probably be to abolish cash ISAs and turn them into normal savings accounts, then focus on relief through the Personal Savings Allowance.Rich2808 said:Can this change be retrospective - taking into account existing investments? If there is a 'lifetime' cap - what happens to current investments above this?

Of course it was done for pensions when the lifetime allowance was cut massively a decade ago from £1.8m to £1.1m - albeit since abolished by Jeremy Hunt a couple of years ago.

So it can be done - even if it unfair.0 -

It could apply to both, but the following arguments could also be made:friolento said:

Why would we need this warning just for cash ISAs but not for non-ISA savings accounts?SnowMan said:

Like that versionmasonic said:

Why not simply "even after the addition of tax free interest, the spending power of money saved in a cash ISA may decrease over time due to prices increasing".Albermarle said:

I think many will just see the words' get back considerably less' and misunderstand them ( wilfully in some cases)SnowMan said:It's been suggested that there should be a warning when you save in a cash ISA (like there is with investments) and I think that has some merit. Perhaps someone can improve on my attemptCash ISAs may (and often do) earn interest at less than the rate at which prices increases, and so you may get back considerably less than what you saved if you take into account what that money can buy.

I will have a go.

Cash ISAs and other savings account may (and often do) earn interest at less than the rate at which prices increase. This means that over time the value of your savings in terms of what they will buy, may slowly decrease.

- For those who don’t wish to get involved with something they don’t understand, i.e. investing, Regular Savers (being the loss leaders that they are) are more likely to result in the customer maintaining the purchasing power of their money.- Non-ISA savings are more likely to include funds that are held in cash appropriately - an emergency fund to avoid having to sell stocks and shares at a loss, or the little money that those in a less fortunate financial situation have managed to set aside.

- Now that we have the PSA, the majority of people pay no tax on their savings income, so ISAs are more likely to be used by those who have sufficient assets that they should be investing instead. With ISA rates often below the equivalent taxable accounts after tax, there can be a double loss made in opting for a Cash ISA (to inflation and also in not securing the best return possible on anything held in cash.)1 -

Not to fear further off-topic but there's a strong case that anti-smoking legislation has been incredibly beneficial for the established tobacco companies:subjecttocontract said:I see nothing wrong with putting a warning on cash ISAs but they put health warnings on cigarette packets and I'm not convinced that more than a tiny, tiny percentage of smokers stop as a result of that warning.- Near-impossible barrier to entry for new market players

- Plain packaging means limited ability for competitors to differentiate by "brand"

- Advertising restrictions means no marketing expenditure

- Import controls maintains stability of country/region-tiered pricing hierarchy

0 -

Returning the proportions back to what they were when ISAs were originally introduced (Total £7k, cash £3k, S&S £7k or £4k if cash used)george4064 said:Will be interesting to see what comes of this. Potentially restricting the amount of cash one can hold in an ISA or reducing the cash ISA allowance to just £4k.Remember the saying: if it looks too good to be true it almost certainly is.1 -

Original values adjusted for inflation would be fair enough, the Tories went far beyond that. That would be more like £6k cash rather than the rumoured £4k.jimjames said:

Returning the proportions back to what they were when ISAs were originally introduced (Total £7k, cash £3k, S&S £7k or £4k if cash used)george4064 said:Will be interesting to see what comes of this. Potentially restricting the amount of cash one can hold in an ISA or reducing the cash ISA allowance to just £4k.0 -

Are you new here?masonic said:

Cash ISAs are somewhat less addictive though.subjecttocontract said:I see nothing wrong with putting a warning on cash ISAs but they put health warnings on cigarette packets and I'm not convinced that more than a tiny, tiny percentage of smokers stop as a result of that warning.") 4

4 -

If you want to boost the UK stock markets they should reduce the Share transaction tax which is higher than most major stock markets. This would boost the Uk stock market and also mean pension funds investing in UK would perform better. That is one of the reasons funds in Uk perform so poorly. They are charged 0.50% for each share purchase, then a lot of the funds charge 0.8% charges per year and on top of that the providers charge 0.40% annual fees, so that it lot of money going in fees if you buy uk shares or funds.

Or at least they could fix it so that shares brought inside Stocks Isa are not charged the 0.5% tax1 -

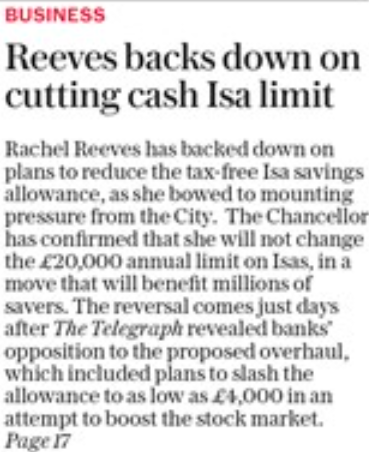

https://archive.is/20250519201802/https://www.telegraph.co.uk/business/2025/05/19/reeves-backs-down-on-plans-to-cut-cash-isa-limit/

"Speaking to the BBC on Monday, Ms Reeves said: “I’m not going to reduce the limit of what people can put into an Isa, but I do want people to get better returns on their savings, whether that’s in a pension or in their day-to-day savings"3 -

Sounds like the major banks talked her out of it.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards