We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

The Old Regular Savers Discussion Thread 28/12/24-29/1/26

Comments

-

Must admit that was my understanding - only in the same tax year could withdrawn ISA subscriptions be replaced, if the isa was "flexible" Others seem to think differently. Hopefully someone can come up with the definitive tax manual answerwiseonesomeofthetime said:

If it is a flexible ISA then you can withdraw money and replace it in the same ISA and in the same tax year without it affecting your £20,000 new money allowance.s71hj said:

So can money be put in say today up to the 20000 max for this tax year, then withdrawn and does that secure that as isa allowance I could put money in in a subsequent tax year in excess of that tax year's £20000?surreysaver said:

I've got a flexible ISA and a flexible mortgage. Take money out of the flexible mortgage this week, put it into the flexible ISA and move the money back next week.flaneurs_lobster said:Why?

* Maxing out an isa before tax year end is the last chance to do it.

* Temporary cash flow problem suggests money 'borrowed' from reg savers could be replaced later in April.

Simples.

I understand the mechanism, just not seeing the underlying reason in meaningful financial advantage terms.So I could get my ISA allowance up to the £20000 limit in this tax year which makes sense in the longer term for my situation. I have a 90 day account maturing on the 10th but that money would be too late for this tax year

Is it not moving £10k earning 6% to ISA(s) earning something similar albeit tax-free for a few days? The increase in earnings will be what? A tenner?

It allows me to max my ISA every tax year and carry that allowance over, so when I've got the cash it allows me to earn interest tax free

If you top up today, and withdraw today, then you will not have that bridge for 2025/26 to replace the withdrawn funds as the transactions are in different tax years.

Hope that makes sense.0 -

As long as the money is in the ISA by 5th April, and taken out on or after 6th April, and redeposited by 5th April next year and so on.s71hj said:

So can money be put in say today up to the 20000 max for this tax year, then withdrawn and does that secure that as isa allowance I could put money in in a subsequent tax year in excess of that tax year's £20000?surreysaver said:

I've got a flexible ISA and a flexible mortgage. Take money out of the flexible mortgage this week, put it into the flexible ISA and move the money back next week.flaneurs_lobster said:Why?

* Maxing out an isa before tax year end is the last chance to do it.

* Temporary cash flow problem suggests money 'borrowed' from reg savers could be replaced later in April.

Simples.

I understand the mechanism, just not seeing the underlying reason in meaningful financial advantage terms.So I could get my ISA allowance up to the £20000 limit in this tax year which makes sense in the longer term for my situation. I have a 90 day account maturing on the 10th but that money would be too late for this tax year

Is it not moving £10k earning 6% to ISA(s) earning something similar albeit tax-free for a few days? The increase in earnings will be what? A tenner?

It allows me to max my ISA every tax year and carry that allowance over, so when I've got the cash it allows me to earn interest tax free

Need to be careful this year, as tax year ends on a weekend, so depends when funds will be shown as credited to the accountI consider myself to be a male feminist. Is that allowed?1 -

Principality 1 Year Triple Access

Maturity warning letter arrived today, not the usual pack with a number of options and prompting to go online/post off to select one. Just a single side of A4 warning the default will pay 2.9% which is among their lowest rates, and advising that you can close the account or transfer money from the Maturity account to another account with them.

So it looks like there’s no more securing an account ahead of time - and the loophole of getting multiple of one RS via maturities closed.4 -

Principality overpaymentKim_13 said:

Accidentally did this with the Maturity Winter - the excess arrived back within about 14 hours. They sent a letter explaining what they had done - no idea why they couldn’t just send a secure message and a text advising to read it.allegro120 said:Principality

I've sent £250 instead of £125 to Christmas by accident. It shows £125 on transactions statement. Has anyone had an experience of exceeding the allowance in a singe transaction? Should I expect the surplus £125 to be automatically returned or do I need to call Principality to resolve this?

Looks like you were lucky. My excess has not yet arrived (4 days). I've chased it today at both ends, Principality and receiving account (Chase). I was told that the returns of overpayments are generated automatically and it can take 3-5 working days, the letter is in the post and they e-mailed it to me so I can share it with Chase. I hope the money will turn up on Monday.

It was also my chance to test Chase and Principality customer services. Both were brilliant - competent, helpful, no waiting in queues etc.

I don't know why some banks and BSs still sending letters where there is no need for it. It must cost them a lot of money. I have to say Principality is not bad at all, I have 10 accounts with them and can't remember receiving any letters for ages. Virgin sends me 2 statements every month for my 10.38% regular savers - they go straight into recycling bin, I can acces my accounts on app and online. I'm sure I've opted for paperless with Virgin years ago.0 -

Very strange - my receiving account was also Chase.allegro120 said:

Principality overpaymentKim_13 said:

Accidentally did this with the Maturity Winter - the excess arrived back within about 14 hours. They sent a letter explaining what they had done - no idea why they couldn’t just send a secure message and a text advising to read it.allegro120 said:Principality

I've sent £250 instead of £125 to Christmas by accident. It shows £125 on transactions statement. Has anyone had an experience of exceeding the allowance in a singe transaction? Should I expect the surplus £125 to be automatically returned or do I need to call Principality to resolve this?

Looks like you were lucky. My excess has not yet arrived (4 days). I've chased it today at both ends, Principality and receiving account (Chase). I was told that the returns of overpayments are generated automatically and it can take 3-5 working days, the letter is in the post and they e-mailed it to me so I can share it with Chase. I hope the money will turn up on Monday.

It was also my chance to test Chase and Principality customer services. Both were brilliant - competent, helpful, no waiting in queues etc.

I don't know why some banks and BSs still sending letters where there is no need for it. It must cost them a lot of money. I have to say Principality is not bad at all, I have 10 accounts with them and can't remember receiving any letters for ages. Virgin sends me 2 statements every month for my 10.38% regular savers - they go straight into recycling bin, I can acces my accounts on app and online. I'm sure I've opted for paperless with Virgin years ago.

Principality’s new go online and look at our account range means not receiving half a forest in options, at least - which I had two of last December. Just a shame they didn’t keep the maturity portal and put a check in to avoid any duplicate accounts being opened. Now if you want to guarantee an account, you have to early close, potentially moving some or all of the balance to a lower rate before you otherwise would have had to.2 -

My 1 Year Triple matures on the 18th, didn't get the 'options' letter yet. Tried to find out for myself, but can't login - website maintenance.... It's a shame that the loophole is closed, but I didn't expect it to last forever so not too disappointedKim_13 said:

Very strange - my receiving account was also Chase.allegro120 said:

Principality overpaymentKim_13 said:

Accidentally did this with the Maturity Winter - the excess arrived back within about 14 hours. They sent a letter explaining what they had done - no idea why they couldn’t just send a secure message and a text advising to read it.allegro120 said:Principality

I've sent £250 instead of £125 to Christmas by accident. It shows £125 on transactions statement. Has anyone had an experience of exceeding the allowance in a singe transaction? Should I expect the surplus £125 to be automatically returned or do I need to call Principality to resolve this?

Looks like you were lucky. My excess has not yet arrived (4 days). I've chased it today at both ends, Principality and receiving account (Chase). I was told that the returns of overpayments are generated automatically and it can take 3-5 working days, the letter is in the post and they e-mailed it to me so I can share it with Chase. I hope the money will turn up on Monday.

It was also my chance to test Chase and Principality customer services. Both were brilliant - competent, helpful, no waiting in queues etc.

I don't know why some banks and BSs still sending letters where there is no need for it. It must cost them a lot of money. I have to say Principality is not bad at all, I have 10 accounts with them and can't remember receiving any letters for ages. Virgin sends me 2 statements every month for my 10.38% regular savers - they go straight into recycling bin, I can acces my accounts on app and online. I'm sure I've opted for paperless with Virgin years ago.

Principality’s new go online and look at our account range means not receiving half a forest in options, at least - which I had two of last December. Just a shame they didn’t keep the maturity portal and put a check in to avoid any duplicate accounts being opened. Now if you want to guarantee an account, you have to early close, potentially moving some or all of the balance to a lower rate before you otherwise would have had to.") 1

1 -

My 1 year Triple also matures on the 18th I received the options letter today, dated 2nd April.allegro120 said:

My 1 Year Triple matures on the 18th, didn't get the 'options' letter yet. Tried to find out for myself, but can't login - website maintenance.... It's a shame that the loophole is closed, but I didn't expect it to last forever so not too disappointedKim_13 said:

Very strange - my receiving account was also Chase.allegro120 said:

Principality overpaymentKim_13 said:

Accidentally did this with the Maturity Winter - the excess arrived back within about 14 hours. They sent a letter explaining what they had done - no idea why they couldn’t just send a secure message and a text advising to read it.allegro120 said:Principality

I've sent £250 instead of £125 to Christmas by accident. It shows £125 on transactions statement. Has anyone had an experience of exceeding the allowance in a singe transaction? Should I expect the surplus £125 to be automatically returned or do I need to call Principality to resolve this?

Looks like you were lucky. My excess has not yet arrived (4 days). I've chased it today at both ends, Principality and receiving account (Chase). I was told that the returns of overpayments are generated automatically and it can take 3-5 working days, the letter is in the post and they e-mailed it to me so I can share it with Chase. I hope the money will turn up on Monday.

It was also my chance to test Chase and Principality customer services. Both were brilliant - competent, helpful, no waiting in queues etc.

I don't know why some banks and BSs still sending letters where there is no need for it. It must cost them a lot of money. I have to say Principality is not bad at all, I have 10 accounts with them and can't remember receiving any letters for ages. Virgin sends me 2 statements every month for my 10.38% regular savers - they go straight into recycling bin, I can acces my accounts on app and online. I'm sure I've opted for paperless with Virgin years ago.

Principality’s new go online and look at our account range means not receiving half a forest in options, at least - which I had two of last December. Just a shame they didn’t keep the maturity portal and put a check in to avoid any duplicate accounts being opened. Now if you want to guarantee an account, you have to early close, potentially moving some or all of the balance to a lower rate before you otherwise would have had to.Fashion on a ration 2025 0/66 coupons spent

79.5 coupons rolled over 4/75.5 coupons spent - using for secondhand purchases

One income, home educating family1 -

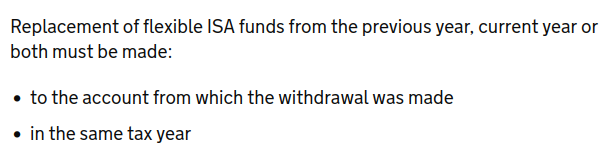

You say "only in the same tax year could withdrawn ISA subscriptions be replaced," It's nothing to do with "subscriptions". With a flexible ISA you can withdraw MONEY and replace it in the same tax year without it affecting your annual allowance. Doesn't matter where that money came from, new money, old money, interest, transfers in, etc.happybagger said:

Must admit that was my understanding - only in the same tax year could withdrawn ISA subscriptions be replaced, if the isa was "flexible" Others seem to think differently. Hopefully someone can come up with the definitive tax manual answerwiseonesomeofthetime said:

If it is a flexible ISA then you can withdraw money and replace it in the same ISA and in the same tax year without it affecting your £20,000 new money allowance.s71hj said:

So can money be put in say today up to the 20000 max for this tax year, then withdrawn and does that secure that as isa allowance I could put money in in a subsequent tax year in excess of that tax year's £20000?surreysaver said:

I've got a flexible ISA and a flexible mortgage. Take money out of the flexible mortgage this week, put it into the flexible ISA and move the money back next week.flaneurs_lobster said:Why?

* Maxing out an isa before tax year end is the last chance to do it.

* Temporary cash flow problem suggests money 'borrowed' from reg savers could be replaced later in April.

Simples.

I understand the mechanism, just not seeing the underlying reason in meaningful financial advantage terms.So I could get my ISA allowance up to the £20000 limit in this tax year which makes sense in the longer term for my situation. I have a 90 day account maturing on the 10th but that money would be too late for this tax year

Is it not moving £10k earning 6% to ISA(s) earning something similar albeit tax-free for a few days? The increase in earnings will be what? A tenner?

It allows me to max my ISA every tax year and carry that allowance over, so when I've got the cash it allows me to earn interest tax free

If you top up today, and withdraw today, then you will not have that bridge for 2025/26 to replace the withdrawn funds as the transactions are in different tax years.

Hope that makes sense.3 -

happybagger said:

Must admit that was my understanding - only in the same tax year could withdrawn ISA subscriptions be replaced, if the isa was "flexible" Others seem to think differently. Hopefully someone can come up with the definitive tax manual answerwiseonesomeofthetime said:

If it is a flexible ISA then you can withdraw money and replace it in the same ISA and in the same tax year without it affecting your £20,000 new money allowance.s71hj said:

So can money be put in say today up to the 20000 max for this tax year, then withdrawn and does that secure that as isa allowance I could put money in in a subsequent tax year in excess of that tax year's £20000?surreysaver said:

I've got a flexible ISA and a flexible mortgage. Take money out of the flexible mortgage this week, put it into the flexible ISA and move the money back next week.flaneurs_lobster said:Why?

* Maxing out an isa before tax year end is the last chance to do it.

* Temporary cash flow problem suggests money 'borrowed' from reg savers could be replaced later in April.

Simples.

I understand the mechanism, just not seeing the underlying reason in meaningful financial advantage terms.So I could get my ISA allowance up to the £20000 limit in this tax year which makes sense in the longer term for my situation. I have a 90 day account maturing on the 10th but that money would be too late for this tax year

Is it not moving £10k earning 6% to ISA(s) earning something similar albeit tax-free for a few days? The increase in earnings will be what? A tenner?

It allows me to max my ISA every tax year and carry that allowance over, so when I've got the cash it allows me to earn interest tax free

If you top up today, and withdraw today, then you will not have that bridge for 2025/26 to replace the withdrawn funds as the transactions are in different tax years.

Hope that makes sense.You can read all about it here: https://www.gov.uk/guidance/manage-isa-subscriptions-for-your-investors#flexible-isasSpecifically: As this is the regular savers thread, it's worth noting replacement also needs to be within the T&Cs of the account. You may not be able to replace a large sum if the monthly contribution limit is just a few hundred pounds.1

As this is the regular savers thread, it's worth noting replacement also needs to be within the T&Cs of the account. You may not be able to replace a large sum if the monthly contribution limit is just a few hundred pounds.1 -

So if I put £5000 in today and take it out tomorrow I'll be able to put £25000 in from tomorrow up to and including 5th April 2026?slinger2 said:

You say "only in the same tax year could withdrawn ISA subscriptions be replaced," It's nothing to do with "subscriptions". With a flexible ISA you can withdraw MONEY and replace it in the same tax year without it affecting your annual allowance. Doesn't matter where that money came from, new money, old money, interest, transfers in, etc.happybagger said:

Must admit that was my understanding - only in the same tax year could withdrawn ISA subscriptions be replaced, if the isa was "flexible" Others seem to think differently. Hopefully someone can come up with the definitive tax manual answerwiseonesomeofthetime said:

If it is a flexible ISA then you can withdraw money and replace it in the same ISA and in the same tax year without it affecting your £20,000 new money allowance.s71hj said:

So can money be put in say today up to the 20000 max for this tax year, then withdrawn and does that secure that as isa allowance I could put money in in a subsequent tax year in excess of that tax year's £20000?surreysaver said:

I've got a flexible ISA and a flexible mortgage. Take money out of the flexible mortgage this week, put it into the flexible ISA and move the money back next week.flaneurs_lobster said:Why?

* Maxing out an isa before tax year end is the last chance to do it.

* Temporary cash flow problem suggests money 'borrowed' from reg savers could be replaced later in April.

Simples.

I understand the mechanism, just not seeing the underlying reason in meaningful financial advantage terms.So I could get my ISA allowance up to the £20000 limit in this tax year which makes sense in the longer term for my situation. I have a 90 day account maturing on the 10th but that money would be too late for this tax year

Is it not moving £10k earning 6% to ISA(s) earning something similar albeit tax-free for a few days? The increase in earnings will be what? A tenner?

It allows me to max my ISA every tax year and carry that allowance over, so when I've got the cash it allows me to earn interest tax free

If you top up today, and withdraw today, then you will not have that bridge for 2025/26 to replace the withdrawn funds as the transactions are in different tax years.

Hope that makes sense.0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.6K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards