We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Flexible ISAs: Current year subscriptions can no longer be replaced in a different ISA

Comments

-

badger09 said:

Are you sure the particular bank allows a proper ISA transfer by that method?Just because they offer the mechanism to move money from one ISA to another, doesn’t necessarily mean it’s recognised as a ISA transfer.badmemory said:

Both with the same bank & an online transfer.gravel_2 said:

Which bank(s)? Did you use the normal transfer route?badmemory said:Be careful what your bank shows on their system. A couple of weeks ago I transferred from one ISA at the end of its fixed period when the rate sank to another with the same bank & they are reporting it as if it is new money. So I only have £8k left of my £20k allowance.

I am now thoroughly narked as the money was tranferred on 4th April, last tax year but in the account on 8th April this tax year so they have totally messed up my ISAs & to add insult to injury the interest will be due on 4th April 25. They used to allow these for the last at least 10 years, but it would appear no longer. A conversation will be required I think.

0 -

Interestingly, I had exactly that sort of conversation with @slinger2 before when I was wondering about reporting by Chip.

Correct me if I am wrong but I think the rules haven't changed, it only has been an attempt to clarify things more.

You can read the exchange below (it goes over a few pages):

https://forums.moneysavingexpert.com/discussion/comment/80727374/#Comment_807273740 -

pecunianonolet said:Interestingly, I had exactly that sort of conversation with @slinger2 before when I was wondering about reporting by Chip.

Correct me if I am wrong but I think the rules haven't changed, it only has been an attempt to clarify things more.

You can read the exchange below (it goes over a few pages):

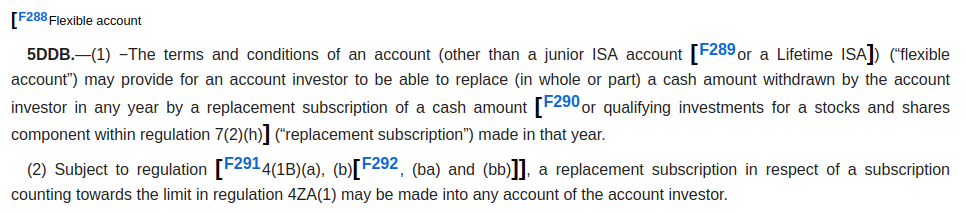

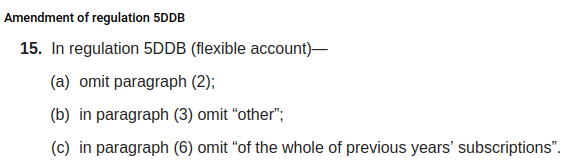

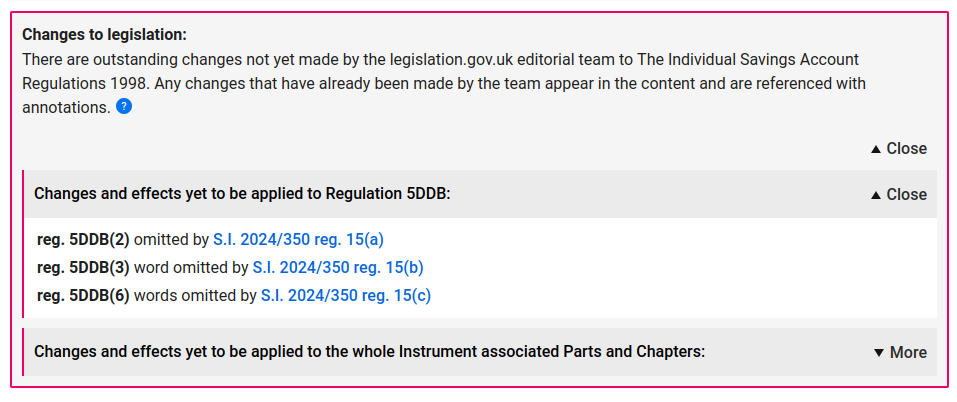

https://forums.moneysavingexpert.com/discussion/comment/80727374/#Comment_80727374The rules have changed. There was a worked example from HMRC showing that current year subscriptions were allowed to be flexibly withdrawn from one ISA and replaced into a different ISA. The guidance issued to ISA managers explicitly stated that they could "effectively be replaced in any current year ISA".Regulation 5DDB(2) introduced in The Individual Savings Account (Amendment) Regulations 2016 states the following: The Individual Savings Account (Amendment) Regulations 2024 amends 5DDB to remove (2):

The Individual Savings Account (Amendment) Regulations 2024 amends 5DDB to remove (2): If you go to the original 1998 instrument, this doesn't yet reflect the 2024 changes, they have an alert warning of this:

If you go to the original 1998 instrument, this doesn't yet reflect the 2024 changes, they have an alert warning of this: This change to the legislation appears to have been missed by everyone, including HMRC, which is why it wasn't included with all of the other HMRC updates prior to the start of this tax year. I suppose when the purpose of the amendment is to introduce greater freedoms, it is easy to overlook a line that, without reference to its effect, removes a freedom.Regarding your conversation with slinger2, this won't make things any better regarding reporting of the available allowance by providers. If you open 3 cash ISAs, each will start showing £20k available to add for the 2024/25 tax year (even if you've already used your allowance with one of the others), and the each calculation will only be adjusted to account for your activity with the provider of the ISA in question. So it will be easy to mistakenly oversubscribe unless you check what you have paid into each of your ISAs for the tax year. There is no requirement, nor facility, for any ISA manager to show allowance that is only available to use in their ISA and not elsewhere. ISA managers assume you only have one current year ISA and have no knowledge of what you may have been doing elsewhere. This is how it has always been, despite it being possible to subscribe to more than one ISA almost since the inception of ISAs.5

This change to the legislation appears to have been missed by everyone, including HMRC, which is why it wasn't included with all of the other HMRC updates prior to the start of this tax year. I suppose when the purpose of the amendment is to introduce greater freedoms, it is easy to overlook a line that, without reference to its effect, removes a freedom.Regarding your conversation with slinger2, this won't make things any better regarding reporting of the available allowance by providers. If you open 3 cash ISAs, each will start showing £20k available to add for the 2024/25 tax year (even if you've already used your allowance with one of the others), and the each calculation will only be adjusted to account for your activity with the provider of the ISA in question. So it will be easy to mistakenly oversubscribe unless you check what you have paid into each of your ISAs for the tax year. There is no requirement, nor facility, for any ISA manager to show allowance that is only available to use in their ISA and not elsewhere. ISA managers assume you only have one current year ISA and have no knowledge of what you may have been doing elsewhere. This is how it has always been, despite it being possible to subscribe to more than one ISA almost since the inception of ISAs.5 -

I see that the change came into force on 6 April 2024, so anyone moving new 24/25 money from a flexible ISA to another ISA has broken the rules.

Currently https://www.gov.uk/guidance/manage-isa-subscriptions-for-your-investors#flexible-isas (Last updated 30 April 2024) says:

"For flexible ISAs, the ‘net’ subscriptions should be reported on the annual returns of information."

Under this system HMRC are still not going to know whether people are breaking the rules or not.

0 -

Looks like HMRC doesn't know what they are doing.masonic said:pecunianonolet said:Interestingly, I had exactly that sort of conversation with @slinger2 before when I was wondering about reporting by Chip.

Correct me if I am wrong but I think the rules haven't changed, it only has been an attempt to clarify things more.

You can read the exchange below (it goes over a few pages):

https://forums.moneysavingexpert.com/discussion/comment/80727374/#Comment_80727374The rules have changed. There was a worked example from HMRC showing that current year subscriptions were allowed to be flexibly withdrawn from one ISA and replaced into a different ISA. The guidance issued to ISA managers explicitly stated that they could "effectively be replaced in any current year ISA".Regulation 5DDB(2) introduced in The Individual Savings Account (Amendment) Regulations 2016 states the following:The Individual Savings Account (Amendment) Regulations 2024 amends 5DDB to remove (2):If you go to the original 1998 instrument, this doesn't yet reflect the 2024 changes, they have an alert warning of this:This change to the legislation appears to have been missed by everyone, including HMRC, which is why it wasn't included with all of the other HMRC updates prior to the start of this tax year. I suppose when the purpose of the amendment is to introduce greater freedoms, it is easy to overlook a line that, without reference to its effect, removes a freedom.Regarding your conversation with slinger2, this won't make things any better regarding reporting of the available allowance by providers. If you open 3 cash ISAs, each will start showing £20k available to add for the 2024/25 tax year (even if you've already used your allowance with one of the others), and the each calculation will only be adjusted to account for your activity with the provider of the ISA in question. So it will be easy to mistakenly oversubscribe unless you check what you have paid into each of your ISAs for the tax year. There is no requirement, nor facility, for any ISA manager to show allowance that is only available to use in their ISA and not elsewhere. ISA managers assume you only have one current year ISA and have no knowledge of what you may have been doing elsewhere. This is how it has always been, despite it being possible to subscribe to more than one ISA almost since the inception of ISAs.

In the guidance to ISA managers it said before, even pre 6th April, that for flexible ISAs funds can only be replaced in the ISA they originate from.

https://www.gov.uk/guidance/who-can-invest-in-an-isa-if-youre-an-isa-managerFor flexible ISAs, replacement funds can only be credited to the account they originated from.

Indeed, the guidance for ISA investors before recent amends were made saidWithdrawals of current year subscriptions, can effectively be replaced in any current year ISA.https://www.gov.uk/guidance/manage-isa-subscriptions-for-your-investors#flexible-isas

I think the second statement was more in relation that you could withdraw funds from a cash ISA and replace in a Stocks & Share ISA or any other allowed type as you were not allowed to have more ISA's of the same type with current year subscriptions.

With the recent amends to me it looks more like further clarification to align their guidance and take conflicting information out, rather than a full change of course. However, the legislation documents again say different.

None of the changes, regardless if this is deemed a rule change or amend, make any difference unless the reporting changes. It still allows, if prepared to take any subsequent consequences, to oversubscribe within a tax year due to the current net reporting on flexible ISAs. The risk of course is that an ISA is declared invalid at a later time and interest received becomes taxable.

I think the best we can do at this point is to wait how things develop, await any further updates and see if MSE can get a straight answer from HMRC directly when they review/update their article. In the meantime, recording what you paid in where and when might not be a bad idea either.

0 -

No, that page has also been updated on 6 April with the new rule, while earlier in the year it was different (and consistent with the other guidance at the time):pecunianonolet said:

In the guidance to ISA managers it said before, even pre 6th April, that for flexible ISAs funds can only be replaced in the ISA they originate from.

https://www.gov.uk/guidance/who-can-invest-in-an-isa-if-youre-an-isa-managerFor flexible ISAs, replacement funds can only be credited to the account they originated from.

In the case of a flexible ISA, withdrawals of current year subscriptions, can effectively be replaced in any current year ISA, but cannot breach the ‘one ISA of each type per tax year’ rule.https://web.archive.org/web/20240118104059/https://www.gov.uk/guidance/who-can-invest-in-an-isa-if-youre-an-isa-manager

Not sure why one guidance page was updated on 6 April and it took until the 30th for the other to follow, but hard to disagree with your assertion that "Looks like HMRC doesn't know what they are doing"!5 -

eskbanker said:Not sure why one guidance page was updated on 6 April and it took until the 30th for the other to follow, but hard to disagree with your assertion that "Looks like HMRC doesn't know what they are doing"!I think both guidance pages were updated on 6th April. One of them to state that replacement subscriptions had to go back into the ISA they were withdrawn from, the other to remove the statement about not breaching 'one ISA of each type per tax year' but leave the 'any [valid] current year ISA' in place (removing the word 'valid' IIRC).The tax free savings bulletin to ISA managers issued the month before and describing the changes was silent on this issue.1

-

Yes, you're right - https://www.gov.uk/guidance/manage-isa-subscriptions-for-your-investors was indeed updated on 6 April, but the document change control history was only belatedly amended on 30 April to reflect the fact that the flexibility wording had already been changed!masonic said:eskbanker said:Not sure why one guidance page was updated on 6 April and it took until the 30th for the other to follow, but hard to disagree with your assertion that "Looks like HMRC doesn't know what they are doing"!I think both guidance pages were updated on 6th April. One of them to state that replacement subscriptions had to go back into the ISA they were withdrawn from, the other to remove the statement about not breaching 'one ISA of each type per tax year' but leave the 'any [valid] current year ISA' in place (removing the word 'valid' IIRC).The tax free savings bulletin to ISA managers issued the month before and describing the changes was silent on this issue.0 -

eskbanker said:

Yes, you're right - https://www.gov.uk/guidance/manage-isa-subscriptions-for-your-investors was indeed updated on 6 April, but the document change control history was only belatedly amended on 30 April to reflect the fact that the flexibility wording had already been changed!masonic said:eskbanker said:Not sure why one guidance page was updated on 6 April and it took until the 30th for the other to follow, but hard to disagree with your assertion that "Looks like HMRC doesn't know what they are doing"!I think both guidance pages were updated on 6th April. One of them to state that replacement subscriptions had to go back into the ISA they were withdrawn from, the other to remove the statement about not breaching 'one ISA of each type per tax year' but leave the 'any [valid] current year ISA' in place (removing the word 'valid' IIRC).The tax free savings bulletin to ISA managers issued the month before and describing the changes was silent on this issue.The flexibility wording was changed twice on that page. I have a screenshot of the paragraph captured on 29th April showing the intermediate wording that still contained the part about replacing in any current year ISA. I also have a screenshot from March of the same page with the extended version with a clause about one ISA of each type per tax year. So they edited on 6th, without removing the important part, then went back on 30th to correct their mistake. There were inconsistent messages on the two pages mentioned between the 6th and 30th.You've quoted the pre-6th April and 6-30th April versions here: https://forums.moneysavingexpert.com/discussion/comment/80753861/#Comment_80753861Those both differ from the current version.1 -

eskbanker said:

Yes, you're right - https://www.gov.uk/guidance/manage-isa-subscriptions-for-your-investors was indeed updated on 6 April, but the document change control history was only belatedly amended on 30 April to reflect the fact that the flexibility wording had already been changed!masonic said:eskbanker said:Not sure why one guidance page was updated on 6 April and it took until the 30th for the other to follow, but hard to disagree with your assertion that "Looks like HMRC doesn't know what they are doing"!I think both guidance pages were updated on 6th April. One of them to state that replacement subscriptions had to go back into the ISA they were withdrawn from, the other to remove the statement about not breaching 'one ISA of each type per tax year' but leave the 'any [valid] current year ISA' in place (removing the word 'valid' IIRC).The tax free savings bulletin to ISA managers issued the month before and describing the changes was silent on this issue.'Withdrawals of current year subscriptions, can effectively be replaced in any current year ISA, but cannot breach the ‘one ISA of each type per tax year’ rule.'

If it helps, these were the words in place at 06/02/24, for sure.

On that day I had cut & pasted the words and emailed them to a friend, along with a the link to the HMRC doc.

2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards