We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Flexible ISAs: Current year subscriptions can no longer be replaced in a different ISA

masonic

Posts: 29,712 Forumite

This came up in a thread on the main savings board, but I thought it worthy of its own thread, as several forumites make use of ISA flexibility to move money between their various ISAs and it has been the subject of quite a few threads in the past month or so. Original thread is: https://forums.moneysavingexpert.com/discussion/6526323/moving-s-s-isa-same-year and credit to @eskbanker for checking and finding the changed guidance from HMRC.

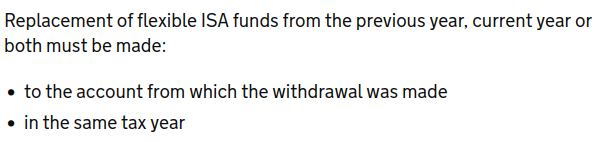

Before 30th April, HMRC guidance was clear that money flexibly withdrawn from a current year ISA could effectively be replaced in any current year ISA. It now says that it must be replaced to the account from which the withdrawal was made:

...and in the updates section, it states that the wording has been updated to "clarify" this. There was no mention of any impending change in the most recent tax free savings bulletin.

I struggle to see HMRC enforcing this, but this is their new stance.

7

Comments

-

I'd replied on the other thread but will post here for completeness

I'm currently using this aspect of flexible ISAs and it seems utterly bizarre that something like this is changed mid way through a tax year. I can completely understand the reasoning as otherwise the reporting aspect and potential for errors by customers must be very high and virtually impossible to police but some warning rather than a hidden update would be sensible.Remember the saying: if it looks too good to be true it almost certainly is.4 -

Perhaps that is the reasoning behind it, although I think under the new system things will be even more complicated. Under the old system, providers reported the amount of annual allowance remaining (£20,000 minus net subscriptions). Any figure below £20k meant some current year subscriptions had been used, and all that is required of the investor is to do the sum £20k minus available allowance to determine how much they have used in that ISA (a negative number means zero).Under the new system, this is not possible if money has been flexibly withdrawn at any point in the tax year. Suppose they paid in £10k and flexibly withdrew £5k. Currently the ISA managers would all report £15k remaining, but in fact the investor has used £10k of their annual allowance. If they then put that money into a different ISA, they'll have used £15k of their allowance. Then they add another £10k to the second ISA and they've breached their limit, while the two ISA managers are saying they have £15k and £5k available respectively. At least under the old system they could deduce that they'd made £5k and £15k net subscriptions respectively without having to go through all of their transactions with a fine tooth comb.So new functionality will need to be rolled out across ISA managers to make it clearer to customers the difference between unused allowance and replacement subscription allowance.3

-

This new system is only going to be enforceable if ISA managers report (to HMRC) the maximum amount of new money that has been deposited rather than the final net amount. eg deposit £10k, withdraw £5k, deposit £1k: rather than reporting the net figure of £6k they're going to need to report £10k (another £4k could have been deposited but wasn't during the tax year)

Clearly it's going to be difficult to enforce the new rule this year but perhaps they'll change everything next year.1 -

slinger2 said:This new system is only going to be enforceable if ISA managers report (to HMRC) the maximum amount of new money that has been deposited rather than the final net amount. eg deposit £10k, withdraw £5k, deposit £1k: rather than reporting the net figure of £6k they're going to need to report £10k (another £4k could have been deposited but wasn't during the tax year)

Clearly it's going to be difficult to enforce the new rule this year but perhaps they'll change everything next year.ISA managers don't have to report 2024/25 subscriptions until summer 2025, so there is over a year for the system to be changed. However, I don't have much faith in it being done by then!With the new freedoms, planned changes around fractional shares, and now this, ISA managers nationwide are going to be having nightmares about new changes being sprung on them

1 -

My trouble is that I've parked some of this year's money in a flexi ISA on the basis that I can withdraw it later in the tax year, perhaps when I find a good fixed-rate ISA. Seems that's no longer allowed. Not sure what to do now.1

-

You'd still be able to use the ISA transfer system to move it in. It's just more hassle to follow that process.slinger2 said:My trouble is that I've parked some of this year's money in a flexi ISA on the basis that I can withdraw it later in the tax year, perhaps when I find a good fixed-rate ISA. Seems that's no longer allowed. Not sure what to do now.

1 -

Wouldn't the reason for it be as a solution to those with the money to do so attempting to protect many times the annual allowance from tax for most of the year under the new system?

If you open an ISA, deposit £20K and flexibly withdraw the lot in early April 2025, wouldn't it otherwise be reported that no allowance had been used? If you are effectively restricted to one flexible ISA only, then it would seem to close that loophole.1 -

It does close the loophole. It's just annoying that it also restricts people who were abiding by the rules.Kim_13 said:Wouldn't the reason for it be as a solution to those with the money to do so attempting to protect many times the annual allowance from tax for most of the year under the new system?

If you open an ISA, deposit £20K and flexibly withdraw the lot in early April 2025, wouldn't it otherwise be reported that no allowance had been used? If you are effectively restricted to one flexible ISA only, then it would seem to close that loophole.

Looks like you can still have many flexi ISAs, but now they must effectively be run independently, you can't move money from one to another.1 -

Kim_13 said:Wouldn't the reason for it be as a solution to those with the money to do so attempting to protect many times the annual allowance from tax for most of the year under the new system?

If you open an ISA, deposit £20K and flexibly withdraw the lot in early April 2025, wouldn't it otherwise be reported that no allowance had been used? If you are effectively restricted to one flexible ISA only, then it would seem to close that loophole.Perhaps this is the reason. Unless the reporting system is also changed, it will make no difference to those fraudulently oversubscribing and then flexibly withdrawing before the end of the tax year. Because they wouldn't be making replacement subscriptions. So maybe they do intend to change the reporting rules before the 2024/25 returns.The timing suggests HMRC may have got wind of some early abusers of the system rather than anticipating it.1 -

Masonic zooming around the forum with this news.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards