We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

E.ON Next Tariff Renewal

Comments

-

RG2015 said:

You are comparing 2% per month ( = 24% p.a.) on a payment that would happen anyway with 6% p.a. for locking money away in a savings account.Scot_39 said:

If the cash back is only 2% why would OP want to max it out ?Sea_Shell said:If you want to increase your DD manually to benefit from Santander cashback, you can probably just do this, separately from your tariff ending.

You'd be limited to a certain % above their recommended, but it would be up to £250 a month, before you max out at £5 a month c/b (2%)

You can get more in a standard instant access on line savings account on the money, possibly a lot more in a regular saver.

There are some paying over 6% with right bank / account.

Lending it to the energy company for 2% and yhe potential rebate i.e, access issues seems a strange choice.

Exactly.

Overpay, get 2% cashback, build up credit, request a refund, rinse and repeat.

How's it going, AKA, Nutwatch? - 12 month spends to date = 3.24% of current retirement "pot" (as at end December 2025)0 -

RG2015 said:

You are comparing 2% per month ( = 24% p.a.) on a payment that would happen anyway with 6% p.a. for locking money away in a savings account.Scot_39 said:

If the cash back is only 2% why would OP want to max it out ?Sea_Shell said:If you want to increase your DD manually to benefit from Santander cashback, you can probably just do this, separately from your tariff ending.

You'd be limited to a certain % above their recommended, but it would be up to £250 a month, before you max out at £5 a month c/b (2%)

You can get more in a standard instant access on line savings account on the money, possibly a lot more in a regular saver.

There are some paying over 6% with right bank / account.

Lending it to the energy company for 2% and yhe potential rebate i.e, access issues seems a strange choice.It's not really 24% is it. Its not accumulative - you don't get 2%/£5 on the same £250 every month - you get it once - the next 2% is on new money - and the utility company holds onto the excess paying you nothing for the next n months until rebate.

And the £250 "wouldnt just happen anyway" - "so say for instance for ease" - you only actually needed to pay £125 to cover the bill. You woudn't do it unless you had the rebate. It wouldn't be building credit for a future refund - if it was needed.So your 24% is of £250 = £60 - but you handover £3000 - including that extra £1500 you don't actually have to - to get £30 of it.So again its 2% of the total (2% of £3000 = £60) - not the monthly.So 2% - it's a rebate - not an interest rate - never be confused as one - there's no rate/time factor.So let me be clear - the £30 for the actual bill is literally free money (excluding it's share of the acount fee of course - £48pa).The other £125 is essentially a "savings" mechanismThe current 2% rebate therefore not great in say month 1 / Jan cf a high rate savings accountBut brillaint in later months - where the savings account would only be earning - months remaining= n, n/12ths of the flat rate.So lets take one scenario - your £250 - double required - for a full 12m payment123 2% rebate pathJan 250 - £5 rebateFeb 250 - £5...Dec 250 - £5£3000 in DD Payments, £60 total 2% Santander credit, supplier rebate £1500 - maybe x days later than requested, maybe not 100% risk (the - no we want to hold onto 1m,2m credit etc as it's ... etc).And in super gloom mode - there's the recent collapses - months to clear any credit at all.Vs pay only bill, save other half at say 3-6%Jan 125 DD - 2.50 £125 into savings account earns 6% pa in reg saver for 11m £6.87 - (*)a lot more than £2.50Feb 125 DD - 2.50 £125 into savings account earns for 10 months - £6.25 (*)...Nov 125 DD - 2.50 £125 into savings account earns for 1 months - £0.625 - (**)a lot less than £2.50Dec 125 DD - £2.50 £125 saving only if lift Jan 1st(***)£1500 in DD payments, £1500 (1275+125 or 1500 in RS) in capital, £30 rebate, £41.25 in interest at 6% if lift Dec (11m), £48.75 if lift Jan (12m), guaranteed access - £71.25 or £78.75 combined.Drop the rate to 5% - £64, or £70.62Drop the rate to 4% - £57.5 or £62.50Drop the rate to 3% - £50.62 or £54.37 - best instant access - c3.2% conv, 3.4% app.Losses cf £60 123 route in bold.Think need rate 4.37% flat to break even at Dec1st, Or 3.7% Jan 1st.So not quite there on instant.But on best regular savers - possible (but these tend to be tied).All ignoring the compound interest on £2 monthly if left in account at c2% - 22p/26pBut also need to arguably factor in the £4 pm - £48 per annum account fee - for the main account. To secure perks like 2% interest - the DD rebates - and ....AND arguably the optimal plan - if the utility companies would allow it - is to save the money to a high interest savings account - like a regular saver for the early part of the year - when has longer to earn interest to term (and so interest exceeds the rebate like (*). Or some ramp in between.Then maximise the rebate - towards the end - to earn the fixed 2% rebate 125 = 2.50 (when the interest is less eg (**)).0 -

"It's not really 24% is it. Its not accumulative"Scot_39 said:

If the cash back is only 2% why would OP want to max it out ?Sea_Shell said:If you want to increase your DD manually to benefit from Santander cashback, you can probably just do this, separately from your tariff ending.

You'd be limited to a certain % above their recommended, but it would be up to £250 a month, before you max out at £5 a month c/b (2%)

You can get more in a standard instant access on line savings account on the money, possibly a lot more in a regular saver.

There are some paying over 6% with right bank / account.

Lending it to the energy company for 2% and yhe potential rebate i.e, access issues seems a strange choice.

You are correct it is not cumulative. But 2% for one month is equivalent to 24% per annum.

Therefore your statement that you could get more in a standard instant access account is incorrect.

Ignoring the cumulative effect, a £250 DD would earn 2% cashback of £5 in one month

£250 in an easy access account for one month would earn £250 x 3% / 12 = £0.625.

0 -

RG2015 said:

"It's not really 24% is it. Its not accumulative"Scot_39 said:

If the cash back is only 2% why would OP want to max it out ?Sea_Shell said:If you want to increase your DD manually to benefit from Santander cashback, you can probably just do this, separately from your tariff ending.

You'd be limited to a certain % above their recommended, but it would be up to £250 a month, before you max out at £5 a month c/b (2%)

You can get more in a standard instant access on line savings account on the money, possibly a lot more in a regular saver.

There are some paying over 6% with right bank / account.

Lending it to the energy company for 2% and yhe potential rebate i.e, access issues seems a strange choice.

You are correct it is not cumulative.

But your statement that you could get more in a standard instant access account is incorrect.

Ignoring the cumulative effect, a £250 DD would earn 2% cashback of £5 in one month

£250 in an easy access account for one month would earn £250 x 3% / 12 = £0.625.Yes that bit was a push to be fair. As the figures in my long post calcs showed and I admitted.But once again - your comparison isn't valid either - its just looking at the interest for 1 month - UNLESS you are truly expecting to lift the rebate from the utility company every month.Because the interest rate is a rate - so in month 1 - assuming a once per year utility rebate - the excess is invested for upto 11 or 12 months - depending on planned time for that rebate from utility. Decreasing over the year.You cannot invest the full £250 - only in my example - £125 - or rather the actual excess to £250 - I just used 50% as a nice round example. The reality far less on average I suspect - EPG £2500 is £208pm so leaves c£40 pm for instance.The interest on balance at 2% + the three tiers of rebate - all in part offset against the £48 fee too.I actually liked the idea of the account - I came very close to opening one when relatively new.0 -

Fair enough, although mine was not a direct comparison other than to counter your "you could get more elsewhere" bit.Scot_39 said:RG2015 said:

"It's not really 24% is it. Its not accumulative"Scot_39 said:

If the cash back is only 2% why would OP want to max it out ?Sea_Shell said:If you want to increase your DD manually to benefit from Santander cashback, you can probably just do this, separately from your tariff ending.

You'd be limited to a certain % above their recommended, but it would be up to £250 a month, before you max out at £5 a month c/b (2%)

You can get more in a standard instant access on line savings account on the money, possibly a lot more in a regular saver.

There are some paying over 6% with right bank / account.

Lending it to the energy company for 2% and yhe potential rebate i.e, access issues seems a strange choice.

You are correct it is not cumulative.

But your statement that you could get more in a standard instant access account is incorrect.

Ignoring the cumulative effect, a £250 DD would earn 2% cashback of £5 in one month

£250 in an easy access account for one month would earn £250 x 3% / 12 = £0.625.Yes that bit was a push to be fair. As the figures in my long post calcs showed and I admitted.But once again - your comparison isn't valid either - its just looking at the interest for 1 month - UNLESS you are truly expecting to lift the rebate from the utility company every month..

All I claim is that with a bit of judicious planning you could earn more by overpaying E.ON than by just depositing the extra cash in a savings account.

I did this last year when the Santander cashback was doubled to 4% and the limit also doubled to £10 per month for two months.

I really couldn't be bothered with the full £250 now, although I may overpay by a small amount and still be well up on the deal.2 -

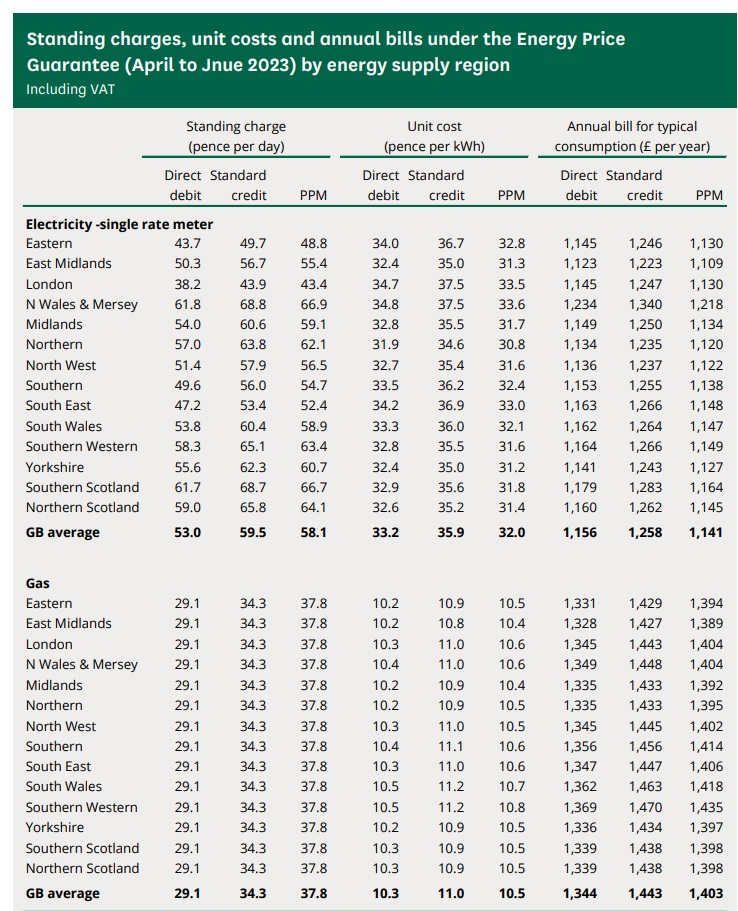

The quoted prices have now changed to agree with the ones on the list below.Sea_Shell said:No difference. AIUI even if you "choose" it, you'd stay on your fix until the end.

They just don't appear to have changed their software to account for the current situation, compared to when fixes were available.

Have you seen my thread on a similar subject?

https://forums.moneysavingexpert.com/discussion/6430886/notification-of-increase-timescales#latest

You won't get the quoted price, as it'll change on the 1st April.

These are courtesy of DerwentMailman on the thread on this link.

https://forums.moneysavingexpert.com/discussion/comment/79922303#Comment_79922303

3

3 -

Have seen reports that EON are actually tweaking prices, reducing unit price and increasing SC, so I suggest EON customers check to make sure they actually staying at same levels.

0 -

Reflected in table above your post.Chrysalis said:Have seen reports that EON are actually tweaking prices, reducing unit price and increasing SC, so I suggest EON customers check to make sure they actually staying at same levels.0 -

That will be the same for all suppliers with the new Standing Charges announced by Ofgem for 1st April then the Government EPG taking amounts of the kWh prices.Chrysalis said:Have seen reports that EON are actually tweaking prices, reducing unit price and increasing SC, so I suggest EON customers check to make sure they actually staying at same levels.1 -

Yes, they have tweaked their rates as you have said. I am coming off a fix on 1st April and my forecast tariff shown online was changed last Thursday, (16th March). This is in accord with the table a few posts back.Chrysalis said:Have seen reports that EON are actually tweaking prices, reducing unit price and increasing SC, so I suggest EON customers check to make sure they actually staying at same levels.

The email I received on 14th February had the old E.ON Next variable rates. I guess at some point they will notify me directly of the new rates.

As I have been on fixed rate deals for many years with different suppliers, I have no idea how any of them advise customers of changes in their variable rates.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards