We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

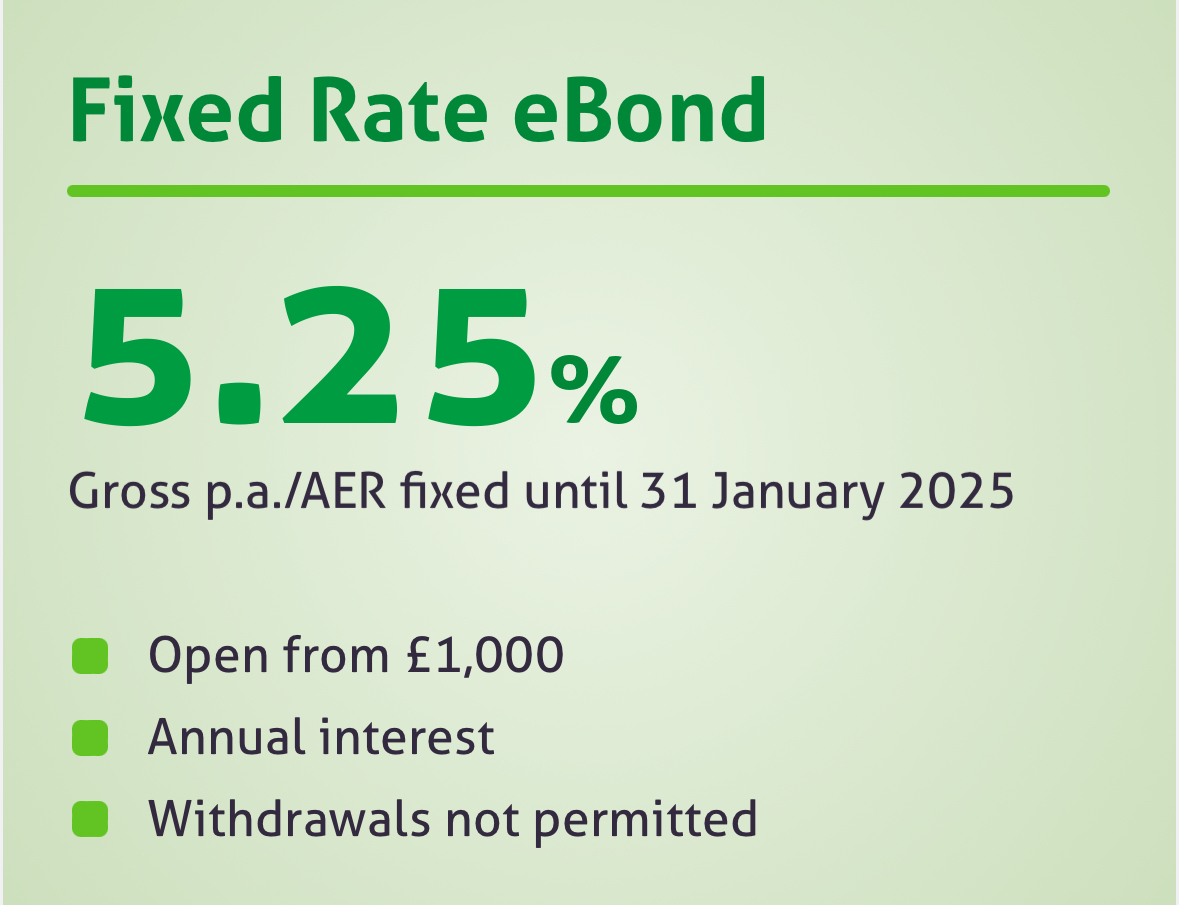

The Top Fixed Interest Savings Discussion Area

Comments

-

6.01% if you are a 20% taxpayer = 4.8%.

If you are a 40% taxpayer you get = 3.6%

Inflation will take what's left, and more.0 -

multiple deposits within that 14 day window will be fine with Oxbury.SickGroove said:It states I have 14 days to fund my 2 year fixed rate account, so as my main current fix doesn't mature til 17/11, can I make multiple deposits up until the 14 days or does it all need to be deposited in one go?

you might want to double-check with Oxbury about the interest being paid upon maturity as the product summary for the 2-yr fix says that the interest is paid ANNUALLY... and I think my previous multi-year fix interest with them was paid annually rather than all at maturity.SickGroove said:Finally, as the interest is compounded & paid after the two years...a 68K deposit will generate considerable interest...with the interest being paid into the fixed-rate account and therefore inaccessible to you, it's questionable whether you would *need* to declare it next year - but that's a whole other can of worms being discussed on many other threads here!- Interest will be paid annually with reference to the date of receipt of your first deposit and credited to your savings account

possibly if you wanted to avoid a tax issue in 25/26, you could just declare next year's interest when paid.2 - Interest will be paid annually with reference to the date of receipt of your first deposit and credited to your savings account

-

-

I opened an Oxbury 2 year yesterday after a big struggle with my old phone. The interest is paid annually.• Accounts cannot be opened with balances below £1,000• Interest is calculated daily• Interest will be paid annually with reference to the date of receipt of your first deposit and credited to your savingsaccount• Where we pay interest annually, your AER and gross rate will be the same• All our interest rates are available at www.oxbury.com

I opened a Vanquis 2 year at 5.9% before their rate went down and have not funded this or Oxbury yet. Trying to decide which one to fund. What are peoples opinions of these two savings providers, I have not used either before?0 -

with Oxbury, you can open a fix with a £1 test deposit, it's just that you need to get to £1k+ balance within that 14 day funding window - deposits with Oxbury are immediate in my experience.DavidAC said:I opened an Oxbury 2 year yesterday after a big struggle with my old phone. The interest is paid annually.• Accounts cannot be opened with balances below £1,000• Interest is calculated daily• Interest will be paid annually with reference to the date of receipt of your first deposit and credited to your savingsaccount• Where we pay interest annually, your AER and gross rate will be the same• All our interest rates are available at www.oxbury.com

I opened a Vanquis 2 year at 5.9% before their rate went down and have not funded this or Oxbury yet. Trying to decide which one to fund. What are peoples opinions of these two savings providers, I have not used either before?

never used Vanquis, but been with Oxbury for a few years - very helpful staff available via chat during the week and very quick to answer emails (often within minutes)... I would have no issue with opening another account with them.3 -

I've had a bit of, what seems to me, rather an oddity. I have a Skipton 1 year fix maturing this month and they've sent me the email about it, with my options. Skiptons 'do nothing' default maturity option is to put the funds into another 1 year fix. The rate they've offered is 5.2% AER, 5.08% monthly (just called Maturity, no issue number). Yet on their public Web site, their current rate for a 1 year fix (issue 230) is 5.25% AER, 5.13% monthly.

This is my first fix maturing, so I've no prior direct experience - but reading here it seems to be more conventional that maturing fixes tend to secure a slightly better rate for loyal current customers? I'm not taking another fix anyway, I already secured one a few weeks ago in lieu of this, by borrowing from my EA funds, just before rates started dropping.

1 -

I've had "loyalty" rates from some banks on fixes maturing and just the normal offering from others.BooJewels said:I've had a bit of, what seems to me, rather an oddity. I have a Skipton 1 year fix maturing this month and they've sent me the email about it, with my options. Skiptons 'do nothing' default maturity option is to put the funds into another 1 year fix. The rate they've offered is 5.2% AER, 5.08% monthly (just called Maturity, no issue number). Yet on their public Web site, their current rate for a 1 year fix (issue 230) is 5.25% AER, 5.13% monthly.

This is my first fix maturing, so I've no prior direct experience - but reading here it seems to be more conventional that maturing fixes tend to secure a slightly better rate for loyal current customers? I'm not taking another fix anyway, I already secured one a few weeks ago in lieu of this, by borrowing from my EA funds, just before rates started dropping.

At this point, I employ a wait-and-see approach") as each one matures. 1

as each one matures. 1 -

I wouldn't have an issue with it being the same rate as their current offerings - but offering a lower rate to an existing customer seems a bit naughty. Obviously, if I were in the market for a new fix with them, I could cash in this one and then open a new fix, but it seems a bit shortsighted to force me into doing that when it's more work for both parties.Ozzig said:

I've had "loyalty" rates from some banks on fixes maturing and just the normal offering from others.BooJewels said:I've had a bit of, what seems to me, rather an oddity. I have a Skipton 1 year fix maturing this month and they've sent me the email about it, with my options. Skiptons 'do nothing' default maturity option is to put the funds into another 1 year fix. The rate they've offered is 5.2% AER, 5.08% monthly (just called Maturity, no issue number). Yet on their public Web site, their current rate for a 1 year fix (issue 230) is 5.25% AER, 5.13% monthly.

This is my first fix maturing, so I've no prior direct experience - but reading here it seems to be more conventional that maturing fixes tend to secure a slightly better rate for loyal current customers? I'm not taking another fix anyway, I already secured one a few weeks ago in lieu of this, by borrowing from my EA funds, just before rates started dropping.

At this point, I employ a wait-and-see approach as each one matures.1 -

They are at it, offering a lower rate than advertised on their website.BooJewels said:I've had a bit of, what seems to me, rather an oddity. I have a Skipton 1 year fix maturing this month and they've sent me the email about it, with my options. Skiptons 'do nothing' default maturity option is to put the funds into another 1 year fix. The rate they've offered is 5.2% AER, 5.08% monthly (just called Maturity, no issue number). Yet on their public Web site, their current rate for a 1 year fix (issue 230) is 5.25% AER, 5.13% monthly.

This is my first fix maturing, so I've no prior direct experience - but reading here it seems to be more conventional that maturing fixes tend to secure a slightly better rate for loyal current customers? I'm not taking another fix anyway, I already secured one a few weeks ago in lieu of this, by borrowing from my EA funds, just before rates started dropping.

Some do offer genuine loyalty rates, personally know that Charter, Kent Reliance and Monument do.

Tandem say they may do, but when I went to check recently for a very small amount maturing, it was the same rate advertised on website. I chose to withdraw, with the intention of funding a regular saver. Two days before maturity, they offered me a better rate, which worked out a tad better than going with regular saver, so just stuck with them.1 -

So if interest paid annually on their 2 year fix, it will initially get paid November 24 so will be included in 24/25 tax year then it's compound & then get paid again November 25 so will be included in 25/26 tax year?janusdesign said:

multiple deposits within that 14 day window will be fine with Oxbury.SickGroove said:It states I have 14 days to fund my 2 year fixed rate account, so as my main current fix doesn't mature til 17/11, can I make multiple deposits up until the 14 days or does it all need to be deposited in one go?

you might want to double-check with Oxbury about the interest being paid upon maturity as the product summary for the 2-yr fix says that the interest is paid ANNUALLY... and I think my previous multi-year fix interest with them was paid annually rather than all at maturity.SickGroove said:Finally, as the interest is compounded & paid after the two years...a 68K deposit will generate considerable interest...with the interest being paid into the fixed-rate account and therefore inaccessible to you, it's questionable whether you would *need* to declare it next year - but that's a whole other can of worms being discussed on many other threads here!- Interest will be paid annually with reference to the date of receipt of your first deposit and credited to your savings account

possibly if you wanted to avoid a tax issue in 25/26, you could just declare next year's interest when paid.

IE the big lump sum over the 2 year period is split between 2 tax years right?

I've never needed to do a HMRC self assessment form, so I'd rather then just work it out...I just need to make sure my tax year interest isn't over 10K right?0 - Interest will be paid annually with reference to the date of receipt of your first deposit and credited to your savings account

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards