We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

How much to live on

Comments

-

For somethings, like employment income, you can just change the estimate directly on the website.Rusty190 said:

mybestattempt : May I ask how and when you do this?mybestattempt said:@Organgrinder and @helensbiggestfan

Do you have an online personal tax account?

I find it useful as you can provide HMRC with your own estimates of income from various sources, update other information and monitor tax code(s) in use.

Is it via messaging on the HMRC site once in your personal account page?

Would you do this at the start of a new financial year just to give them a heads up on what you anticipate you will receive - or, after you've received it?

There is no point waiting until after you receive it, as they will know about that anyway.

An estimate may be used to change your tax code.

Remember that a tax code is only an attempt by HMRC to collect the right amount of tax.

The definitive calculation will only happen after the tax year is finished.1 -

My latest round of updating my income has resulted in several new tax codes. By the end of the tax year I'll still owe HMRC about £500 by the looks of things, but on a positive all my 40% tax will have been claimed back, the £500 representing exam marking where I haven't yet been taxed.

Tomorrow morning any unmarked scripts become available for pool marking, which has a 25% incentive. HMRC have now given my examiner job a 40% code so any extra marking will end up reducing the amount I owe HMRC as well as providing additional income.

To cut a long story short, if I can mark £200 worth tomorrow, I'll pay £80 in tax which will reduce the tax owed by £40 and gain another £120.

It's all so complicated at times!

0 -

Well it turns out I had misread my new tax codes. HMRC are leaving my exam marking untaxed and have given me extra tax relief on my pension contributions, meaning by the end of the financial year I'll owe them £1,000.

I do wonder what is the point of giving them accurate information for PAYE when in reality I'm in exactly the same situation as when I hadn't informed them.

My exam marking brings in approx £4k pa. It should be taxed at 40% but isn't taxed at all. I pay it all into my private pension so in effect I get all the 40% tax back. As I've not been taxed on it, I then have to pay 20% tax which accounts for £800 of the £1000 I owe HMRC.

I suppose I should be grateful for the 40% tax relief meaning this year's contributions have been boosted greatly but will of course benefit when I take them out with a tax free element with the remainder taxed at 20%.

No wonder people find it complicated!!!3 -

Well it turns out the info I got in the HMRC app is incorrect. (See pic).

CD0X is taxed at 40% not the 0% as in the pic.

It will reduce the amount I owe HMRC at the end of the financial year so it's not a problem. Just annoying that the information is incorrect.

0 -

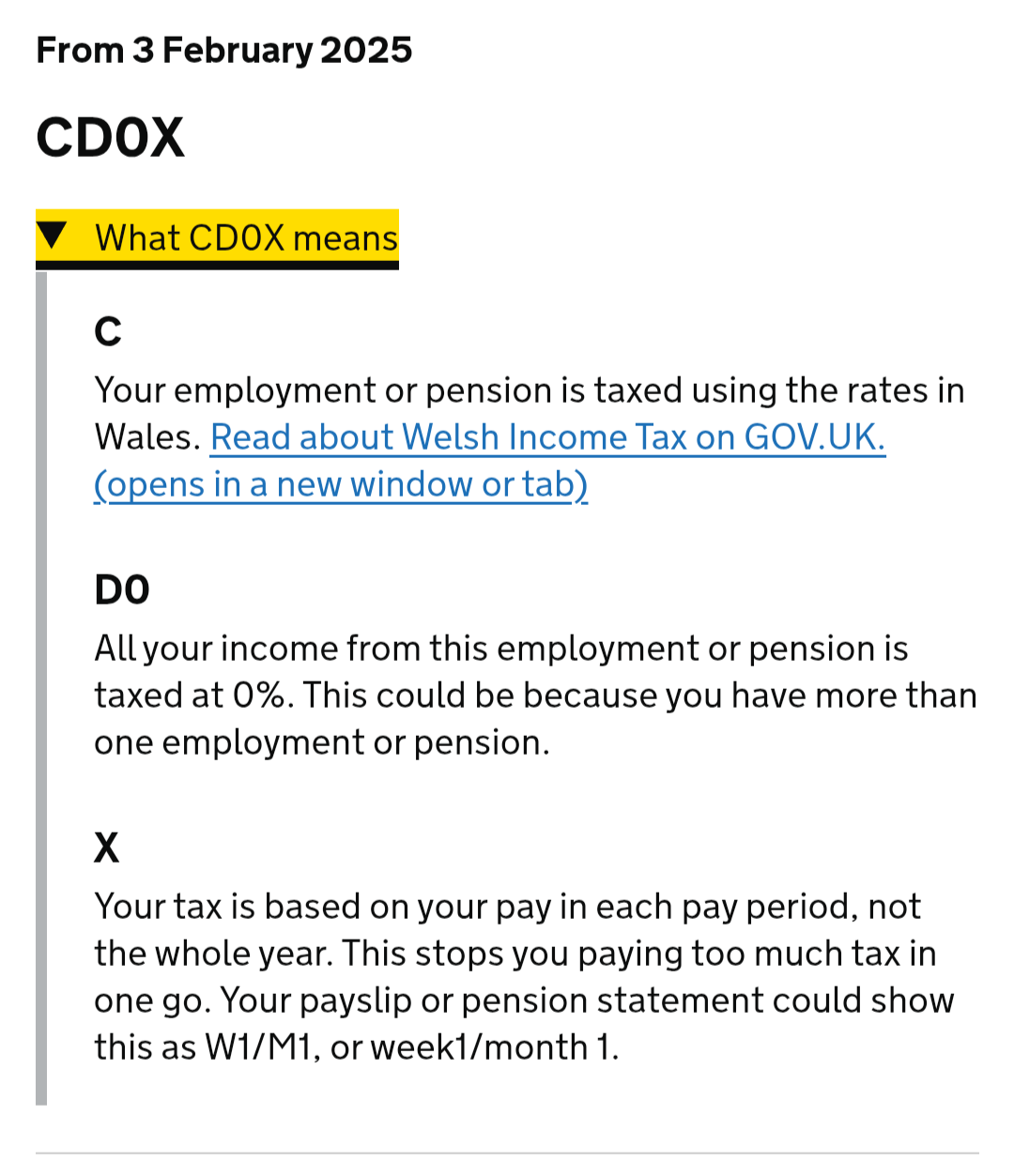

I have just received a new tax code.

These codes are confusing. CD0 means you are taxed at the higher (40%) rate in Wales, but SD0 means I am taxed at the intermediate rate (21%) in Scotland.

I've just found an accountancy website saying a D0 code always means you are taxed at the 40% rate, but it doesn't for me.0 -

Here's a breakdown.

https://www.gov.uk/tax-codes/what-your-tax-code-means

My budgeting spreadsheet gets ever more complicated!!!

0 -

Just to mention How Much To Live on

!

!

Just had a few moments to calculate how much I really need to live my lifestyle at the moment.

The figure is £20256 without holidays and about £23000 with some trips. The figures include everything (all bills, personal spending, annual costs etc...) apart from adding to long term savings.

As always any number is going to be personal and related to preferred lifestyle.

I do not smoke or drink alcohol. No debt and no rent or mortgage to pay.

Fortunately my total pension income exceeds the above figure by a margin so I do add to savings each month. (Which I need to do lol!)1 -

It is a personal matter and everyone has different priorities. We are fortunate to have no debt and no mortgage. Paid off a long time ago. These days we spend our money on a mixture of wants and needs. Needs are obviously household bills etc. Wants are far more varied - we have various vehicles which have to be taxed, tested and insured and maintained. We like attending local auctions and making purchases. We don't eat out much - but can afford to when we want. Not bothered about foreign travel much now, although we may go on a motorcycle tour of Spain or France next year. We don't really drink much now - the odd bottle of wine or Belgian Beer. We do save money each month too. We like good food and good company. We are fortunate that our pensions and savings well exceed our outgoings but do still like a bargain now and again.0

-

Are these the "gold plated pensions" the telegraph constantly bangs on about! ;-)

I'll bite my tongue now otherwise I'll start ranting.1 -

My 'gold-plated (public sector) pension' was earned by working very hard for 42 years in challenging educational environments.

Most of my lifelong friends receive private sector DB and/or DC based pension income that is up to four times mine!

However, certain publications only ever see the other side.

For example, Do they really begrudge anybody a guaranteed index linked pension income of just a few thousand a year to those heroes (in my mind anyway) who spent years cleaning hospital toilets and wards for little more than the minimum wage?

Like @Organgrinder I will say no more as I wish to stay calm!5

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards