We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Suggestions for a speculative punt?

Comments

-

Ditto to what badger said above. Like him, I meant no impoliteness----but sometimes you see "War & Peace" and recall suddenly why you disliked it so much at school. My apologies --and good luck.1

-

Far more sensible to put your money here.

https://www.wisdomtree.eu/en-gb/etfs/thematic/wcld---wisdomtree-cloud-computing-ucits-etf---usd-acc

Fastly is the top holding.The fascists of the future will call themselves anti-fascists.1 -

A punt... i know nothing about them but they have appeared in SMT'S top ten and they probably know more than most about upcoming companies...'Meituan Dianping'0

-

The news about Tik Tok sounds like a very good reason to avoid this investment.GMNN said:Been lurking on this thread for a while and appreciate reading people's views and ideas on speculative punts.

I just invested ~£6k in Fastly yesterday and would like to hear your thoughts. Let me tell you my rationale and then you can critique it.

SNIP

2- Trump issued an executive order to ban Tik Tok from operating in the US, as long as they are owned by a Chinese company. On the Q2 call, Fastly disclosed that Tik Tok was their largest customer, accounting for 12% of their revenue in 1H20, with 50% of that coming from the US. Now, Microsoft is in talks to buy Tik Tok, which would remove the ban threat, but that wouldn't really help Fastly either since in all likelihood Microsoft would move Tik Tok over to their own Azure cloud (they wouldn't stay in business with a competitor, albeit an indirect and much smaller one). So it's a lose-lose situation for Fastly, unless another US company emerges as the buyer for Tik Tok US, which seems unlikely at this point.

0 -

GMNN said:Been lurking on this thread for a while and appreciate reading people's views and ideas on speculative punts.

I just invested ~£6k in Fastly yesterday and would like to hear your thoughts. Let me tell you my rationale and then you can critique it.

You might have heard about Fastly already as it was one of the hottest tech stocks of the 2nd quarter. It went from ~$20 to ~$100 in the span of 2 months (early May to early July) after they released their Q1 earnings.. I've been watching the stock these last couple of months and finally decided to pull the trigger yesterday after the price pulled back ~1/3 from its ATH at $117 in the span of 3 days!

Fastly is a content delivery network (CDN) vendor harnessing the power of cloud edge computing to deliver improved performance of web services for its customers. Instead of having a handful of huge data centers like the "traditional" CDN providers, Fastly has a larger network of smaller but strategically-placed next-gen data centers, physically located much closer to the end users actually accessing those web services. I'm not going to pretend I understand everything about content delivery infrastructure / software, page load times, cache hit ratios, latency etc.. but I've done enough research to know that combining the geographical distribution aspect of their data center network along with (as yet) unmatched technology deployment provides Fastly with a superior value proposition.

I suggest you do more research if it sounds interesting (lots of articles out there better explain what they do), but for me the 2 things which stood out were the cloud edge concept and Fastly's technology. I read a lot of comments from developers / engineers who understand the technical aspects, and one quote which resonates with me is "The future of IT is the cloud, and the future of the cloud is the edge". While "the cloud" has been around for a while now, this concept of "cloud edge" is still relatively new and this part of the industry is in its nascent stage with lots of further growth in the years ahead. Many developers / engineers were also praising Fastly's product offering, comparing their technology to the latest iPhone/Android (or whichever latest phone you think is best!), whereas their closest competitor Cloudflare is probably more like a 3-5 year old iPhone, and the major legacy CDN providers like Akamai is the equivalent of 90's Nokia... Fastly was created by developers for developers, and they hands-down provide the best performance in terms of speed, stability, reliability for web services for companies which truly care about these things. Granted, it seems their product is not the most user-friendly (it's not meant to be used for mom & pop websites!) and their fees command a premium vs alternative offerings, so I think they will struggle to attract smaller companies who might not have the IT resources & knowhow to deploy and maintain such technology, which is why Fastly seems to be focusing more on large enterprise customers.

For now, they still have a very small share of their overall addressable market. They're competing with the big cloud boys (Amazon AWS, Microsoft Azure, Google Cloud who are all also ramping up their cloud edge capabilities), the legacy CDN vendors (Akamai, Limelight Networks...), and their closest competitor Cloudflare which is also a fast-growing tech company in the cloud edge CDN space and currently has a much bigger market share than Fastly.

Cloud edge CDN applications are numerous and fast-growing; think streaming (music, tv/films, live sports...), social media, e-commerce, online gaming, digital media (news outlets, videoconferencing...). I think Cloudflare also has great potential and will do very well, but the reason I chose Fastly instead was because I like the idea of investing in the best technology offering and betting on their customers doing well. A notable difference is that Fastly charges fees based on their customer's traffic volumes whereas Cloudflare mainly charges flat-fees for their products / services. So Cloudflare is more interested in signing-up more customers whereas Fastly has an incentive to drive up traffic for their existing clients, which they do by providing the best-available speed & performance. If their customers do well, then so does Fastly, which is why they have excellent customer service, and also why the stock has seen a surge during the Covid stay-at-home period. Look at Fastly's client list (some notable ones are Shopify, Tik Tok, Reddit, Spotify, Slack, Deliveroo, Rakuten, Twitter, New York Times, Financial Times, Buzzfeed, Vimeo...), most of them will have done well during the pandemic, but they will still continue to grow even if / when we all go back to the office and life goes back to "normal". Lots of tech stocks have seen huge ramp-ups in the last few months, and some might well come back down once life goes back to normal, but I don't think internet usage in the applications I've listed above are going to take a hit in a post-Covid world.

Now, why did I finally pull the trigger yesterday? Obviously I would have loved to jump in 3 months ago when the stock was at $20 but I missed that boat and watched the stock skyrocket. The valuation quickly became ridiculous and I couldn't justify parking money there. I was also waiting for the Q2 earnings call on Wednesday night to confirm they were the real deal, and the huge drops on Thursday and Friday provided the entry point I was looking for. There were 2 reasons why the stock dropped these last couple of days:

1- Expectations were huge for their Q2 results, and even though Fastly delivered higher revenue (62% y-o-y increase) and higher EPS (actually delivering a small operating income vs expected loss) than consensus analyst expectations, the "beat" wasn't as large as some were hoping for. The company actually improved on profitability metrics and management also raised their guidance for Q3 outlook, but again, apparently not as much as analysts were hoping for with their sky-high expectations.

2- Trump issued an executive order to ban Tik Tok from operating in the US, as long as they are owned by a Chinese company. On the Q2 call, Fastly disclosed that Tik Tok was their largest customer, accounting for 12% of their revenue in 1H20, with 50% of that coming from the US. Now, Microsoft is in talks to buy Tik Tok, which would remove the ban threat, but that wouldn't really help Fastly either since in all likelihood Microsoft would move Tik Tok over to their own Azure cloud (they wouldn't stay in business with a competitor, albeit an indirect and much smaller one). So it's a lose-lose situation for Fastly, unless another US company emerges as the buyer for Tik Tok US, which seems unlikely at this point.

With the stock price falling down to the $75-80 range I jumped in with my investment. I'm comfortable with the 1st reason; for me that's just a short-term correction with people taking profits from an insane (and unjustifiable) valuation when the stock was trading close to $120, with a much higher price/sales ratio than any of their peers. The 2nd reason is more worrying, but again this is a short-term issue. I don't think the potential of Fastly losing 6% of their revenue warrants such a big correction. I'm confident the company will offset the loss with their many other fast-growing customers.

The stock is now trading close to the rest of the hyped-up tech stocks in terms of financial metrics, so would not be considered "overvalued" compared to other companies in this sector.. Of course, you could argue the whole tech industry, in particular cloud / SaaS / e-commerce, is in a bubble and it could all come crashing down some day, but I feel long-term it will continue to do well. At the current price, Fastly has an ~$8B market cap, and I think they will close the gap and eventually surpass Cloudflare's ~12B value as they have more growth potential and will grab more market share, though as I said before I think both companies will grow quickly in the coming years.

The other reason which prompted my decision was that the stock seems to have technical support in the mid-70's, so entering in the $75-80 range where it was trading yesterday makes sense to me. If it breaks that support, it could take a big jump down, in which case I would double-down on my investment, but I would be very surprised to see it break below $70, which limits the downside risk (famous last words!).

I will stay with Fastly for at least 3 years, at which point I will reassess and decide whether to stay invested longer or move my money somewhere else (if I think there is a better opportunity at that time). My price target is 400$ (i.e. 5x today's price) which I think is a stretch but a $40B valuation in 3 years is not ridiculous in my opinion considering their potential. No matter what, I will hold for at least 3 years, even if the stock skyrockets again. You don't want to be the guy who invested in AMZN at $200 in 2012 and thinks he's a genius for selling at $1,000 in 2017 (when the stock is now $3,000+...) or TSLA from $200 to $1600 in 2 years!

So, if you've read this far, please tell me why I'm wrong, why this stock will not do well and why I just threw my £6k down the drain.I have a small position in Fastly. It is good growth Company. Jim Cramer's from CNBC has done the deskwork for you. But I am not suggesting people to follow him blindly without doing his own due dilligence and research. Also keep in mind his recomendation is before the recent news about TikTok is coming.About the Risk assessment is here:Each to his own, but I never buy shares in one go, I manage to cost averaging "fastly" down to US$79.30. I think it is quite risky to put £6k in one go. The lesson I have learnt from other people is that better to put 40%-50% (say). If you put all your money (100%) you have no chance to cost avaraging down rather than waiting until the price is working toward your favour. It could be very frustrating and depressing seeing your wealth keep depreciating on day by day basis which could make you give up and selling it at loss. If you put part of it you have the chance to keep averaging down every time the price falls below your current price. Othersse you couod use half of the funding for another venture.It was falling from the recent long time high on 04/08/2020 @US$116,18 to US$ 79,.33 on the market closed on 07/08/2020.

Here is my take:

- I have not heard news regarding the "fundamental change".

- Recent News: https://www.nasdaq.com/market-activity/stocks/fsly/press-releases

- There are many institutional ownership including well known such as: The Vanguard Group, Fidelity , Morgan Stanley, Goldman Sachs

- No inside acticity recently in August https://www.nasdaq.com/market-activity/stocks/fsly/insider-activity . If there is massive sell off from insider, better to be extremely careful as they might have information other people do not have.

- Record Growth Driven by Strong Execution Revenue up 62% Year-over-Year;

https://investors.fastly.com/files/doc_financials/2020/q2/2Q20-Shareholder-Letter.pdfI think It is in the headlines now because of the sentiment due to TikTok uncertainty. I believe If they get a little good news boost, It might make a good jump. Let see, it might be just a few weeks waiting when they come back to the long time high. By that time you will already make 31.71% gain if you sell it. But of course it could also mean losing money when it goes further down. Given no fundamental change and the current price already priced aginst the sentiment the chance to drop another 31.71% is very low. If it ever falls again 10% (say), the Reward/Risk ratio of 3 to 1 is already working toward your favour. Also do not forget that if you still allocate funding for this stock you could still cost averaging down.

If the stock is fundamentally good than bad news is your friend.

Warren Buffet: ‘Be greedy when others are fearful’

Warning: I am not here recommending to buy/sell this stock. To invest please do your own due diligence and do it with your own risk.

1 -

People shouldn't follow him at all. He's a vaguely entertaining TV host who draws enough viewers to maintain an advertising revenue for his employer. Maybe he's got a knack for picking winners and works for CNBC out of pure altrusism but he's just a salesman.adindas said:GMNN said:Been lurking on this thread for a while and appreciate reading people's views and ideas on speculative punts.

I just invested ~£6k in Fastly yesterday and would like to hear your thoughts. Let me tell you my rationale and then you can critique it.

You might have heard about Fastly already as it was one of the hottest tech stocks of the 2nd quarter. It went from ~$20 to ~$100 in the span of 2 months (early May to early July) after they released their Q1 earnings.. I've been watching the stock these last couple of months and finally decided to pull the trigger yesterday after the price pulled back ~1/3 from its ATH at $117 in the span of 3 days!

Fastly is a content delivery network (CDN) vendor harnessing the power of cloud edge computing to deliver improved performance of web services for its customers. Instead of having a handful of huge data centers like the "traditional" CDN providers, Fastly has a larger network of smaller but strategically-placed next-gen data centers, physically located much closer to the end users actually accessing those web services. I'm not going to pretend I understand everything about content delivery infrastructure / software, page load times, cache hit ratios, latency etc.. but I've done enough research to know that combining the geographical distribution aspect of their data center network along with (as yet) unmatched technology deployment provides Fastly with a superior value proposition.

I suggest you do more research if it sounds interesting (lots of articles out there better explain what they do), but for me the 2 things which stood out were the cloud edge concept and Fastly's technology. I read a lot of comments from developers / engineers who understand the technical aspects, and one quote which resonates with me is "The future of IT is the cloud, and the future of the cloud is the edge". While "the cloud" has been around for a while now, this concept of "cloud edge" is still relatively new and this part of the industry is in its nascent stage with lots of further growth in the years ahead. Many developers / engineers were also praising Fastly's product offering, comparing their technology to the latest iPhone/Android (or whichever latest phone you think is best!), whereas their closest competitor Cloudflare is probably more like a 3-5 year old iPhone, and the major legacy CDN providers like Akamai is the equivalent of 90's Nokia... Fastly was created by developers for developers, and they hands-down provide the best performance in terms of speed, stability, reliability for web services for companies which truly care about these things. Granted, it seems their product is not the most user-friendly (it's not meant to be used for mom & pop websites!) and their fees command a premium vs alternative offerings, so I think they will struggle to attract smaller companies who might not have the IT resources & knowhow to deploy and maintain such technology, which is why Fastly seems to be focusing more on large enterprise customers.

For now, they still have a very small share of their overall addressable market. They're competing with the big cloud boys (Amazon AWS, Microsoft Azure, Google Cloud who are all also ramping up their cloud edge capabilities), the legacy CDN vendors (Akamai, Limelight Networks...), and their closest competitor Cloudflare which is also a fast-growing tech company in the cloud edge CDN space and currently has a much bigger market share than Fastly.

Cloud edge CDN applications are numerous and fast-growing; think streaming (music, tv/films, live sports...), social media, e-commerce, online gaming, digital media (news outlets, videoconferencing...). I think Cloudflare also has great potential and will do very well, but the reason I chose Fastly instead was because I like the idea of investing in the best technology offering and betting on their customers doing well. A notable difference is that Fastly charges fees based on their customer's traffic volumes whereas Cloudflare mainly charges flat-fees for their products / services. So Cloudflare is more interested in signing-up more customers whereas Fastly has an incentive to drive up traffic for their existing clients, which they do by providing the best-available speed & performance. If their customers do well, then so does Fastly, which is why they have excellent customer service, and also why the stock has seen a surge during the Covid stay-at-home period. Look at Fastly's client list (some notable ones are Shopify, Tik Tok, Reddit, Spotify, Slack, Deliveroo, Rakuten, Twitter, New York Times, Financial Times, Buzzfeed, Vimeo...), most of them will have done well during the pandemic, but they will still continue to grow even if / when we all go back to the office and life goes back to "normal". Lots of tech stocks have seen huge ramp-ups in the last few months, and some might well come back down once life goes back to normal, but I don't think internet usage in the applications I've listed above are going to take a hit in a post-Covid world.

Now, why did I finally pull the trigger yesterday? Obviously I would have loved to jump in 3 months ago when the stock was at $20 but I missed that boat and watched the stock skyrocket. The valuation quickly became ridiculous and I couldn't justify parking money there. I was also waiting for the Q2 earnings call on Wednesday night to confirm they were the real deal, and the huge drops on Thursday and Friday provided the entry point I was looking for. There were 2 reasons why the stock dropped these last couple of days:

1- Expectations were huge for their Q2 results, and even though Fastly delivered higher revenue (62% y-o-y increase) and higher EPS (actually delivering a small operating income vs expected loss) than consensus analyst expectations, the "beat" wasn't as large as some were hoping for. The company actually improved on profitability metrics and management also raised their guidance for Q3 outlook, but again, apparently not as much as analysts were hoping for with their sky-high expectations.

2- Trump issued an executive order to ban Tik Tok from operating in the US, as long as they are owned by a Chinese company. On the Q2 call, Fastly disclosed that Tik Tok was their largest customer, accounting for 12% of their revenue in 1H20, with 50% of that coming from the US. Now, Microsoft is in talks to buy Tik Tok, which would remove the ban threat, but that wouldn't really help Fastly either since in all likelihood Microsoft would move Tik Tok over to their own Azure cloud (they wouldn't stay in business with a competitor, albeit an indirect and much smaller one). So it's a lose-lose situation for Fastly, unless another US company emerges as the buyer for Tik Tok US, which seems unlikely at this point.

With the stock price falling down to the $75-80 range I jumped in with my investment. I'm comfortable with the 1st reason; for me that's just a short-term correction with people taking profits from an insane (and unjustifiable) valuation when the stock was trading close to $120, with a much higher price/sales ratio than any of their peers. The 2nd reason is more worrying, but again this is a short-term issue. I don't think the potential of Fastly losing 6% of their revenue warrants such a big correction. I'm confident the company will offset the loss with their many other fast-growing customers.

The stock is now trading close to the rest of the hyped-up tech stocks in terms of financial metrics, so would not be considered "overvalued" compared to other companies in this sector.. Of course, you could argue the whole tech industry, in particular cloud / SaaS / e-commerce, is in a bubble and it could all come crashing down some day, but I feel long-term it will continue to do well. At the current price, Fastly has an ~$8B market cap, and I think they will close the gap and eventually surpass Cloudflare's ~12B value as they have more growth potential and will grab more market share, though as I said before I think both companies will grow quickly in the coming years.

The other reason which prompted my decision was that the stock seems to have technical support in the mid-70's, so entering in the $75-80 range where it was trading yesterday makes sense to me. If it breaks that support, it could take a big jump down, in which case I would double-down on my investment, but I would be very surprised to see it break below $70, which limits the downside risk (famous last words!).

I will stay with Fastly for at least 3 years, at which point I will reassess and decide whether to stay invested longer or move my money somewhere else (if I think there is a better opportunity at that time). My price target is 400$ (i.e. 5x today's price) which I think is a stretch but a $40B valuation in 3 years is not ridiculous in my opinion considering their potential. No matter what, I will hold for at least 3 years, even if the stock skyrockets again. You don't want to be the guy who invested in AMZN at $200 in 2012 and thinks he's a genius for selling at $1,000 in 2017 (when the stock is now $3,000+...) or TSLA from $200 to $1600 in 2 years!

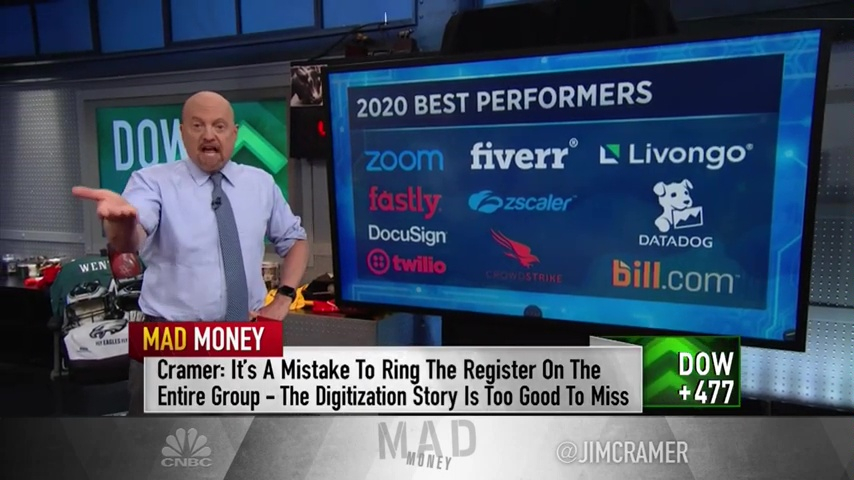

So, if you've read this far, please tell me why I'm wrong, why this stock will not do well and why I just threw my £6k down the drain.Jim Cramer's from CNBC has done the deskwork for you. But I am not suggesting people to follow him blindly without doing his own due dilligence and research. Also keep in mind his recomendation is before the recent news about TikTok is coming.

Also beware of anyone that has to get up at 4am so they can appear on Bloomberg.1 -

Sailtheworld said:

People shouldn't follow him at all. He's a vaguely entertaining TV host who draws enough viewers to maintain an advertising revenue for his employer. Maybe he's got a knack for picking winners and works for CNBC out of pure altrusism but he's just a salesman.adindas said:Jim Cramer's from CNBC has done the deskwork for you. But I am not suggesting people to follow him blindly without doing his own due dilligence and research. Also keep in mind his recomendation is before the recent news about TikTok is coming.

Also beware of anyone that has to get up at 4am so they can appear on Bloomberg.If a person says jump, did you jump straight away ?? It is always a common sense not to follow people blindly without doing your own research/ due diligence. Also, their recommendation might not be suitable to your risk attitude.

But suggesting people to avoid him at all is absurd, thus subject to debate. What about millions of people around the world who have been watching his shows since March, 2005. Do you think people will keep watching his show if they keep losing money following his recommendation? Do you think CNBC will keep his show for such a long time if the number of audience keep falling, if there are a lot of complain from people keep losing money ?

If you want to do a research, have a look on his COVID-19 Stay at home / working from home stocks recommendation, Cramer's COVID-19 index and compare it with the S&P 500 return. I remember a person on you tube has done a comparison. You just need searching and find it out.

Also, keep in mind at CNBC there are lot of wall street analysts, hedge funds managers appear in other Q&A programs such as #AskHalftime that you could watch to be used as a comparison.

0 -

To be fair he was advocating selling Stark Industries stock as well....."It is prudent when shopping for something important, not to limit yourself to Pound land/Estate Agents"

G_M/ Bowlhead99 RIP0 -

adindas said:

I have a small position in Fastly. It is good growth Company. Jim Cramer's from CNBC has done the deskwork for you.

You keep pumping the fact that Cramer and CNBC are analysts doing work for you, but the desk-work they are doing is bringing a stock to your attention, not giving you meaningful insight. As you say, you have to do your own research. He is wealthy but his current job is not analyst - instead, a TV personality whose his job is to fill airtime and make things sound exciting or interesting.Get real. This is not a 'risk assessment' in any conventional sense of the word. Risk assessments are carried out by professional investors and investment managers using complex models. Whereas this is advertorial for Motley Fool who use clickbait to sell stock tips newsletters.

It starts with a question in its opening paragraph 'has the stock become too risky'. Its closing paragraph says that 'it may now be too risky'. So, is it risky or not? There is little insight, and they answer their own question 'has it?' with 'may be'. It stops short of saying yes, because they don't want to be called out on it if the company is a screaming success.

The purpose of the article is to highlight a company that people are talking about and sow doubt in your mind that it may be too risky so that you will be interested in their 'real' closing paragraph, entitled '10 stocks we like better than Fastly', where they inform you that their 'investing geniuses' have 'just revealed' the best 10 stocks to buy, and you can find out all about them if you click through to their website and sign up to a newsletter.

Obviously they are not going to really tell you with complete independence of mind the 10 very best stocks for investors to buy; it is just more clickbait to support their vested interests (Motley Fool Stock Advisor, advertised in the concluding paragraph of this piece, is a tipsheet that they sell for $99 a year).

The fact that it is being run on the Nasdaq.com / Articles website and the Nasdaq is a competent organisation which runs a stock exchange, should not distract you from the fact that the purpose of Motley Fool articles is to take basic publicly available information about companies and package it into articles to sell subscriptions to newsletters that take basic publicly available information about companies and package it into articles. It is quite far removed from a 'risk assessment' that would be carried out by a fund manager or investment professional.

Presumably if their 'risk assessment' actually did a good job of being a risk assessment it would need to be run again now anyway because the largest customer first faced having its US operations banned and then received a takeover offer from a competing cloud computing service provider with deep pockets. Your 'risk assessment' published 7 July mentioned that they had 1800 customers but didn't think to mention the concentration risk of over 12% of the revenue over the six months to June coming from that one customer, nor the fact that on 6 July Secretary of State Mike Pompeo had said that the United States is “certainly looking at” banning Chinese social media apps, including Tik Tok. Per Reuters: “I don’t want to get out in front of the President, but it’s something we’re looking at,” Pompeo said in an interview with Fox News.

I agree with your ethos of saying that the stocks you mention are not recommendations and that people should do their own research. I do have some concern for you that the sources you use for your research are totally inadequate, so your investments are guesses at best. Still, that's fine for a 'speculative punt' thread I suppose.Given no fundamental change and the current price already priced aginst the sentiment the chance to drop another 31.71% is very low. If it ever falls again 10% (say), the Reward/Risk ratio of 3 to 1 is already working toward your favour. Also do not forget that if you still allocate funding for this stock you could still cost averaging down.What 'reward / risk ratio of 3 to 1?' A stock always has the chance to go up 100x over a long enough timescale. Is that a 100 to 1 reward to risk ratio? Some arbitrary view of 'reward to risk' based on its previous peak does not make a lot of sense. And yes if you put some money in a stock and it gets cheaper you could always put more money in the stock if you can't find anything more attractive to buy, though in a great many cases you could find something more attractive to buy instead if you were willing to look for it.3 -

The market hears whatever comes out of his mouth, digests it, and spits out a price adjustment accordingly. You can't buy yesterday's news. If he's made some good stock picks that's great but doesn't it make you wonder why he isn't as rich as Croesus if he's so good?adindas said:Sailtheworld said:

People shouldn't follow him at all. He's a vaguely entertaining TV host who draws enough viewers to maintain an advertising revenue for his employer. Maybe he's got a knack for picking winners and works for CNBC out of pure altrusism but he's just a salesman.adindas said:Jim Cramer's from CNBC has done the deskwork for you. But I am not suggesting people to follow him blindly without doing his own due dilligence and research. Also keep in mind his recomendation is before the recent news about TikTok is coming.

Also beware of anyone that has to get up at 4am so they can appear on Bloomberg.If a person says jump, did you jump straight away ?? It is always a common sense not to follow people blindly without doing your own research/ due diligence. Also, their recommendation might not be suitable to your risk attitude.

But suggesting people to avoid him at all is absurd, thus subject to debate. What about millions of people around the world who have been watching his shows since March, 2005. Do you think people will keep watching his show if they keep losing money following his recommendation? Do you think CNBC will keep his show for such a long time if the number of audience keep falling, if there are a lot of complain from people keep losing money ?

If you want to do a research, have a look on his COVID-19 Stay at home / working from home stocks recommendation, Cramer's COVID-19 index and compare it with the S&P 500 return. I remember a person on you tube has done a comparison. You just need searching and find it out.

Also, keep in mind at CNBC there are lot of wall street analysts, hedge funds managers appear in other Q&A programs such as #AskHalftime that you could watch to be used as a comparison.

Yes I do think people will keep watching CNBC/ Bloomberg whether they lose money or not. I watch both a little but not for stock picking tips - more for the business news than anything else. The commentary is interesting but there's usually no consensus on why something has just happened let alone what will happen next.

I know it's quite compelling to think there's someone we can turn to who can tell us what the future holds on TV but it doesn't work like that. Most fund managers can't beat the market over time and they do it for a living so what chance you, me or a TV presenter being any better.

Follow the money and motivations become clear. Lots of profit centres and they're all predicated on the fallacy that you can either pick winners yourself or find someone that can do so on your behalf. Fortunately markets tend to rise over time which makes investment gods of us all.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards