We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Do you think First Direct will reopen to new customers in 2020?

Comments

-

All banks have their own unpublished criteria for the processing of applications for new accounts and/or credit. First Direct aren't different in that regard.mrkds said:

Thanks. Gave them a ring. Just said I didn't meet their eligibility criteria. Wouldn't give me any further information. So they have a set of hidden criteria that is different to the one they publish on their website. Quite frustrating. 🙁ischris85 said:Number for new customers - 0800 917 24241 -

If we are unable to accept your application, we will tell you. We will also tell you the main reason why we were unable to agree to your request, for example, if you do not pass our credit score we will tell you.

If we have declined your application you may contact us and ask us to reconsider our decision. We will usually ask you to provide additional information, which was not available at the time your original application was submitted.

When you apply for some products, we may be able to provide you with a decision straight away without referring you to a member of our staff. This is called an automated decision. If we decline your application in this way, you will have a right to ask for your application to be reviewed by a member of our staff.

If you wish to ask us to reconsider our decision then please call us using the number on the back of this document and we will review your application and tell you how long it will take until you receive a response.

If following the appeal you are still unhappy with the response you have received, you should write to:

Customer Relations Team

first direct

40 Wakefield Road

Leeds

LS98 1FD

1 -

To update I've also been turned for an account with FD, even though I was a customer of theirs only 1 year ago. I would like to appeal this decision however, I'm not sure what additional information I could provide.0

-

I guess its worth getting them to have a human reconsider your application. Maybe having had an account so recently closed may be an issue. I gave up with FD and tried M&S. Not ideal as they require you to switch and have direct debits set up which s more faff, but they seem to be less picky than FD - they have requested evidence documents which is a good sign

") 1

1 -

mrkds said:I guess its worth getting them to have a human reconsider your application. Maybe having had an account so recently closed may be an issue. I gave up with FD and tried M&S. Not ideal as they require you to switch and have direct debits set up which s more faff, but they seem to be less picky than FD - they have requested evidence documents which is a good sign

Also got turned down by M&S

0 -

Those criteria you posted are the very basic , that has to be met in order to go through FD internal credit scoring. They are known to be picky and the reason they have turned you down is - you did not meet their eligibility criteria ( e.a. their internal credit scoring ). As that is a valid reason you can complain but I can't see much of a point in doing so. Also bear in mind that saving account is only for up to 300 a month for 1 year so even though % seems fantastic it doesn't come to much on 3600 a year with interest calculated daily it comes to about £ 50 after 12 months. Not that I'm saying that's bad , but not the end of the world after all. FD other saving accounts are how to put it mildly.. " not quite so competitive " and if only reason for opening their account is access to regular saving account, might be just easier to cross them out and open normal saving account in a building society, if you can park whole £ 3600 and leave it there for a year ( so whole 3600 can accrue interest from day 1 ) there won't be much of a difference compared to FD saver. I know it ,I have both, but FD only allows 300 per month maximum and 12 months max again, so as much as headline % is good and I do use it for a year ( as I have DD with FD and run their current account, might as well use it while it's there ) , after that it goes to Marcus or building society account to be with the rest of the savings.2

-

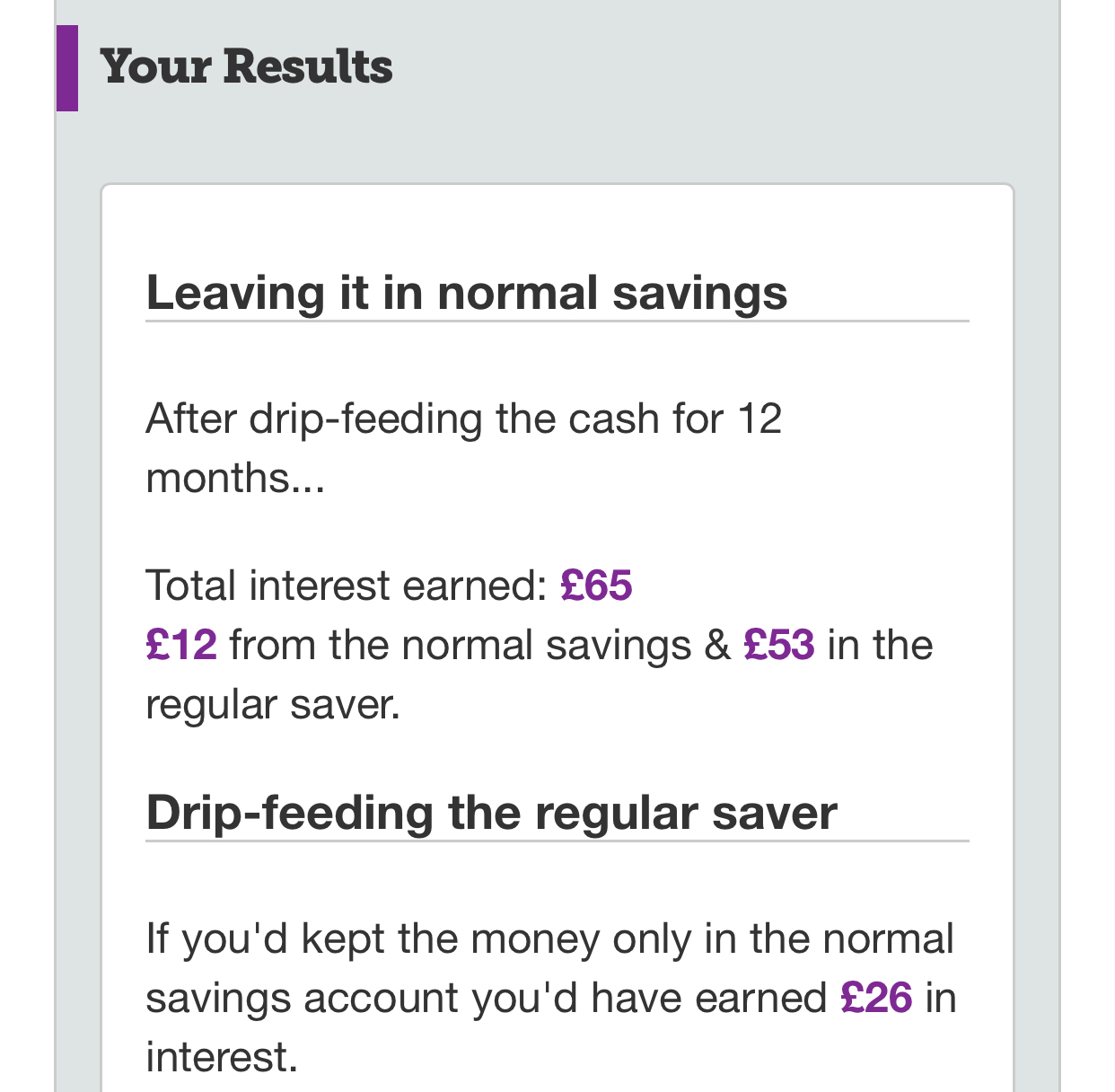

This is MSE and many forumites try to maximise their returns from their savings, so they do care about the odd £30 or £40 extra interest. After all, this means they are beating the current inflation by a wide margin.

Below the calculations for drip-feeding 12 x £300 from a 0.7% instant access account to a 2.75% regular saver. 0.7% is as good as it gets for Marcus instant access these days. But even if you have managed to maintain a 1.2% instant access account, it is still worth the 2.75% regular savers, IMO.

0 -

Colton - I do care ( within reason ) about £ 30 -40 ,what I meant is park whole 3600 into a building society or Marcus account and not drip feed it. If the poster got accepted for FD account then yes, use regular saver by all means. As he/she was turned down - I only stated that as much as headline % is good there is a difference between 2.75 % from the full amount for whole year and from drip fed ,% calculated daily. I have that FD and as I use their current account I use it too ( as clearly stated ) . But I would not spend hours and hours trying it again and again and ask for review and reconsideration if only reason I wanted FD account is access to a saving account. There are building societies with better % than Marcus and much higher acceptance rate than FD. I am not knocking off FD regular savers account and everyone who has one and is in position to save should use it too. All I am saying is that I would prefer to spend couple of hours earning money rather than trying to overturn a decision regarding FD account eligibility ( and most if not all of us would make more in that time than £ 30 ). FD is a decent account for most customers, their regular saving account is good in general, but I value my time too ( and most people do ) = so having a go and applying for one - yes, trying time and again to make them reconsider and emailing and calling - no, I'd accept their decision, move on and open something else instead.0

-

floppydisk1 said:Colton - I do care ( within reason ) about £ 30 -40 ,what I meant is park whole 3600 into a building society or Marcus account and not drip feed it.

That sounds as if you don't care.0 -

Name them please, for like to like accounts.floppydisk1 said:There are building societies with better % than Marcus3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards