7th Dec - AiP submitted

8th Dec - AiP accepted

11th Dec - Full application submitted

We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Kent reliance

Comments

-

I have no idea what that means either 😂 would be helpful if they were clearer! Can I ask, do you know when your valuation was completed? I am waiting to hear back about mine and just trying to get an idea of the timescale, thanks 😊adzharr91 said:

I mean O/Sadzharr91 said: itwe’ve had our valuation completed, I didnt even know they had booked us in for it and now they are asking for an S/O which i dont even know what that is 😂

0 -

They wanted to make sure nobody else was living with us wierdly! Our full submission went over to them on the 30th november, which is when we paid for it, they requested further docs on the 8th December and then the valuation was sent back to them today, but i honestly have no idea when they asked for it to be done or booked inSR100 said:

I have no idea what that means either 😂 would be helpful if they were clearer! Can I ask, do you know when your valuation was completed? I am waiting to hear back about mine and just trying to get an idea of the timescale, thanks 😊adzharr91 said:

I mean O/Sadzharr91 said: itwe’ve had our valuation completed, I didnt even know they had booked us in for it and now they are asking for an S/O which i dont even know what that is 😂

0 -

-

Well this is horrible.

I had a call from my old broker about affordability at Kent's rates and it has scared the living daylights out of me. My new broker had checked and I just fit on my new pay but now I'm really paranoid the HA will reject me... This stress is not good. Not good at all. Anyway:17th Dec - Assessment queue - 8 day wait to assessTBC...

17th Dec - Valuation instructed - 5 day wait to receive a date

Current debt-free wannabe stats:Credit card: £8,524.31 | Loan: £3,224.80 | Student Loan (Plan 1): £5,768.55 | Total: £17,517.66Debt-free target: 21-Mar-2027

Debt-free diary0 -

Didn't the HA do an affordability assessment using the AIP from Kent before you applied for the mortgage? If they did and your AIP is on the same rate as the mortgage you applied for then its unlikely they will reject you once you get a mortgage offer.annetheman said:Well this is horrible.

I had a call from my old broker about affordability at Kent's rates and it has scared the living daylights out of me. My new broker had checked and I just fit on my new pay but now I'm really paranoid the HA will reject me... This stress is not good. Not good at all. Anyway:7th Dec - AiP submitted

8th Dec - AiP accepted

11th Dec - Full application submitted17th Dec - Assessment queue - 8 day wait to assessTBC...

17th Dec - Valuation instructed - 5 day wait to receive a date0 -

They did the initial assessment with AiP from Leeds which was 2.4% pre-pandemic (I've been at this since beginning of March!!!), I initially was purchasing a higher percentage than I am now.aleeek said:

Didn't the HA do an affordability assessment using the AIP from Kent before you applied for the mortgage? If they did and your AIP is on the same rate as the mortgage you applied for then its unlikely they will reject you once you get a mortgage offer.annetheman said:Well this is horrible.

I had a call from my old broker about affordability at Kent's rates and it has scared the living daylights out of me. My new broker had checked and I just fit on my new pay but now I'm really paranoid the HA will reject me... This stress is not good. Not good at all. Anyway:7th Dec - AiP submitted

8th Dec - AiP accepted

11th Dec - Full application submitted17th Dec - Assessment queue - 8 day wait to assessTBC...

17th Dec - Valuation instructed - 5 day wait to receive a date

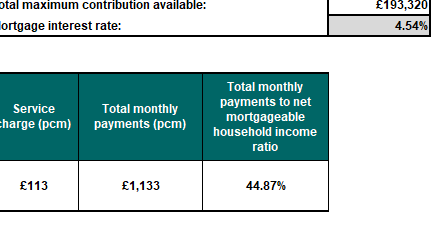

The Memorandum of Sale has been amended by the HA to a lower %age purchase and my new affordability calculation using the HA/Homes England calculator with Kent Reliance at the higher 4.54% rate looks like this:

Literally *just* affordable..... No room for any more movement here! Very tense moment of panic though. This affordability is with my contractual 10% annual bonus (paid end of financial year in April), though I've been with the company 1 year in Jan so first payment of the bonus is in April 2021, it was pro-rata'd in 2020!

I also didn't know that you actually have to purchase the highest percentage you can afford - so weirdly, this has worked out okay? So scary!

If Kent fails for whatever reason, and I can't get anything lower than 4.54%, the HA could very well say I'm no longer eligible.Current debt-free wannabe stats:Credit card: £8,524.31 | Loan: £3,224.80 | Student Loan (Plan 1): £5,768.55 | Total: £17,517.66Debt-free target: 21-Mar-2027

Debt-free diary0 -

Our affordability was just about there too. We got an AIP from Kent but the rate went up before we applied and the housing association was still fine with it, they approved our mortgage offer now. Don't worry too much!annetheman said:

They did the initial assessment with AiP from Leeds which was 2.4% pre-pandemic (I've been at this since beginning of March!!!), I initially was purchasing a higher percentage than I am now.aleeek said:

Didn't the HA do an affordability assessment using the AIP from Kent before you applied for the mortgage? If they did and your AIP is on the same rate as the mortgage you applied for then its unlikely they will reject you once you get a mortgage offer.annetheman said:Well this is horrible.

I had a call from my old broker about affordability at Kent's rates and it has scared the living daylights out of me. My new broker had checked and I just fit on my new pay but now I'm really paranoid the HA will reject me... This stress is not good. Not good at all. Anyway:7th Dec - AiP submitted

8th Dec - AiP accepted

11th Dec - Full application submitted17th Dec - Assessment queue - 8 day wait to assessTBC...

17th Dec - Valuation instructed - 5 day wait to receive a date

The Memorandum of Sale has been amended by the HA to a lower %age purchase and my new affordability calculation using the HA/Homes England calculator with Kent Reliance at the higher 4.54% rate looks like this:

Literally *just* affordable..... No room for any more movement here! Very tense moment of panic though. This affordability is with my contractual 10% annual bonus (paid end of financial year in April), though I've been with the company 1 year in Jan so first payment of the bonus is in April 2021, it was pro-rata'd in 2020!

I also didn't know that you actually have to purchase the highest percentage you can afford - so weirdly, this has worked out okay? So scary!

If Kent fails for whatever reason, and I can't get anything lower than 4.54%, the HA could very well say I'm no longer eligible.1 -

That is absolutely amazing news, congrats!aleeek said:

Our affordability was just about there too. We got an AIP from Kent but the rate went up before we applied and the housing association was still fine with it, they approved our mortgage offer now. Don't worry too much!annetheman said:

They did the initial assessment with AiP from Leeds which was 2.4% pre-pandemic (I've been at this since beginning of March!!!), I initially was purchasing a higher percentage than I am now.aleeek said:

Didn't the HA do an affordability assessment using the AIP from Kent before you applied for the mortgage? If they did and your AIP is on the same rate as the mortgage you applied for then its unlikely they will reject you once you get a mortgage offer.annetheman said:Well this is horrible.

I had a call from my old broker about affordability at Kent's rates and it has scared the living daylights out of me. My new broker had checked and I just fit on my new pay but now I'm really paranoid the HA will reject me... This stress is not good. Not good at all. Anyway:7th Dec - AiP submitted

8th Dec - AiP accepted

11th Dec - Full application submitted17th Dec - Assessment queue - 8 day wait to assessTBC...

17th Dec - Valuation instructed - 5 day wait to receive a date

The Memorandum of Sale has been amended by the HA to a lower %age purchase and my new affordability calculation using the HA/Homes England calculator with Kent Reliance at the higher 4.54% rate looks like this:

Literally *just* affordable..... No room for any more movement here! Very tense moment of panic though. This affordability is with my contractual 10% annual bonus (paid end of financial year in April), though I've been with the company 1 year in Jan so first payment of the bonus is in April 2021, it was pro-rata'd in 2020!

I also didn't know that you actually have to purchase the highest percentage you can afford - so weirdly, this has worked out okay? So scary!

If Kent fails for whatever reason, and I can't get anything lower than 4.54%, the HA could very well say I'm no longer eligible.

Thank you so much for the reassurance, it really means a lot... This is hella stressful lol! Hope you have a smooth sail over to your new home soon")

-AnneCurrent debt-free wannabe stats:Credit card: £8,524.31 | Loan: £3,224.80 | Student Loan (Plan 1): £5,768.55 | Total: £17,517.66Debt-free target: 21-Mar-2027

Debt-free diary0 -

All the best to you too! Your offer will be with you soonannetheman said:

That is absolutely amazing news, congrats!aleeek said:

Our affordability was just about there too. We got an AIP from Kent but the rate went up before we applied and the housing association was still fine with it, they approved our mortgage offer now. Don't worry too much!annetheman said:

They did the initial assessment with AiP from Leeds which was 2.4% pre-pandemic (I've been at this since beginning of March!!!), I initially was purchasing a higher percentage than I am now.aleeek said:

Didn't the HA do an affordability assessment using the AIP from Kent before you applied for the mortgage? If they did and your AIP is on the same rate as the mortgage you applied for then its unlikely they will reject you once you get a mortgage offer.annetheman said:Well this is horrible.

I had a call from my old broker about affordability at Kent's rates and it has scared the living daylights out of me. My new broker had checked and I just fit on my new pay but now I'm really paranoid the HA will reject me... This stress is not good. Not good at all. Anyway:7th Dec - AiP submitted

8th Dec - AiP accepted

11th Dec - Full application submitted17th Dec - Assessment queue - 8 day wait to assessTBC...

17th Dec - Valuation instructed - 5 day wait to receive a date

The Memorandum of Sale has been amended by the HA to a lower %age purchase and my new affordability calculation using the HA/Homes England calculator with Kent Reliance at the higher 4.54% rate looks like this:

Literally *just* affordable..... No room for any more movement here! Very tense moment of panic though. This affordability is with my contractual 10% annual bonus (paid end of financial year in April), though I've been with the company 1 year in Jan so first payment of the bonus is in April 2021, it was pro-rata'd in 2020!

I also didn't know that you actually have to purchase the highest percentage you can afford - so weirdly, this has worked out okay? So scary!

If Kent fails for whatever reason, and I can't get anything lower than 4.54%, the HA could very well say I'm no longer eligible.

Thank you so much for the reassurance, it really means a lot... This is hella stressful lol! Hope you have a smooth sail over to your new home soon

-Anne 1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards