We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

SLLM (Single Lady Large Mortgage)

Comments

-

@HelloB, that was good planning when you fixed for 5 years. It’s good that you managed to recover from the debt/divorce and you are now back ontop. WelldoneInitial mortgage bal £487.5k, current £238k, target £122k (quarter way!)

Mortgage start date first week of July 2019,

Mortgage term 23yrs(end of June 2042🙇🏽♀️),Target is to pay it off in 10years(by 2030🥳).MFW#10 (2022/23 mfw#34)(2021 mfw#47)(2020 mfw#136)

£12K in 2021 #54 (in 2020 #148)

MFiT-T6#27

To save £100K in 48months start 01/07/2020 Achieved 30/05/2023 👯♀️

To save £100k in 60months start 01/01/2027

Am a single mom of 4.Do not wait to buy a property, Buy a property and wait. 🤓0 -

I’m reading through the diary and love the sound of the courses you’ve done LWAP! What provider were they with? Especially the beginner women’s course? I’m London based and soon to be homeownerLadyWithAPlan said:Glad to see we are all moving forward in 2023. I have signed up for a twice weekly DIY class - 10 weeks of level 1 carpentry and level 1 plumbing starting next week after my Autumn 10 weeks of general DIY which I loved.

I tiled and repainted my bathroom and its a joy to walk into. I now need to do the same for my kitchen and I have lots of other DIY to do in the flat but its tax month, lots of paid work and I am doing my side hustle again in February, so I need to get back to working for that - and getting in that gym, so a busy January...plus I have bought a new Made.com workstation in the auction so this weekend as it arrives, I am sorting out my study from trashed to clear and peaceful

I am not drinking though for January which frees up more time") 0

0 -

Wow that makes your mortgage pay off even more impressive! Well doneHelloB said:Thanks ladies!

My ex abruptly left with massive debt and ended up going through an acrimonious divorce in 2020. At one point I didn't know how I could pick myself up, let alone take on a relatively big mortgage on a single income. Thank goodness I fixed the mortgage for 5 years at 1.68%, it's now 8.24% on the Halifax SVR. DON'T BUY STUFF (from Frugalwoods)

DON'T BUY STUFF (from Frugalwoods)

No seriously, just don’t buy things. 99% of our success with our savings rate is attributed to the fact that we don’t buy things... You can and should take advantage of discounts.... But at the end of the day, the only way to truly save money is to not buy stuff. Money doesn’t walk out of your wallet on its own accord.

https://forums.moneysavingexpert.com/discussion/6289577/future-proofing-my-life-deposit-saving-then-mfw-journey-in-under-13-years#latest0 -

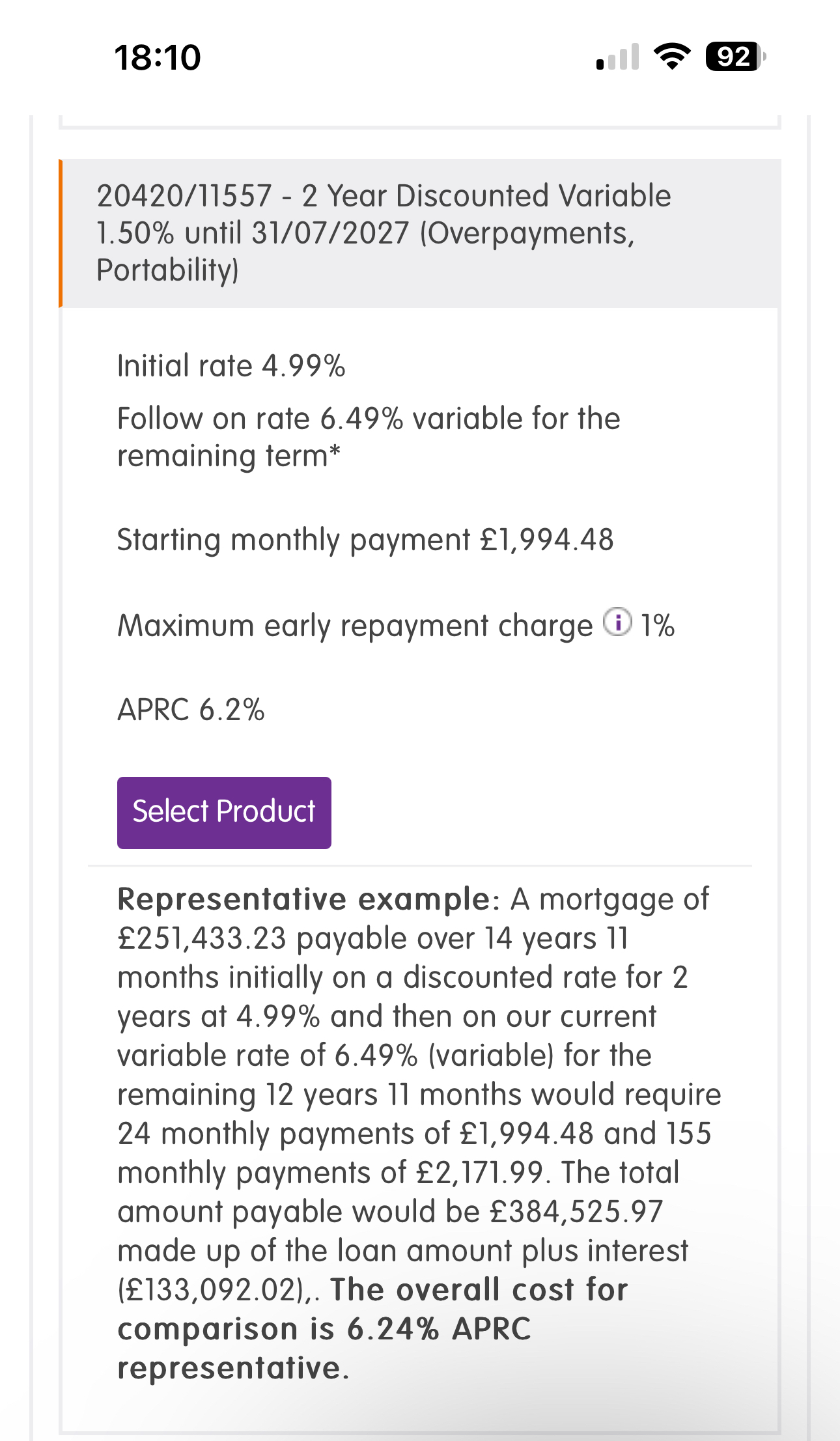

Dear diary and dear friends.I have been lurking for too long. Hope you have all been okay? I have been okay and working as hard as ever but enjoying too. Splashed out a bit by going to New York for a few days, just shopping and sight seeing, that was hectic but nice. I have also been saving hard as I want to massively pay down the mortgage again this year. I am looking forward to pay down by £150k by the end of the year. That will be the second big push and this should bring down the mortgage to below £100k once below £100k that will be a good figure to pay off with one final push after some years . I am also hoping to save enough to be mortgage neutral before I pump in the £150k. So to be honest I have really been pushing hard at savings.Oh how time flies?! I have once again approaching to the end of my current mortgage deal. As always I will go for a tracker product. I have been getting alerts to switch but have not accepted any of their offers as they were only offering me fixed rate products. So I waited it out and now I am being offered one discounted tracker mortgage product each time I check . So I am still postponing accepting a product as I am just wondering if the rates might go down or they might just offer me something better. 🤷♀️ I am not also too pressed if I fall into standard variable for a bit but will definitely try to avoid that.As I plan to massively pay down I did not want to fix as all their fixes were going to make me pay a penalty of 6% on early repayments initially and now down to 4% penalty for the 2yr fixes but more if fixing for longer. The only tracker they are offering me will charge me 1% penalty early repayment for 2yrs. I am glad that now they are offering me a tracker as they were trying to force me to fixed rate. I will need to choose a product by end of May

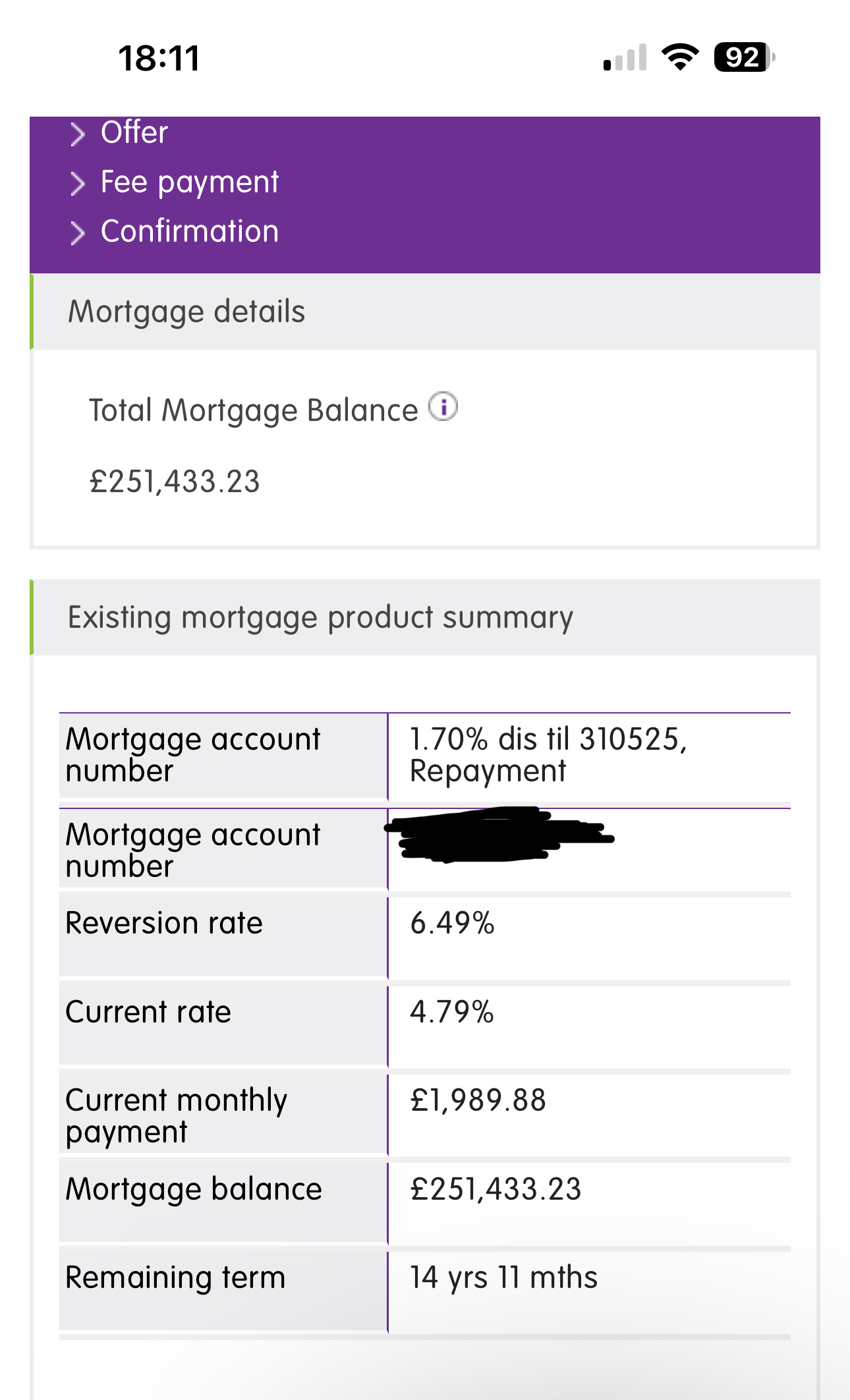

The product I will likely choose 👇🏽 My current product is 1.7% discounted 👇🏽

My current product is 1.7% discounted 👇🏽

I am currently paying £1989.88

and new product mean I will be paying £1994.48 so I will be paying just under £5 more per month.The rate hikes have been a hard slog thank goodness rates are down a bit. £5 more per month is not to bad. I can see the end now and I can smell the sweet aroma of no mortgage. Just a few more years to go once I pay the £150k. 🤞🏽

hope you have all been okay and making your overpayments. I have been managing to continue with the £100 OP. Every little helps! 🌺🥰Initial mortgage bal £487.5k, current £238k, target £122k (quarter way!)

Mortgage start date first week of July 2019,

Mortgage term 23yrs(end of June 2042🙇🏽♀️),Target is to pay it off in 10years(by 2030🥳).MFW#10 (2022/23 mfw#34)(2021 mfw#47)(2020 mfw#136)

£12K in 2021 #54 (in 2020 #148)

MFiT-T6#27

To save £100K in 48months start 01/07/2020 Achieved 30/05/2023 👯♀️

To save £100k in 60months start 01/01/2027

Am a single mom of 4.Do not wait to buy a property, Buy a property and wait. 🤓5 -

You’re doing great and living as well as paying it down 🥰🥰Sealed pot challenge 822

Jan - £176.66 :j0 -

Hi @Sistergold good to see post :-) Wow, a huge overpayment of £150k by the end of the year would be amazing and very motivating! I hope the rates go down even further so you get an even better tracker deal. The next BoE interest rate meeting is 8th May so you could hang on and see how the base rate will affect the mortgage rates.

Good on you for saving hard. I'm taking a similar approach so I know it's not an easy feat especially in this economy. I recently made a £20k overpayment after not making any in a very long time. I debated on whether I should keep it in an ISA but ultimately, I want to prioritise paying down my mortgage early and save over £100k in interest in the long run. It's encouraging to finally see the balance go down significantly.0 -

Thank you @dawnybabes 🥰dawnybabes said:You’re doing great and living as well as paying it down 🥰🥰Initial mortgage bal £487.5k, current £238k, target £122k (quarter way!)

Mortgage start date first week of July 2019,

Mortgage term 23yrs(end of June 2042🙇🏽♀️),Target is to pay it off in 10years(by 2030🥳).MFW#10 (2022/23 mfw#34)(2021 mfw#47)(2020 mfw#136)

£12K in 2021 #54 (in 2020 #148)

MFiT-T6#27

To save £100K in 48months start 01/07/2020 Achieved 30/05/2023 👯♀️

To save £100k in 60months start 01/01/2027

Am a single mom of 4.Do not wait to buy a property, Buy a property and wait. 🤓0 -

Welldone on the £20k OP, that’s a lot! Yes the interest payable is a lot and it’s good to pay down to reduce that as much as possible. If I look at the tracker quote and the amount of interest payable of £133k?! I know I have to pay down the mortgage as quickly as possible as I don’t want to pay more than necessary.Mysaving said:Hi @Sistergold good to see post :-) Wow, a huge overpayment of £150k by the end of the year would be amazing and very motivating! I hope the rates go down even further so you get an even better tracker deal. The next BoE interest rate meeting is 8th May so you could hang on and see how the base rate will affect the mortgage rates.

Good on you for saving hard. I'm taking a similar approach so I know it's not an easy feat especially in this economy. I recently made a £20k overpayment after not making any in a very long time. I debated on whether I should keep it in an ISA but ultimately, I want to prioritise paying down my mortgage early and save over £100k in interest in the long run. It's encouraging to finally see the balance go down significantly.Thank for that reminder concerning the 8th of May BoE meeting, will hold out till then as there is no real hurry. A delay will cost just under a £100 each month which will not be the end of the world. Will wait and see what happens in May. 🌺Initial mortgage bal £487.5k, current £238k, target £122k (quarter way!)

Mortgage start date first week of July 2019,

Mortgage term 23yrs(end of June 2042🙇🏽♀️),Target is to pay it off in 10years(by 2030🥳).MFW#10 (2022/23 mfw#34)(2021 mfw#47)(2020 mfw#136)

£12K in 2021 #54 (in 2020 #148)

MFiT-T6#27

To save £100K in 48months start 01/07/2020 Achieved 30/05/2023 👯♀️

To save £100k in 60months start 01/01/2027

Am a single mom of 4.Do not wait to buy a property, Buy a property and wait. 🤓1 -

Thanks Sistergold.0

-

Well done on what you've achieved this year and great to hear you had a lovely trip to NY too

") keep going, you'll get there.

keep going, you'll get there.

Debt = £8017/£8017 (100% paid - cleared 26th August 2020) Boiler Fund = £2500/£2500 (100% saved - 26th August 2021)Emergency fund = £5000/£5000 (100% saved - 5th Jan 2025) | MFW Goal 2025: £6429/£3000 | Mortgage = £86,468/£132,469 (35% paid)Goal for 2026:1) MFW £4734/£3600 - achieved!!0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards