We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

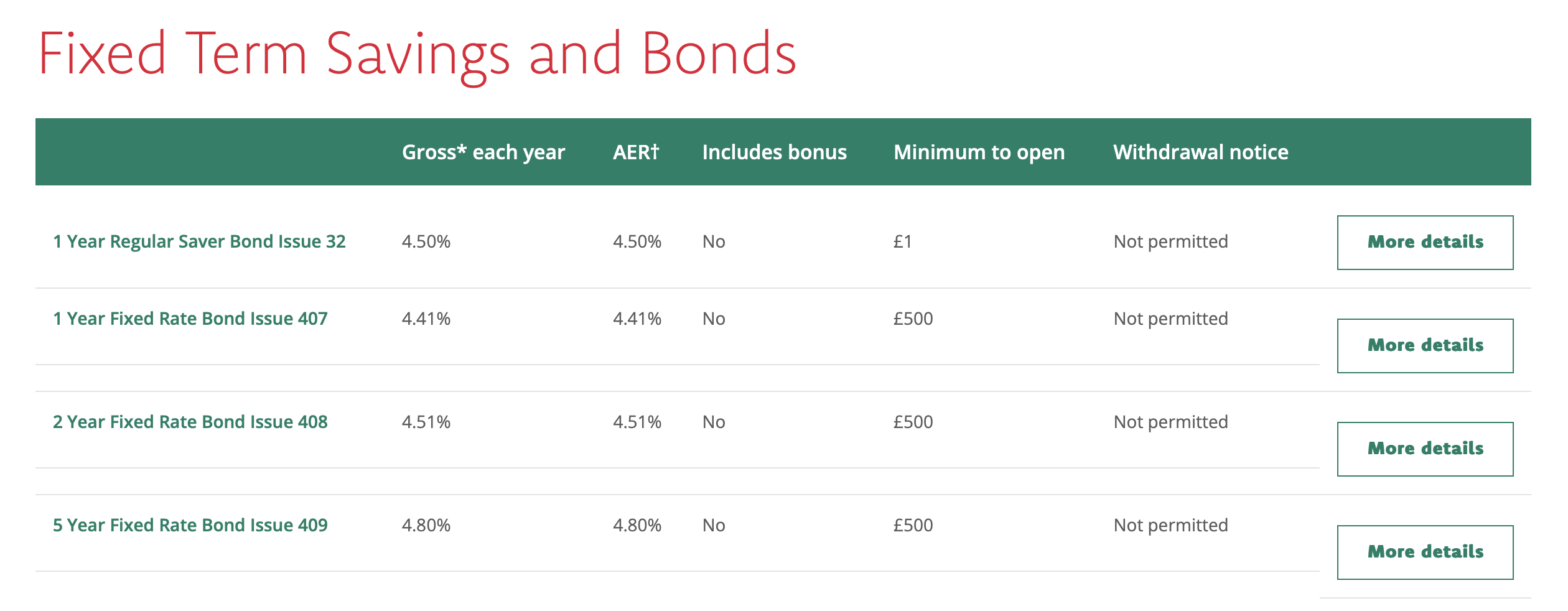

Regular Savings Accounts: The Best Currently Available List!

Comments

-

The main drawback I can see with this however is that I also do seem have a slight knack for sending technical systems a bit loopy.dekkard said:

If not already doing, you could think about working in web development / software testing. Sounds like you have some of the required attributes!Bridlington1 said:aaj123 said:

Do you mind me asking what was the genesis of your extreme obsession (to the valuable benefit of the rest of us) with savings accounts?Bridlington1 said:

Whenever Principality have launched a new regular saver recently it has appeared on moneyfacts shortly after midnight the night before it was launched so by this logic we should know when it will be launched a few hours in advance.ForumUser7 said:TiVo_Lad said:

There is no Regular Saver currently listed on the Principality website, which suggests that a launch isn't far away. IIRC the last one officially launched at 09:00.Bridlington1 said:

This is one of the reasons I opened the account this afternoon. Whenever it's appeared on moneyfacts shortly after midnight the link has always been available and working so I wanted to see exactly how far in advance the link would appear. With hindsight I should have just noted that a new regular saver will be launched soon and just left it at that, this would have answered that question for me without the risk of annoying Principality BS. But there's little I can do about that now.Malchester said:

I haven't tried to send funds anc wouldn't do until it was fully opened and I know the interest rate even though I have sort code and account number and reference for the account. Just tried to open the account out of interest and for devilment.Bridlington1 said:

I would agree, I really could do with learning some more patience! I think this episode was more a combination of curiosity mixed with my own stupidity more than anything else though.Stargunner said:

It would be a lot easier if you were more patient and waited for the account to be live and you would also have the benefit of knowing the interest rate before you started trying to fund it.Bridlington1 said:

When I applied for a new Principality account last year after having previously closed my only account with them I had to wait for an activation key to arrive in the post before I could view my accounts online so I wouldn't worry about it too much.Malchester said:Have been Principality customer in the past but details not recognised so applied for the new regular saver in hop / on spec. Have got user ID and account number and system says I have registered but cannot log in. Will wait and see

Having said that it may be worth hanging fire with applying for the new regular saver issue 33 though. There seems to be an issue with receiving funds into it, which doesn't surprise me too much given that the account has yet to be launched. I sent some money to it around 5 hours ago and nothing is showing in online banking yet. I've checked the account details multiple times and they are correct. I've just attempted to make a £1 transfer from my FHS regular saver to the regular saver issue 33 account as a test and I got this message:

Hopefully it will resolve itself in over the coming days when they actually launch the account but I fear things could get quite eventful.

Any idea when the account goes live?

So I don't know is the honest answer.

If I were to hazard a guess I would guess it will appear on moneyfacts either shortly after midnight tonight but more likely shortly after midnight on Monday or Tuesday morning since I can't recall them ever launching a new regular saver on a non working day, with the account officially becoming live later that morning but it could be anytime really.

There is still, and the FHS and NHS RS and children's RS etc.

Launch time sounds right to me though, surprised it wasn't realised today - maybe tomorrow

Which day it will be officially launched is very much an unknown. If I recall correctly this is the first time anyone on this forum has discovered a new Principality savings account will be launched before it has even been listed anywhere and I had checked the link on Thursday and it wasn't online then so it was discovered about as early as it could be. I doubt even the staff at Principality will know about issue 33 yet so we are in uncharted territory in many ways.

It could go live tomorrow or the day after but it could be a couple of weeks yet. I don't know which of these scenarios is the most likely. It's all very intriguing though.

I mean we all like making money go far but knowing timings of when different accounts appear on moneyfacts, whose link works with what prefix, etc is an altogether different level. lol.

MSE does tend to bring out the best of people to everyone's benefit. I recall a chap in the Phone landline forum who had a similar obsession about landline billing mechanisms, 08xx numbers, how to avoid and prefixes, etc.I've just always been more of a saver. I remember my granddad telling me that the banks pay people to keep their money in them when I was very young and I quite liked this idea. Also I think the fact that when I was young my father was always terrible with money, having gone bankrupt on more than one occasion when I was growing up, helped to seal the deal to some extent. I have always been petrified of the thought of going into debt for whatever reason, the best way to ensure this never happens is to ensure you always have sufficient savings to cover all possible emergencies.With savings accounts I simply try and maximise the interest I get on my savings, in part out of compulsion since I absolutely hate spending money so instinctively hoard it instead and in part part because I also quite enjoy being a bit of a rate tart, plus I am a bit of a perfectionist in some ways so want to be earning as much interest as I possibly can. I am forever chasing the top savings rates, checking this forum several times a day as well as moneyfacts and others frequently.As a result I've unintentionally remembered the rough timings of when some of the banks and building societies launch savings products as well as noticed patterns in how various application links are structured since some of them follow a very logical pattern, Principality being the obvious one.The peculiarities of Principality's links is something I discovered accidentally last year though. Last summer I tried applying for one of their regular savings accounts the day it was launched, but the link to the old account was still on their website so I inadvertently opened that instead. When I tried again later that day I noticed the links seemed very similar, compared the two links, noticed that the new one was almost identical but with 1 added to the product code and from this I discovered how Principality's links are structured.

In the past year alone I've suffered TSB's technical systems not letting me make payments in online banking without locking me out and asking me to ring their fraud team (phone/branch payments worked fine though), a set of 42 traffic lights which failed to notice I exist, a psychology experiment at university in which I crashed a computer system (the only person out of around 100 to do so), a university printer that decided to blow a fuse when I clicked "print", a lift which most of the time only goes up if I walk out of the lift, then walk back in again and a laptop which makes loud bleeping noises unless I have something playing in the background (currently the national anthem) amongst other issues.

Given the above I don't think any company would really want to let me loose on their technical systems since some might say I am the Frank Spencer of the digital age.7 -

Fear not I've heard that before. At the moment I'm just pouring pretty much every penny into saving for a house deposit but once I have got that sorted with an emergency fund built up (most likely in some top paying regular savers) I shall start investing.aaj123 said:

I am sure you have heard this before but cash is not the way to build up wealth. You are nearly always achieving negative real returns I.e your purchasing power is going down and that's before we even consider tax on interest.Bridlington1 said:

I've never touched crypto before in my life. My money is pretty much all in cash savings as I intend to buy my first home in a year or so. The only exceptions being £10 worth of shares I hold with Wombat invest (I got a free £10 when I referred someone to Wombat invest which needed to be invested before I could withdraw it) and some money I have in Wealthify's GIAs and S&S ISA that were the result of using Wealthify as a source of cheap DDs and a £50 sign up offer but that's it.aaj123 said:

Given you said you are a saver who likes to hoard money, are you also into crypto and the hodl culture - in particular btc and eth rather than shitcoins that are just a gamble?Bridlington1 said:aaj123 said:

Do you mind me asking what was the genesis of your extreme obsession (to the valuable benefit of the rest of us) with savings accounts?Bridlington1 said:

Whenever Principality have launched a new regular saver recently it has appeared on moneyfacts shortly after midnight the night before it was launched so by this logic we should know when it will be launched a few hours in advance.ForumUser7 said:TiVo_Lad said:

There is no Regular Saver currently listed on the Principality website, which suggests that a launch isn't far away. IIRC the last one officially launched at 09:00.Bridlington1 said:

This is one of the reasons I opened the account this afternoon. Whenever it's appeared on moneyfacts shortly after midnight the link has always been available and working so I wanted to see exactly how far in advance the link would appear. With hindsight I should have just noted that a new regular saver will be launched soon and just left it at that, this would have answered that question for me without the risk of annoying Principality BS. But there's little I can do about that now.Malchester said:

I haven't tried to send funds anc wouldn't do until it was fully opened and I know the interest rate even though I have sort code and account number and reference for the account. Just tried to open the account out of interest and for devilment.Bridlington1 said:

I would agree, I really could do with learning some more patience! I think this episode was more a combination of curiosity mixed with my own stupidity more than anything else though.Stargunner said:

It would be a lot easier if you were more patient and waited for the account to be live and you would also have the benefit of knowing the interest rate before you started trying to fund it.Bridlington1 said:

When I applied for a new Principality account last year after having previously closed my only account with them I had to wait for an activation key to arrive in the post before I could view my accounts online so I wouldn't worry about it too much.Malchester said:Have been Principality customer in the past but details not recognised so applied for the new regular saver in hop / on spec. Have got user ID and account number and system says I have registered but cannot log in. Will wait and see

Having said that it may be worth hanging fire with applying for the new regular saver issue 33 though. There seems to be an issue with receiving funds into it, which doesn't surprise me too much given that the account has yet to be launched. I sent some money to it around 5 hours ago and nothing is showing in online banking yet. I've checked the account details multiple times and they are correct. I've just attempted to make a £1 transfer from my FHS regular saver to the regular saver issue 33 account as a test and I got this message:

Hopefully it will resolve itself in over the coming days when they actually launch the account but I fear things could get quite eventful.

Any idea when the account goes live?

So I don't know is the honest answer.

If I were to hazard a guess I would guess it will appear on moneyfacts either shortly after midnight tonight but more likely shortly after midnight on Monday or Tuesday morning since I can't recall them ever launching a new regular saver on a non working day, with the account officially becoming live later that morning but it could be anytime really.

There is still, and the FHS and NHS RS and children's RS etc.

Launch time sounds right to me though, surprised it wasn't realised today - maybe tomorrow

Which day it will be officially launched is very much an unknown. If I recall correctly this is the first time anyone on this forum has discovered a new Principality savings account will be launched before it has even been listed anywhere and I had checked the link on Thursday and it wasn't online then so it was discovered about as early as it could be. I doubt even the staff at Principality will know about issue 33 yet so we are in uncharted territory in many ways.

It could go live tomorrow or the day after but it could be a couple of weeks yet. I don't know which of these scenarios is the most likely. It's all very intriguing though.

I mean we all like making money go far but knowing timings of when different accounts appear on moneyfacts, whose link works with what prefix, etc is an altogether different level. lol.

MSE does tend to bring out the best of people to everyone's benefit. I recall a chap in the Phone landline forum who had a similar obsession about landline billing mechanisms, 08xx numbers, how to avoid and prefixes, etc.I've just always been more of a saver. I remember my granddad telling me that the banks pay people to keep their money in them when I was very young and I quite liked this idea. Also I think the fact that when I was young my father was always terrible with money, having gone bankrupt on more than one occasion when I was growing up, helped to seal the deal to some extent. I have always been petrified of the thought of going into debt for whatever reason, the best way to ensure this never happens is to ensure you always have sufficient savings to cover all possible emergencies.With savings accounts I simply try and maximise the interest I get on my savings, in part out of compulsion since I absolutely hate spending money so instinctively hoard it instead and in part part because I also quite enjoy being a bit of a rate tart, plus I am a bit of a perfectionist in some ways so want to be earning as much interest as I possibly can. I am forever chasing the top savings rates, checking this forum several times a day as well as moneyfacts and others frequently.As a result I've unintentionally remembered the rough timings of when some of the banks and building societies launch savings products as well as noticed patterns in how various application links are structured since some of them follow a very logical pattern, Principality being the obvious one.The peculiarities of Principality's links is something I discovered accidentally last year though. Last summer I tried applying for one of their regular savings accounts the day it was launched, but the link to the old account was still on their website so I inadvertently opened that instead. When I tried again later that day I noticed the links seemed very similar, compared the two links, noticed that the new one was almost identical but with 1 added to the product code and from this I discovered how Principality's links are structured.

Fine if this is an interim strategy for your house deposit but consider diversifying later.

1 -

Since I fear we're starting to go a bit off topic (apologies for that), any guesses for what the new Principality BS regular saver issue 33 interest rate will be?

0 -

I wondered perhaps 4.75% - someone else suggested this around when the BOE rate rose last month IIRC. 5% would be nice, but maybe too niceBridlington1 said:Since I fear we're starting to go a bit off topic (apologies for that), any guesses for what the new Principality BS regular saver issue 33 interest rate will be?If you want me to definitely see your reply, please tag me @forumuser7 Thank you.

N.B. (Amended from Forum Rules): You must investigate, and check several times, before you make any decisions or take any action based on any information you glean from any of my content, as nothing I post is advice, rather it is personal opinion and is solely for discussion purposes. I research before my posts, and I never intend to share anything that is misleading, misinforming, or out of date, but don't rely on everything you read. Some of the information changes quickly, is my own opinion or may be incorrect. Verify anything you read before acting on it to protect yourself because you are responsible for any action you consequently make... DYOR, YMMV etc.1 -

Well they did jump 0.75% from 3% to 3.75% from issue 30 to 31 if I recall correctly so a 0.5% increase doesn't seem inconceivable to me at all, plus it has been a while since they launched issue 32.ForumUser7 said:

I wondered perhaps 4.75% - someone else suggested this around when the BOE rate rose last month IIRC. 5% would be nice, but maybe too niceBridlington1 said:Since I fear we're starting to go a bit off topic (apologies for that), any guesses for what the new Principality BS regular saver issue 33 interest rate will be?1 -

Issue 30 3.25% released in or around October 2022Bridlington1 said:

Well they did jump 0.75% from 3% to 3.75% from issue 30 to 31 if I recall correctly so a 0.5% increase doesn't seem inconceivable to me at all, plus it has been a while since they launched issue 32.ForumUser7 said:

I wondered perhaps 4.75% - someone else suggested this around when the BOE rate rose last month IIRC. 5% would be nice, but maybe too niceBridlington1 said:Since I fear we're starting to go a bit off topic (apologies for that), any guesses for what the new Principality BS regular saver issue 33 interest rate will be?

Issue 31 4.00% released in or around February 2023

Issue 32 4.50% released in or around March 2023

Issue 33 ?% to release in (or around) June 2023

I'd be pleased with 5.00% tbh - more favourable terms than Loughborough BS RSIf you want me to definitely see your reply, please tag me @forumuser7 Thank you.

N.B. (Amended from Forum Rules): You must investigate, and check several times, before you make any decisions or take any action based on any information you glean from any of my content, as nothing I post is advice, rather it is personal opinion and is solely for discussion purposes. I research before my posts, and I never intend to share anything that is misleading, misinforming, or out of date, but don't rely on everything you read. Some of the information changes quickly, is my own opinion or may be incorrect. Verify anything you read before acting on it to protect yourself because you are responsible for any action you consequently make... DYOR, YMMV etc.2 -

Still no news on issue 33. I wonder how long it will take Principality to reveal the mystery. I won't fund it if it's below 5%.ForumUser7 said:

Issue 30 3.25% released in or around October 2022Bridlington1 said:

Well they did jump 0.75% from 3% to 3.75% from issue 30 to 31 if I recall correctly so a 0.5% increase doesn't seem inconceivable to me at all, plus it has been a while since they launched issue 32.ForumUser7 said:

I wondered perhaps 4.75% - someone else suggested this around when the BOE rate rose last month IIRC. 5% would be nice, but maybe too niceBridlington1 said:Since I fear we're starting to go a bit off topic (apologies for that), any guesses for what the new Principality BS regular saver issue 33 interest rate will be?

Issue 31 4.00% released in or around February 2023

Issue 32 4.50% released in or around March 2023

Issue 33 ?% to release in (or around) June 2023

I'd be pleased with 5.00% tbh - more favourable terms than Loughborough BS RS0 -

Kroo are raising their interest rate from 1st July to 3.85% (feeder account)

5 -

Melton BS 5% RS NLA according to MoneyFacts. Still shows on the BS’s website, perhaps it’ll be removed tomorrowIf you want me to definitely see your reply, please tag me @forumuser7 Thank you.

N.B. (Amended from Forum Rules): You must investigate, and check several times, before you make any decisions or take any action based on any information you glean from any of my content, as nothing I post is advice, rather it is personal opinion and is solely for discussion purposes. I research before my posts, and I never intend to share anything that is misleading, misinforming, or out of date, but don't rely on everything you read. Some of the information changes quickly, is my own opinion or may be incorrect. Verify anything you read before acting on it to protect yourself because you are responsible for any action you consequently make... DYOR, YMMV etc.1 -

According to moneyfacts Suffolk BS are launching a new 4.15% regular saver for existing customers and new customers living in IP, NR, CO, CM, CB and PE postcodes.1

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards