We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Regular Savings Accounts: The Best Currently Available List!

Comments

-

But it's a scenario to be aware of. Especially those who may be already paying the max into their pension.kaMelo said:friolento said:kaMelo said:

Does it really matter? Surely maximising interest is more beneficial irrespective of any tax liability.mattojgb said:

You didn't need to even have any savings to qualify for the payment.CuparLad said:Re: the Nationwide Fairer Share PaymentThe payment is taxable savings income. This means that it is treated in the same way as any interest you may earn on your savings account or current account. We are not required to deduct any tax from the payment, but we will report it to HM Revenue & Customs (HMRC).You may be liable to income tax on the payment, depending on whether the total amount of interest you have received in the tax year is more than your Personal Savings Allowance.

I was thinking I'd kept my interest earnings below the threshold, but this would take me over.

It may well matter for those who get catapulted into Higher Rate tax by this payment. Suddenly their tax free amount drops from £1,000 to £500, and they get to pay 40% tax on anything above £500.Although a niche scenario I guess it can matter. It would be better not to run things so close though by using a pension to soak up any 40% income.

My priority of paying into accounts is 7.5% and above first, then offset mortgage (currently 6%), then accounts paying 6.5-7.5%, then ISA when the new tax year starts at 5% (currently fully paid up for this year), then accounts in descending order, with easy access taking priority over those with restricted access.

This order of priority may change should the mortgage and ISA rates change.

I'm hoping I will stay out of the PSA next tax year, and my put money into investments to help stay out of it, as this time last year it was much easier to stay out of the PSAI consider myself to be a male feminist. Is that allowed?0 -

Apologies for taking this further off topic, but this is the situation I find myself in. I thought I'd adjusted pension contributions so my salary was below the threshold, but I hadn't accounted for all my interest earnings. I'm too late now to put any more pension in via my employer, I can only put it into my SIPP. How complex is it to then unwind/claim back all the 40% tax payments? Kind of a nice problem to have, although only down to the frozen thresholds. ThankskaMelo said:friolento said:kaMelo said:

Does it really matter? Surely maximising interest is more beneficial irrespective of any tax liability.mattojgb said:

You didn't need to even have any savings to qualify for the payment.CuparLad said:Re: the Nationwide Fairer Share PaymentThe payment is taxable savings income. This means that it is treated in the same way as any interest you may earn on your savings account or current account. We are not required to deduct any tax from the payment, but we will report it to HM Revenue & Customs (HMRC).You may be liable to income tax on the payment, depending on whether the total amount of interest you have received in the tax year is more than your Personal Savings Allowance.

I was thinking I'd kept my interest earnings below the threshold, but this would take me over.

It may well matter for those who get catapulted into Higher Rate tax by this payment. Suddenly their tax free amount drops from £1,000 to £500, and they get to pay 40% tax on anything above £500.Although a niche scenario I guess it can matter. It would be better not to run things so close though by using a pension to soak up any 40% income.0 -

Message from Skipton:

The date for the deposit still shows as the 4th. May be it will update overnight?0

The date for the deposit still shows as the 4th. May be it will update overnight?0 -

Skipton members RSI remember that some posters were considering closing the 7.5% version and then immediately opening the present 7% version. I am considering this technique to free savings to partially fund a new ISA come April.Has anyone tried this? How easy was the change?0

-

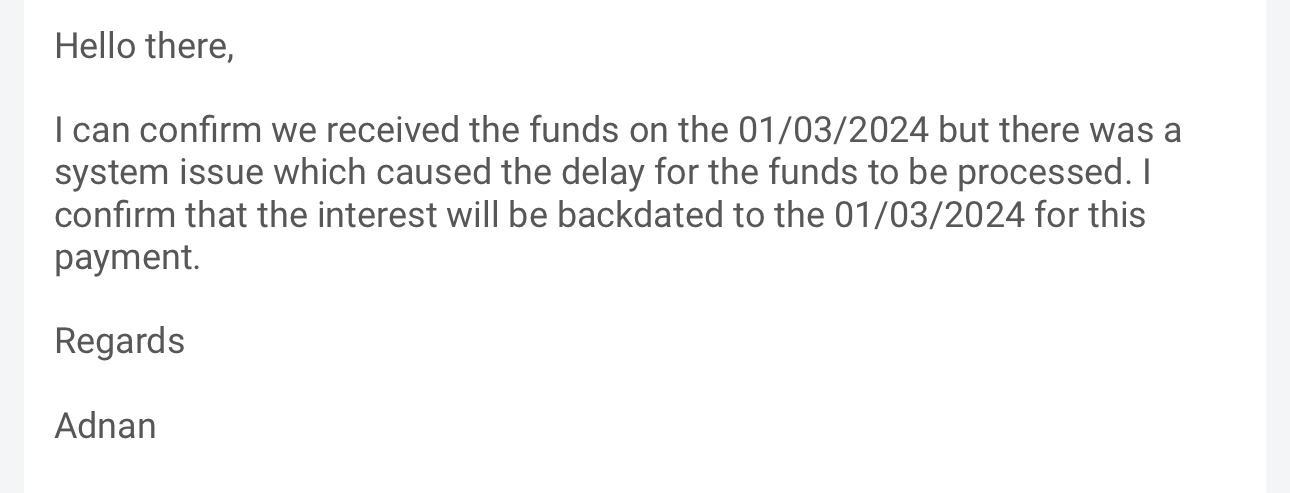

I inquired by live chat on Tuesday (5th) about my SO paid out of my CA on Friday (1st) which eventually showed as received late on Monday(4th). I was first told that it was not possible to backdate the payment, but when I challenged this, after a protracted pause in the conversation, I was told that the CS could "see" that .....friolento said:Message from Skipton:The date for the deposit still shows as the 4th. May be it will update overnight?"My apologies, I can see that interest is being earned on this payment from the 1st March."

I asked them how they could "see" this, was it a separate field on the screen to the date credited? It took a while to get a reply to that actual question, but I eventually got ....

"I am able to view the date funds were received, processed and interested paid from."

So, it seems that the payment might remain as 4th, with a promise that the interest will be paid from the 1st. I have kept a copy of the chat!

Compiler of the RS League Table.

Being nosey... How many Regular Saver accounts do you have? — MoneySavingExpert Forum2 -

My OH had this problem, the last letter of his surname was missed by the Coop, didn't stop the switch taking place, which I was surprised at.PloughmansLunch said:

I get his message below, and I can’t face a hour+ of that hold music again. Unless my name or date of birth has changed without my knowledge I’m stumped, as the only other details needed are right there in front of me on the card. It doesn’t work if I use the RS details eitherdealyboy said:

Co-op RS@PloughmansLunch said:

Yes - I’ve had emails and letters in the post confirming the account details so both are technically open, but have left them unfunded for now as I’m unable to register for online banking. I’m a new customer but my accounts are locked before I’ve even chosen a password for some reason, and an hour and a quarter on the phone for co-op CS to attempt to rectify was a complete waste of time.ChewyyBacca said:Has anybody opened a Co-Op Cashminder account and then successfully opened the 7% Regular saver with Co-op?

T&Cs of RS on the website says Cashminder current account is acceptable, but someone on the forum got rejected for RS, saying Cashminder acct is not acceptable.

Anyone else has got a different experience?

Hi Ploughmans ... What actually happens when you try to register? I must have tried about a dozen times before it actually worked.

His name is 6 space 8, with middle names taking up another 15, so there may be some truncation going on.0 -

I got it sorted out in the end after another long phonecall - co-op had retained my old debit card and account details from a 1yr+ ago switched out account, and not updated my customer profile with the new current & savings accounts.savethepandas said:

My OH had this problem, the last letter of his surname was missed by the Coop, didn't stop the switch taking place, which I was surprised at.PloughmansLunch said:

I get his message below, and I can’t face a hour+ of that hold music again. Unless my name or date of birth has changed without my knowledge I’m stumped, as the only other details needed are right there in front of me on the card. It doesn’t work if I use the RS details eitherdealyboy said:

Co-op RS@PloughmansLunch said:

Yes - I’ve had emails and letters in the post confirming the account details so both are technically open, but have left them unfunded for now as I’m unable to register for online banking. I’m a new customer but my accounts are locked before I’ve even chosen a password for some reason, and an hour and a quarter on the phone for co-op CS to attempt to rectify was a complete waste of time.ChewyyBacca said:Has anybody opened a Co-Op Cashminder account and then successfully opened the 7% Regular saver with Co-op?

T&Cs of RS on the website says Cashminder current account is acceptable, but someone on the forum got rejected for RS, saying Cashminder acct is not acceptable.

Anyone else has got a different experience?

Hi Ploughmans ... What actually happens when you try to register? I must have tried about a dozen times before it actually worked.

His name is 6 space 8, with middle names taking up another 15, so there may be some truncation going on.1 -

Got a Co-op current account opened fairly quickly so applied for their regular saver on 4th March and got an application acknowledgement. It's now the 12th and no sign of the account. Called today and was told I forgot to put my middle name on the form but I guess nobody contacted me to query this?! It's so weird to be waiting so long when every other bank opens these accounts sometimes within a matter of minutes. She said I should have the account within the next couple of days but I guess we'll just have to see.0

-

They say (when she asked what was taking so long) they hadn't processed my OH's because she put 'Ms' on the application when their existing records said 'Miss' ... FGS!renza88 said:Got a Co-op current account opened fairly quickly so applied for their regular saver on 4th March and got an application acknowledgement. It's now the 12th and no sign of the account. Called today and was told I forgot to put my middle name on the form but I guess nobody contacted me to query this?! It's so weird to be waiting so long when every other bank opens these accounts sometimes within a matter of minutes. She said I should have the account within the next couple of days but I guess we'll just have to see.

They asked which was correct?

Seriously? 'Both', she said.

She's still waiting after a February 26th application...! They say they're busy with processing... finding things to be picky about? Failed to put a full stop after 'Rd' in your address? 2

2 -

Whenever you're talking to a computer, you just need to tell it what it wants to hear. If you're giving data to a computer that already holds data on you, just give it the data that matches what it already knowsI consider myself to be a male feminist. Is that allowed?4

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards