We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Regular Savings Accounts: The Best Currently Available List!

Comments

-

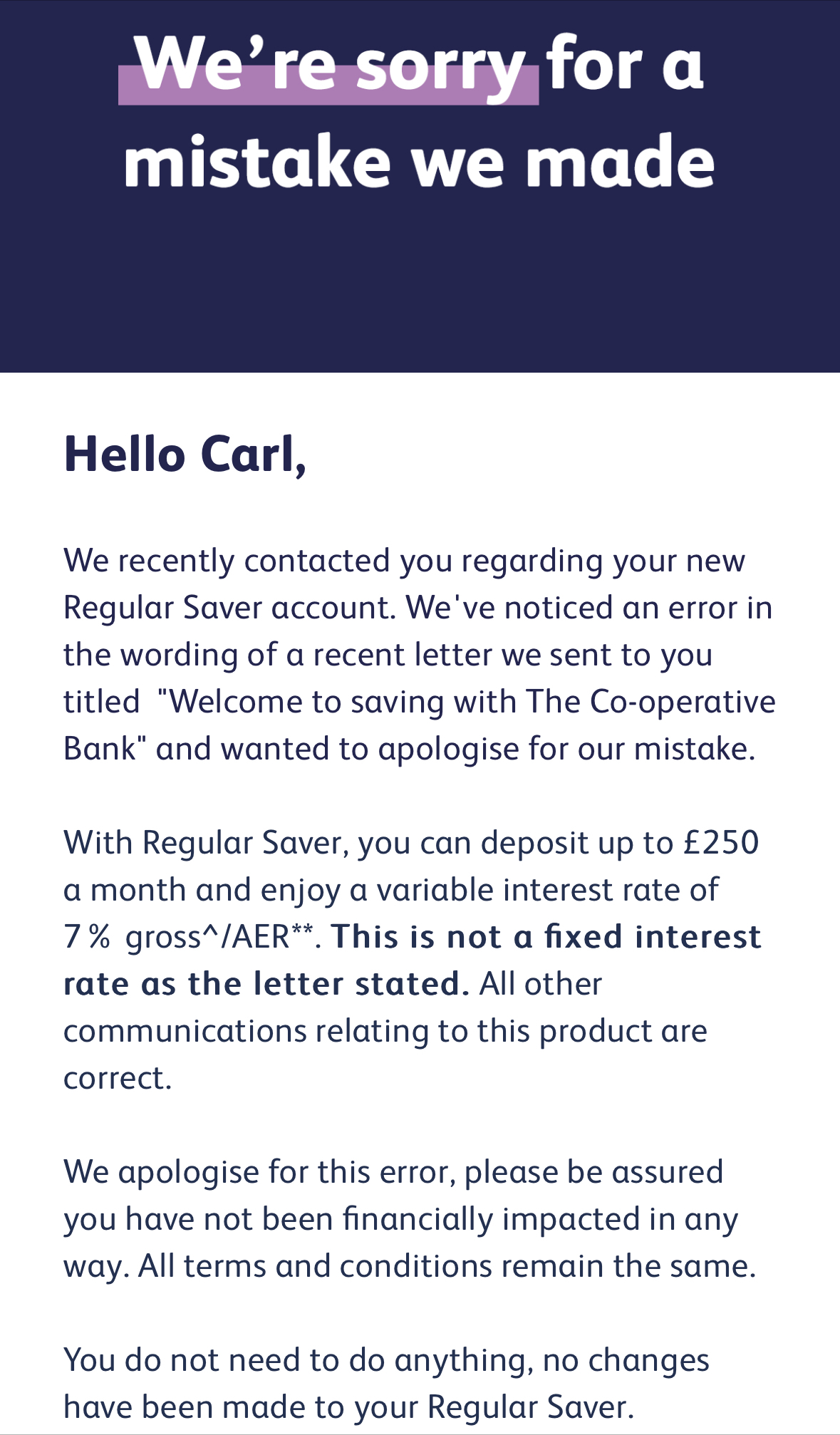

Same old Coop.E_zroda said:Not Carl too?trickydicky14 said:

Yes I just had the same email.csw5780 said:Gers said:pecunianonolet said:Received my postal correspondence from Coop today about my regular saver and it states

"Your regular saver is a fixed term account for 12 months, paying a variable interest rate of 7.00% gross/AER"

So looks like they noticed the error and corrected it in their correspondence. Thought it might be helpful to others as some early birds received letters stating it different and being a fixed rate.Interesting! My letter, dated 06 March states:'Thanks for choosing to save with us and for making your initial deposit into your new Co-operative Bank Regular Saver paying a rate of 7.00% gross / AER." No reference to either fixed or variable rate.Thnk that I'll scan and keep this letter until maturity. Email received today!

Email received today!

Just dreadful IMO0 -

Nothing dreadful about a 7% interest rate. What the hell does it matter what the email says, we know it's variable. Doubt I'll bother to look at any correspondence and just forget about the Co-Op for 12 months until I'm able to collect the proceeds.simonsmithsays said:

Same old Coop.E_zroda said:Not Carl too?trickydicky14 said:

Yes I just had the same email.csw5780 said:Gers said:pecunianonolet said:Received my postal correspondence from Coop today about my regular saver and it states

"Your regular saver is a fixed term account for 12 months, paying a variable interest rate of 7.00% gross/AER"

So looks like they noticed the error and corrected it in their correspondence. Thought it might be helpful to others as some early birds received letters stating it different and being a fixed rate.Interesting! My letter, dated 06 March states:'Thanks for choosing to save with us and for making your initial deposit into your new Co-operative Bank Regular Saver paying a rate of 7.00% gross / AER." No reference to either fixed or variable rate.Thnk that I'll scan and keep this letter until maturity. Email received today!

Just dreadful IMO3 -

Yes in practise this is only an issue if (when) they try to lower the rates.

One could argue their email stating this has no impact on us does sort of imply that there is no impact of the rate being variable, not fixed, suggesting they don't plan to drop the rates; i.e. their statement that I've "not been financially impacted in any way" won't be true if they do later decide to make it have a financial impact.1 -

If it's a variable rate id definitely recommend you not ignoring correspondence and also not forgetting about the coop for the next 12 months - just incase they drop the rate and you've got other avenues to push your money.subjecttocontract said:

Nothing dreadful about a 7% interest rate. What the hell does it matter what the email says, we know it's variable. Doubt I'll bother to look at any correspondence and just forget about the Co-Op for 12 months until I'm able to collect the proceeds.simonsmithsays said:

Same old Coop.E_zroda said:Not Carl too?trickydicky14 said:

Yes I just had the same email.csw5780 said:Gers said:pecunianonolet said:Received my postal correspondence from Coop today about my regular saver and it states

"Your regular saver is a fixed term account for 12 months, paying a variable interest rate of 7.00% gross/AER"

So looks like they noticed the error and corrected it in their correspondence. Thought it might be helpful to others as some early birds received letters stating it different and being a fixed rate.Interesting! My letter, dated 06 March states:'Thanks for choosing to save with us and for making your initial deposit into your new Co-operative Bank Regular Saver paying a rate of 7.00% gross / AER." No reference to either fixed or variable rate.Thnk that I'll scan and keep this letter until maturity. Email received today!

Just dreadful IMO

Regardless of that, I'd also (having had some very unsettling experiences with co-op savings in the past) suggest you'd keep a watching brief on your monthly balance and your closing balance.

Each to their own though.

0 -

My expectations are exactly what they should be i.e. with my account open and a S/O making my monthly deposits I will have no need to bother with it until February 2025. I can get on with all the more important things in my life.simonsmithsays said:

If it's a variable rate id definitely recommend you not ignoring correspondence and also not forgetting about the coop for the next 12 months - just incase they drop the rate and you've got other avenues to push your money.subjecttocontract said:

Nothing dreadful about a 7% interest rate. What the hell does it matter what the email says, we know it's variable. Doubt I'll bother to look at any correspondence and just forget about the Co-Op for 12 months until I'm able to collect the proceeds.simonsmithsays said:

Same old Coop.E_zroda said:Not Carl too?trickydicky14 said:

Yes I just had the same email.csw5780 said:Gers said:pecunianonolet said:Received my postal correspondence from Coop today about my regular saver and it states

"Your regular saver is a fixed term account for 12 months, paying a variable interest rate of 7.00% gross/AER"

So looks like they noticed the error and corrected it in their correspondence. Thought it might be helpful to others as some early birds received letters stating it different and being a fixed rate.Interesting! My letter, dated 06 March states:'Thanks for choosing to save with us and for making your initial deposit into your new Co-operative Bank Regular Saver paying a rate of 7.00% gross / AER." No reference to either fixed or variable rate.Thnk that I'll scan and keep this letter until maturity. Email received today!

Just dreadful IMO

Regardless of that, I'd also (having had some very unsettling experiences with co-op savings in the past) suggest you'd keep a watching brief on your monthly balance and your closing balance.

Each to their own though.

Checking balances every month is not something I do.

0 -

This is a very different approach to some of those of us with multiple variable accounts who lurk on here.subjecttocontract said:

My expectations are exactly what they should be i.e. with my account open and a S/O making my monthly deposits I will have no need to bother with it until February 2025. I can get on with all the more important things in my life.simonsmithsays said:

If it's a variable rate id definitely recommend you not ignoring correspondence and also not forgetting about the coop for the next 12 months - just incase they drop the rate and you've got other avenues to push your money.subjecttocontract said:

Nothing dreadful about a 7% interest rate. What the hell does it matter what the email says, we know it's variable. Doubt I'll bother to look at any correspondence and just forget about the Co-Op for 12 months until I'm able to collect the proceeds.simonsmithsays said:

Same old Coop.E_zroda said:Not Carl too?trickydicky14 said:

Yes I just had the same email.csw5780 said:Gers said:pecunianonolet said:Received my postal correspondence from Coop today about my regular saver and it states

"Your regular saver is a fixed term account for 12 months, paying a variable interest rate of 7.00% gross/AER"

So looks like they noticed the error and corrected it in their correspondence. Thought it might be helpful to others as some early birds received letters stating it different and being a fixed rate.Interesting! My letter, dated 06 March states:'Thanks for choosing to save with us and for making your initial deposit into your new Co-operative Bank Regular Saver paying a rate of 7.00% gross / AER." No reference to either fixed or variable rate.Thnk that I'll scan and keep this letter until maturity. Email received today!

Just dreadful IMO

Regardless of that, I'd also (having had some very unsettling experiences with co-op savings in the past) suggest you'd keep a watching brief on your monthly balance and your closing balance.

Each to their own though.

Checking balances every month is not something I do.

We choose to monitor correspondence and rates intensely during the term and tip and feed appropriately.

Certainly not 'forgetting about' institutions with a variable product rates and a chequered history.

I guess your approach works for you.

Bon chance1 -

I archive all significant correspondence from banks snd not forgetting them. In case of RS, I deposit every month and check that it has arrived. With regards to this Co-op mistake, I signed up for variable and happy to treat it as variable. If they drop the rate below my best paying EA I will withdraw and relocate this money elsewhere. Meanwhile every £250 deposit I made so far is earning 7% AER and I'm happy with this.simonsmithsays said:

If it's a variable rate id definitely recommend you not ignoring correspondence and also not forgetting about the coop for the next 12 months - just incase they drop the rate and you've got other avenues to push your money.subjecttocontract said:

Nothing dreadful about a 7% interest rate. What the hell does it matter what the email says, we know it's variable. Doubt I'll bother to look at any correspondence and just forget about the Co-Op for 12 months until I'm able to collect the proceeds.simonsmithsays said:

Same old Coop.E_zroda said:Not Carl too?trickydicky14 said:

Yes I just had the same email.csw5780 said:Gers said:pecunianonolet said:Received my postal correspondence from Coop today about my regular saver and it states

"Your regular saver is a fixed term account for 12 months, paying a variable interest rate of 7.00% gross/AER"

So looks like they noticed the error and corrected it in their correspondence. Thought it might be helpful to others as some early birds received letters stating it different and being a fixed rate.Interesting! My letter, dated 06 March states:'Thanks for choosing to save with us and for making your initial deposit into your new Co-operative Bank Regular Saver paying a rate of 7.00% gross / AER." No reference to either fixed or variable rate.Thnk that I'll scan and keep this letter until maturity. Email received today!

Just dreadful IMO

Regardless of that, I'd also (having had some very unsettling experiences with co-op savings in the past) suggest you'd keep a watching brief on your monthly balance and your closing balance.

Each to their own though.2 -

Thanks, spoke to TSB and believe it’s the same issue that you linked to though re registering has not worked so will have to call them again.DJDools said:

I had the same issues. Have now fixed. This might help:tg99 said:My TSB Monthly Saver matured and changed to Easy Access account in early hours of today (Wed). Trying now to open another and says sorry not eligible. I meet all the criteria so does it take a certain time - 24-48 hours? - before system properly updates and recognises previous one now matured?Potential issue:0 -

Coventry Building Society are launching Loyalty Regular Saver (2), paying 6.75%

Open the account via the Internet, branch, telephone or by post.

Pay in up to £250 per month. The maximum account balance is £3,000.

The account is available to existing members (must have held at least one savings or mortgage account with Coventry BS, ITL or Godiva since 1 January 2023 or earlier.)

There is a 14 day 'cooling off' period. After this period, you can close the account or make a withdrawal, but this will be subject to a charge equal to 30 calendar days' interest on the amount withdrawn.

Reverts into an Easy Access Saver (7) after 12 months.

If you login to Coventry BS online banking, the account is available.

The Account Summary states:

"You can only have one Loyalty Regular Saver (2) at a time."

It seems that current holders of the Loyalty Regular Saver (issue 1) cannot have issue 2.

EDIT: Please follow the direct link to the account page now that it has launched, here.

Please call me 'Kazza'.22 -

"You can only have one Loyalty Regular Saver (2) at a time."

Should mean you can have Iss1 & Iss2... But it looks like bad proof reading as it won't let you apply for Iss2 if you hold Iss1 - tried it - so the exclusion is built in the functionality.

ETA That's new for the Cov - previously you could break their rules until they eventually caught you...

5

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards