We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Regular Savings Accounts: The Best Currently Available List!

Comments

-

I think that Bridlington1 is striving to hold the most amount of bank and savings accounts out of everyone on MSE 😂OneUser1 said:For those who can get to a branch, the Westbrom 6% fixed for a year, £250 per month maximum looks attractive and is still available.I don’t understand why anyone with a 7% and 8% Regular Saver at the Monmouthshire would open the 4.75% variable as well. The higher paying accounts ensure continuity of membership. When they mature, and only then, certainly look for an account to maintain membership then. But not now.2 -

I think Bridlington1 leaves the rest of us eating dustStargunner said:

I think that Bridlington1 is striving to hold the most amount of bank and savings accounts out of everyone on MSE 😂OneUser1 said:For those who can get to a branch, the Westbrom 6% fixed for a year, £250 per month maximum looks attractive and is still available.I don’t understand why anyone with a 7% and 8% Regular Saver at the Monmouthshire would open the 4.75% variable as well. The higher paying accounts ensure continuity of membership. When they mature, and only then, certainly look for an account to maintain membership then. But not now.

I choose the rooms that I live in with care,

The windows are small and the walls almost bare,

There's only one bed and there's only one prayer;

I listen all night for your step on the stair.5 -

I closed my first Santander 5% regular saver around the time Tandem increased their EA rate to 5% to unlock the accrued interest, though did open a new one earlier this month with £1 on the off-chance.dealyboy said:

It seems to me that it's not worth the bother, but I know it's a hobby. Do you get a bonus for a full house?@Bridlington1 said:Stargunner said:

Why would you even bother opening this account, especially as you probably already have their 8% and 7% regular savers that they only launched a few months ago.,Bridlington1 said:

Yes it certainly isn't the greatest is it. Since it has a £1 minimum balance and requires no further funding I may still open it with £1 just on the off-chance it becomes competitive in the future.Wheres_My_Cashback said:

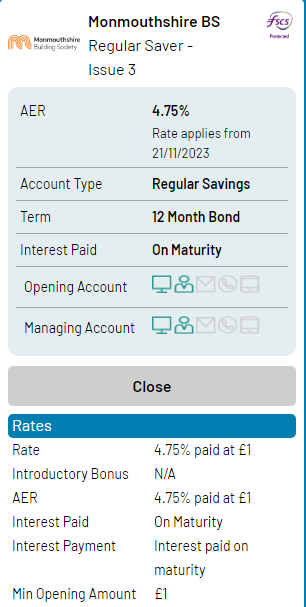

I somehow don't think MBS are going to be facing their usual problem of being overwhelmed with this oneBridlington1 said:Monmouthshire BS will be launching a Regular Saver Issue 3 at 4.75% tomorrow.

")

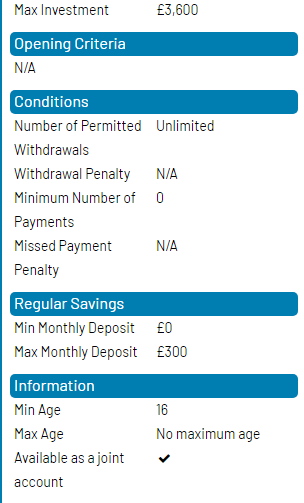

Think it's going to be more a case of... First of all you're correct, I do have their 8% and 7% regular savers. I also have the 5.6% Coronation Regular Saver and the soon to mature Christmas Regular Saver.Whilst 4.75% isn't a good rate now and doesn't currently look as though it will become competitive in the future, if rates start to fall at some point next year and Monmouthshire decide not to cut their 4.75% rate then it could become a reasonable rate for the last month or two. If it had a larger minimum balance or required monthly funding then I doubt I'd be opening it but since it only has a £1 minimum balance and requires no further funding the cost to me of having the account sat with a £1 balance for a year should be at most 1 or 2p so it seems just about worth opening on the off-chance. Admittedly it is on the lower end of accounts I would open speculatively though.

First of all you're correct, I do have their 8% and 7% regular savers. I also have the 5.6% Coronation Regular Saver and the soon to mature Christmas Regular Saver.Whilst 4.75% isn't a good rate now and doesn't currently look as though it will become competitive in the future, if rates start to fall at some point next year and Monmouthshire decide not to cut their 4.75% rate then it could become a reasonable rate for the last month or two. If it had a larger minimum balance or required monthly funding then I doubt I'd be opening it but since it only has a £1 minimum balance and requires no further funding the cost to me of having the account sat with a £1 balance for a year should be at most 1 or 2p so it seems just about worth opening on the off-chance. Admittedly it is on the lower end of accounts I would open speculatively though.

EDIT: The account is now live on their website.

https://www.monbs.com/savings/regular-saver/

Do you have the Santander £200 regular saver 5% which has a fixed rate and flexible? Mine is dormant.

I'd agree, though to be fair it does also have a disadvantage. I plan to buy my first home within the next year so I'm most likely going to be having to contact over 60 different banks/building societies to update my address and landline number at some point in the near future. Still it's a small price to pay for the other perks of holding multiple accounts.subjecttocontract said:I'm finding that having dormant accounts with say £1 in them does have other advantages. When I'm looking for somewhere e.g. to transfer my cash ISAs into then already having an account with a bank or b/society makes it much, much quicker.

Well I do rather enjoy having one or two more savings accounts than most people do, though it certainly isn't my intention to have more accounts than anyone else on MSE to be fair, my accounts have bred in recent years though not entirely deliberately.Stargunner said:

I think that Bridlington1 is striving to hold the most amount of bank and savings accounts out of everyone on MSE 😂OneUser1 said:For those who can get to a branch, the Westbrom 6% fixed for a year, £250 per month maximum looks attractive and is still available.I don’t understand why anyone with a 7% and 8% Regular Saver at the Monmouthshire would open the 4.75% variable as well. The higher paying accounts ensure continuity of membership. When they mature, and only then, certainly look for an account to maintain membership then. But not now.

I'll take that as a compliment although I'm sure there are loads of people reading this with far more accounts than I currently have. I'm aware of at least one other person on this forum who has close to double the number of accounts I have so I'm probably left eating dust myself on this occasion.trickydicky14 said:

I think Bridlington1 leaves the rest of us eating dustStargunner said:

I think that Bridlington1 is striving to hold the most amount of bank and savings accounts out of everyone on MSE 😂OneUser1 said:For those who can get to a branch, the Westbrom 6% fixed for a year, £250 per month maximum looks attractive and is still available.I don’t understand why anyone with a 7% and 8% Regular Saver at the Monmouthshire would open the 4.75% variable as well. The higher paying accounts ensure continuity of membership. When they mature, and only then, certainly look for an account to maintain membership then. But not now.

5 -

Think I may well pop in tomorrow morning and open the West Brom regular saver. Its not amazing at 6% but its fairly certain rates have hit their peak so anything around that mark is worth having for 12 months.OneUser1 said:For those who can get to a branch, the Westbrom 6% fixed for a year, £250 per month maximum looks attractive and is still available.I don’t understand why anyone with a 7% and 8% Regular Saver at the Monmouthshire would open the 4.75% variable as well. The higher paying accounts ensure continuity of membership. When they mature, and only then, certainly look for an account to maintain membership then. But not now.0 -

Kazza - thanks for your helpful advice. If only Halifax could make that clear - these 'renewals' of accounts are very confusing.Kazza242 said:

My Halifax regular saver matured near the end of October 2023. They transferred the balance plus interest to my Instant Saver account.Rich2808 said:I have a general question about opening the Halifax regular saver. My old regular saver matured 2 weeks ago but Halifax online banking does not offer it as an option for me to open a new one online. Have tried calling them twice - but apparently they were too busy to take the call.

Has anyone else had this problem with maturing Halifax regular savers. I am registered for online banking and have a current account with them.

They then rolled my existing matured account (with £0 balance) into a new regular saver account for another 12 months and applied the interest rate available at the time of maturity (5.50%). The account number remains the same.

I transferred the first payment via an internal transfer and amended my existing standing order.

Find your matured regular saver account on Halifax online banking. It should have the 5.50% rate applied to it.

You can then make your first payment. Or did you close your Halifax regular saver following maturity?

I have a matured saver account showing a 5.5% rate - but for obvious reasons I would rather have something called a regular saver confirming the fixed rate. Do I renew this into another savings account - say the reward bonus saver paying 4.2% - and then I will be free to open a new account (the actual regular saver)? The only option not given to me for renewing the account is another regular saver!!

Given I just do a transfer from my halifax account I don't really care the account number might change.

I am just not comfortable using the matured saver account number - as its not clear what its terms are or what restrictions apply to it or if they can cut the rate? If its a regular saver still - why not call it that?!

0 -

Sorted it now - did the renewal and opened a new regular saver.Rich2808 said:

Kazza - thanks for your helpful advice. If only Halifax could make that clear - these 'renewals' of accounts are very confusing.Kazza242 said:

My Halifax regular saver matured near the end of October 2023. They transferred the balance plus interest to my Instant Saver account.Rich2808 said:I have a general question about opening the Halifax regular saver. My old regular saver matured 2 weeks ago but Halifax online banking does not offer it as an option for me to open a new one online. Have tried calling them twice - but apparently they were too busy to take the call.

Has anyone else had this problem with maturing Halifax regular savers. I am registered for online banking and have a current account with them.

They then rolled my existing matured account (with £0 balance) into a new regular saver account for another 12 months and applied the interest rate available at the time of maturity (5.50%). The account number remains the same.

I transferred the first payment via an internal transfer and amended my existing standing order.

Find your matured regular saver account on Halifax online banking. It should have the 5.50% rate applied to it.

You can then make your first payment. Or did you close your Halifax regular saver following maturity?

I have a matured saver account showing a 5.5% rate - but for obvious reasons I would rather have something called a regular saver confirming the fixed rate. Do I renew this into another savings account - say the reward bonus saver paying 4.2% - and then I will be free to open a new account (the actual regular saver)? The only option not given to me for renewing the account is another regular saver!!

Given I just do a transfer from my halifax account I don't really care the account number might change.

I am just not comfortable using the matured saver account number - as its not clear what its terms are or what restrictions apply to it or if they can cut the rate? If its a regular saver still - why not call it that?!

So thanks for your help!0 -

A new Loyalty Regular Saver is due to be announced in the next few days by Coventry and it will be open to everyone with an account with the building society since January 20226

-

That might be quite a nice account. I won't be eligible, as not been with them long enough.francoghezzi said:A new Loyalty Regular Saver is due to be announced in the next few days by Coventry and it will be open to everyone with an account with the building society since January 2022

Any guesses on rate or monthly deposits, I'm thinking it could be 6% 7% and 500pcm?0 -

No idea about the rate, 7% and 500pcm would be nice but I don't believe in miracles 😁Middle_of_the_Road said:

That might be quite a nice account. I won't be eligible, as not been with them long enough.francoghezzi said:A new Loyalty Regular Saver is due to be announced in the next few days by Coventry and it will be open to everyone with an account with the building society since January 2022

Any guesses on rate or monthly deposits, I'm thinking it could be 6% 7% and 500pcm?2 -

It has to be markedly better than their existing regular saver, which is 500 per anniversary month at 5.5% though, if it's going to be a loyalty product.francoghezzi said:

No idea about the rate, 7% and 500pcm would be nice but I don't believe in miracles 😁Middle_of_the_Road said:

That might be quite a nice account. I won't be eligible, as not been with them long enough.francoghezzi said:A new Loyalty Regular Saver is due to be announced in the next few days by Coventry and it will be open to everyone with an account with the building society since January 2022

Any guesses on rate or monthly deposits, I'm thinking it could be 6% 7% and 500pcm?1

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.3K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 248K Work, Benefits & Business

- 605.2K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards