We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Regular Savings Accounts: The Best Currently Available List!

Comments

-

dealyboy said:

... can't you open a new current account and regular saver?@Gers said:I too have culled all RSs paying under 5.75% as I'm already well over PSA for this tax year, almost £400 of which is from RSs. I've missed out on the NW RS as I closed down NW in August. It's mildly annoying but I have others to keep my spirits and bank account on the up.I've got an annoying SBS two year fixed rate account due to mature in October paying a miserable 0.90% which I waltzed into without thinking so I am content with my current savings regime.

I could - but won't! I'm trying to rationlise my accounts.

1 -

Ah right, not had mine yet.Rawrzy said:Bazzalona13295 said:Having a brain fade but assuming it WAS the RS account from Tipton and Coseley that I'm waiting for Postal ID reference for........anyone in a similar situation had theirs yet?

I got the letter containing the code pretty quickly after applying, was a few days tops. Was quite surprised.

Had other stuff from around the same time so hopefully not far away.0 -

I had my ‘thank you for opening…’ Tipton letter arrive a few days ago, along with the same type of letter dated 4th July(!) for the previous Tipton RS I’d opened months agoBazzalona13295 said:

Ah right, not had mine yet.Rawrzy said:Bazzalona13295 said:Having a brain fade but assuming it WAS the RS account from Tipton and Coseley that I'm waiting for Postal ID reference for........anyone in a similar situation had theirs yet?

I got the letter containing the code pretty quickly after applying, was a few days tops. Was quite surprised.

Had other stuff from around the same time so hopefully not far away.1 -

-

Does Nationwide have a cut off for payments in to start receiving interest same day? Just funded £200 into the new Reg Sav and it has been credited with a date of 23 Sep.0

-

Thumbs_Up said:

Nah, it’s not worth it. I only went with the Coventry first saver (1st addition) because it’s £1000 a month @ 5.60% with easy access. First direct because I wanted the easy switch money, currently putting in £300 a month but will most likely drop this down to £50 or whatever the bear minimum is. I mean at the end of the 12 month period what does 100 quid or whatever the sum is, what will it buy you. Having said that if you are a individual with 100 quid spare at the end of the month I can see it’s blessings.

I haven’t gone with nationwide because I didn’t have a “burner account” also I would like to the keep the banks at arms distance and have them on my side. As aside it will be interesting to see if the banks play hardball with some forum members on here and we will have a stream of threads complaining bitterly about accounts being closed.

Also this account will last for 36 month. By that time the inflation and subsequently the interest rate might already come down. By that time This account will triumph.

1 -

Currently have 13 regular savers.Bazzalona13295 said:

Glad someone else has a 'quite mad' interest in this sort of thing. Not just me thenBridlington1 said:

For me it is certainly worth it. It takes very little effort for me to open and fund the Nationwide regular saver and the account is a now valued addition to my collection. If you throw a few other regular savers at a high rate into the mix £30 here and £10 there in extra interest from regular savers soon adds up to a sizable chunk of money.Malchester said:I really wonder whether these accounts are worth it. £200 a month into NW reg saver would give approx £96 interest over the year plus £62 interest for the rest held in Santander easy access saver = £158. Full amount in Santander easy access account for a year £124. Is it worth it for £30?

Plus it's a very nice little hobby I find (yes I am probably quite mad).

Makes sense to fund those above 5.2% rather than leave in Santander. Also have Santander edge saver at 7%

Nationwide 8%

Skipton 7.5%

First Direct 7%

YBS 7%

NATWEST 6.17%

RBS 6.17%

YBS 5.75%

Nationwide 5.5%

Halifax 5.5%

Coventry 5.5%

YBS 5.25% Not funding anymore

Lloyds 5.25% Club Lloyds 2 payments left

Coventry FHS2 5.05% Not decided what to do with this

Lloyds 4.25% Renewed after 10 payments, made £49.87 interest

1 -

Is this a fixed rate account, as issue 2 is a variable rate account?adindas said:Thumbs_Up said:Nah, it’s not worth it. I only went with the Coventry first saver (1st addition) because it’s £1000 a month @ 5.60% with easy access. First direct because I wanted the easy switch money, currently putting in £300 a month but will most likely drop this down to £50 or whatever the bear minimum is. I mean at the end of the 12 month period what does 100 quid or whatever the sum is, what will it buy you. Having said that if you are a individual with 100 quid spare at the end of the month I can see it’s blessings.

I haven’t gone with nationwide because I didn’t have a “burner account” also I would like to the keep the banks at arms distance and have them on my side. As aside it will be interesting to see if the banks play hardball with some forum members on here and we will have a stream of threads complaining bitterly about accounts being closed.

Also this account will last for 36 month. By that time the inflation and subsequently the interest rate might already come down. By that time This account will triumph.0 -

No, it's variable too, and has risen 4 times this year.Middle_of_the_Road said:

Is this a fixed rate account, as issue 2 is a variable rate account?adindas said:Thumbs_Up said:Nah, it’s not worth it. I only went with the Coventry first saver (1st addition) because it’s £1000 a month @ 5.60% with easy access. First direct because I wanted the easy switch money, currently putting in £300 a month but will most likely drop this down to £50 or whatever the bear minimum is. I mean at the end of the 12 month period what does 100 quid or whatever the sum is, what will it buy you. Having said that if you are a individual with 100 quid spare at the end of the month I can see it’s blessings.

I haven’t gone with nationwide because I didn’t have a “burner account” also I would like to the keep the banks at arms distance and have them on my side. As aside it will be interesting to see if the banks play hardball with some forum members on here and we will have a stream of threads complaining bitterly about accounts being closed.

Also this account will last for 36 month. By that time the inflation and subsequently the interest rate might already come down. By that time This account will triumph.1 -

Wheres_My_Cashback said:

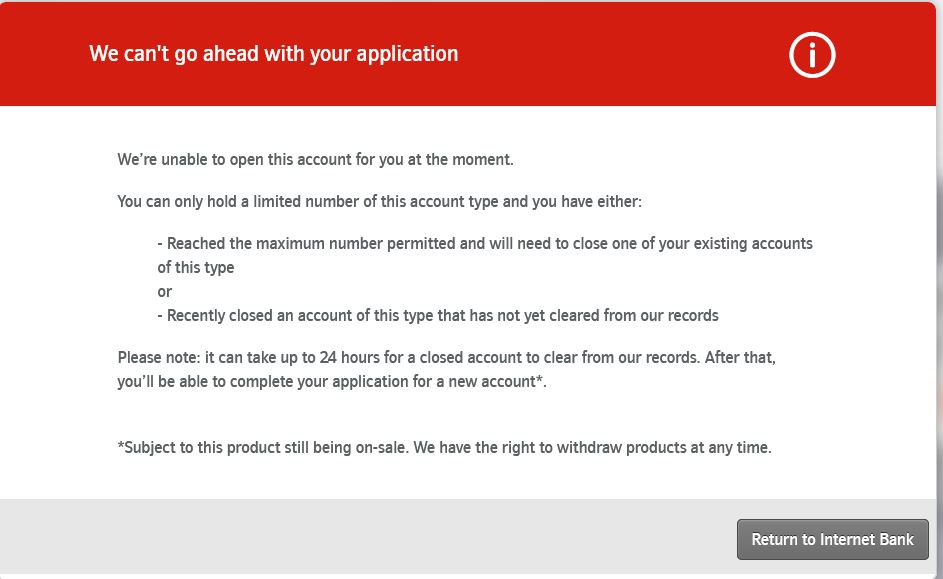

If they've tightened up their checks that is?allegro120 said:

You are only allowed one of these. If one manages to open two they will close one of them.adindas said:What method other people use to get the second Nationwide Flex RS 8%?I tried it today this is what I get ...

I remember not too far back of having 5 Flex direct current accounts paying 5%? for a year when only 1 was permitted. It was quite common amongst MSE readers to have a few ;-)

It only took them 10 months to notice before notifying of closure of 4 so I was quite happy with my extra 40 months of interest.HSBC, First Direct, precise ...TSB still ...

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards