We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Top Easy Access Savings Discussion Area

Comments

-

Agree, it's hard to see what benefit they get from having occasional access to some of my data. Classic rate tarts don't fit their model customer who has one current account, uses debit cards and cash for their spending, and who has may be one savings account.TiVo_Lad said:I do wonder what benefit these banks actually get from snooping around current accounts. Mine is mainly an intermediary account between the savings accounts that I have and so it's just money "passing through". I never use the debit card to pay for anything and haven't used cash in six months. The best they'd know is I'm a rate tart (which didn't prevent Tandem from freezing my account in the early says due to "suspicious" activity (aka classic rate tart activity)).0 -

BigBlueSky said:

If large amounts are involved and the funds leave your account straight away but don't arrive at the destination until the next day for example you will have lost a days interest. Say you have transferred the full £85,000 and lost a days interest @ 3% that is £6.99. For some it might not matter, but for others it might.FindingBBob said:Genuine question - a lot of people on here seem to be very concerned about speed of access to their funds or how quickly they deposit. Most, at worst, seem to either have same day withdrawal or next working day. Most have at least same day deposit recognition. I keep a reasonable float of cash in my current account that would cover most "emergency expenses" any thing bigger is therefore planned for.. why is speed so important? Am I missing something?Yes, rather annoyingly I have experienced this today.

Transferred 85k from my Aldermore account this morning. It is still not in my Nationwide current account at 2pm. I have now missed the 1pm cut-off time at Charter Bank to have the funds credited to my savings account.

One day of interest lost.. to me.

I guess either Aldermore, Nationwide or Charter pocket my 7 quid.0 -

my Money Dashboard OB connections with Santander show no expiry (both app and site), but every 90 days, the connection does need to be renewed.Band7 said:liamcov said:

I'm uncomfortable with this too - are there any common problems with this?pecunianonolet said:

Skipton told me earlier that because my withdrawal request was past 8pm it would only be processed the next working day. Seems like a change as I'm pretty sure I took money out past 8pm before and had it transferred max 30 min after. Rather disappointing so I guess I need a Chip account, with a dummy current account attached as I don't like snooping via open banking.tg99 said:Kent Reliance has a cut off time to receive withdrawn funds by end of same working day…..in practice does anyone know if a pre-cut off withdrawal arrives in your current account pretty quickly within say 10-20 mins like Skipton withdrawals?

The one good thing with Chip is the access is limited to 90 days I think so I guess I have to confirm at that point again, but another one (Tandem I think) doesn't seem to have a limit.BTW, looks I have a CHIP connection without an expiry date

1 -

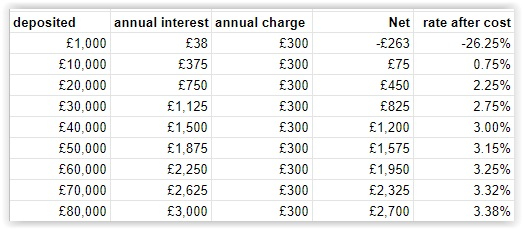

I see a lot of people here who have up to FSCS amount, I tried to search but has anyone applied for this and got it easily? Private Savings Account | Savings | Private Banking | Virgin Money UKIt gives rate based on BoE -0.25%.You would need to get the private account which costs £25/mo but with this rate it would be worth it? (https://uk.virginmoney.com/private/)1

-

On a very quick calc, I wouldn't think this account is of interest to many. If I had the money sitting there all year, I'd go for a fixed term or a notice account, which would pay me better interest.Futuristic said:I see a lot of people here who have up to FSCS amount, I tried to search but has anyone applied for this and got it easily? Private Savings Account | Savings | Private Banking | Virgin Money UKIt gives rate based on BoE -0.25%.You would need to get the private account which costs £25/mo but with this rate it would be worth it? (https://uk.virginmoney.com/private/)

5 -

There are better 1 year fixes available at the moment without the high annual £300 charge of that account.Futuristic said:I see a lot of people here who have up to FSCS amount, I tried to search but has anyone applied for this and got it easily? Private Savings Account | Savings | Private Banking | Virgin Money UKIt gives rate based on BoE -0.25%.You would need to get the private account which costs £25/mo but with this rate it would be worth it? (https://uk.virginmoney.com/private/)

If, on the other hand, you consider the other services available for that fee to be worthwhile, that is another matter.

David£6000 in 20230 -

It seems they are all NLA. The only ones available to open are Issue 32 and 31. I don't think these are increasing rates. Are they?savethepandas said:Charter Savings Bank Easy Access issue 28 rate rising from 3% to 3.25%on 27th Feb.0 -

@Band7Band7 said:Absolutely. This HSBC account should always come with a big health warning. If you can treat it a bit like a 30ish day Notice account, where the withdrawal date should always be the day they pay interest (1st, or next working day after 1st).

To skim off the monthly interest, it is possible to use Chat to request closure of an OBS after you have emptied it. They'll close it within 24 hours, and you can then immediately open a new OBS. Bit of a faff, so you may decide to settle for the lower rate on the monthly interest.

closure of OBS & opening another OBS- does this process serve any purpose?

0 -

As you only earn a minimal amount of interest in the month that you make the withdrawal, closing it on withdrawal and then opening another one means you can then start earning the higher rate of interest again straightaway.ChewyyBacca said:

@Band7Band7 said:Absolutely. This HSBC account should always come with a big health warning. If you can treat it a bit like a 30ish day Notice account, where the withdrawal date should always be the day they pay interest (1st, or next working day after 1st).

To skim off the monthly interest, it is possible to use Chat to request closure of an OBS after you have emptied it. They'll close it within 24 hours, and you can then immediately open a new OBS. Bit of a faff, so you may decide to settle for the lower rate on the monthly interest.

closure of OBS & opening another OBS- does this process serve any purpose?

1 -

Freedommm said:

It seems they are all NLA. The only ones available to open are Issue 32 and 31. I don't think these are increasing rates. Are they?savethepandas said:Charter Savings Bank Easy Access issue 28 rate rising from 3% to 3.25%on 27th Feb.

They are increasing but from a lower 2.64% to 2.89%.

1

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards